Why should investors care about the importance of portfolio diversification? Doesn’t ‘diversification’ sometimes feel like overused jargon?

Well, no, it isn’t.

However, if you have been bogged down by buzzwords that seem to overly complicate how to invest, we understand the frustration. Traditional financial advisors tend to make the subject of investing sound very difficult when in reality core concepts like portfolio diversification are straightforward.

Portfolio diversification is not just another buzzword: It is a major deciding factor whether you lose your money or grow it in the stock market over the long term.

True diversification of investments, when done correctly, helps reduce your risk, preserve your capital, and grow your money.

Importantly, this means investing in many negatively correlated assets.

A helpful hint here: Your friend with the portfolio of dozens of high-growth tech stocks is not properly diversified. Indeed, they are at risk of heavy volatility and money loss.

Let’s listen to a familiar voice to guide us on the subject.

“Rule No. 1 is never lose money,” famously said Warren Buffett. “Rule No. 2 is never forget Rule No. 1.” By minimising your risk, portfolio diversification protects your investments and provides you with optimal opportunities for long-term growth.

Far from being jargon, portfolio diversification is a concept every investor must understand, appreciate, and implement.

In this article, we will consider:

- What is portfolio diversification? Important math concepts

- The importance of portfolio diversification: A study of benefits

- How to achieve portfolio diversification

- Investing in a diversified portfolio

- Maintaining your diversified portfolio: The place of rebalancing

1. What is portfolio diversification? Important math concepts

What if we start with a little story that illustrates what portfolio diversification is all about? (Who doesn’t love a good story?)

It’s the story of Tom and Mitch:

Meet Tom – he plants bananas because everyone in his neighborhood loves bananas. They sell like crazy!

But his neighbor Mitch decided to grow bananas, oranges, apples, and lemons. People kept telling him he should focus on bananas – they will bring him a higher yield.

One day the moisture level changed (humm…), and the banana crops became completely ruined.

Guess who had fruits on the table by the end of the day? You guessed right: Mitch.

Planting many different species of plants and fruits ensured that Mitch’s farm didn’t suffer complete ruin when the weather became unpredictable. The same concept is compatible with your investments.

Portfolio diversification is how you emulate smart Mitch and avoid the sad tale of Tom. It’s how you ensure you don’t put all of your eggs in one basket (to use a popular metaphor).

But let’s leave the story now and explain the importance of portfolio diversification in more concrete terms.

Risk and Return

Underlying the concept of portfolio diversification is the fact that two elements must be important to the investor: return and risk.

On the one hand, you want to be sure you will earn good returns from your investment. But on the other hand, you want to ensure you don’t lose your money in the investment.

Many investors lose money because they focus exclusively on the potential return of an investment. But as Warren Buffet has told us, the number one rule is to avoid losing your money (ie; consider the risk).

Not surprisingly, one of the main goals of a smart investor is to protect his/her money.

Tom had more potential return than Mitch — bananas were the favourite fruits in the land. But when a change in environment took all the bananas away, it didn’t matter that he had more potential returns.

Mitch had less potential return — bananas, the favourite fruit, were only a fraction of his “holding.” However, because ¾ of his holdings were safe, he earned returns on those even when his bananas were gone.

The morale as it applies to investing is simple: potential returns only make a difference if you can protect your principal investment from risk.

Measuring Risk

For many years, investors focused almost exclusively on the potential return of an investment.

But that was not because they didn’t understand that risk is important. The challenge was finding a quantitative way to measure risk.

Harry Markowitz, an American economist, developed such a quantitative technique — the Modern Portfolio Theory (MPT) — in his journal article, “Portfolio Selection,” published in the 1952 edition of the Journal of Finance.

In the MPT, the risk of an asset is measured as the standard deviation of the expected returns of the asset. The standard deviation is a popular statistical measure of how variables deviate from the mean. The more the expected returns of an asset deviates from the mean, the riskier the asset.

Put simply, the higher the standard deviation of an asset, the riskier it is.

With this, investors could now measure both the returns and risk of an asset, and then compare both.

Diversification, correlation, and risk

Markowitz insisted that the average investor is risk-averse — for a given level of returns, he/she would want to have a minimum level of risk; for a given level of risk, he would want to have the maximum level of return.

Given this risk-averseness, Markowitz suggested that the more sought-after goal for investors is to minimise risk for a given return and maximise return for a given risk.

But how could investors reduce their risk?

Next, he introduced the concept of correlation. Correlation measures how much two variables move in the same direction in response to certain factors.

Let’s review some basic math here. The correlation coefficient between two variables can range from -1 to +1.

If the correlation coefficient is -1, it means that the two variables are completely negatively correlated — when one moves in one direction, the other moves in the opposite direction at the same rate (a 10% increase in one leads to a 10% decrease in the other).

If the correlation coefficient is +1, it means that the two variables are completely positively correlated — when one moves in one direction, the other moves in the same direction at the same rate (a 10% increase in one leads to a 10% increase in the other).

How does all of this apply to your investment portfolio?

If the same factors cause two companies to move in the same direction (positive correlation), their stock prices will move in the same direction — when one falls, the other falls. However, if the same factors cause two companies to move in the opposite direction (negative correlation), their stock prices will move in the opposite direction.

Understanding this kind of correlation is at the heart of portfolio diversification.

Markowitz postulated that the less positively correlated your portfolio, the less the risk in that portfolio. A portfolio of two assets where both of them have a correlation coefficient of +1 is the riskiest — the same factor in the market can cause both of them to fall at the same time and at the same rate.

If that correlation coefficient is +0.5, it is less risky because even though they will move in the same direction, it’s not at the same rate.

According to Markowitz’ theory, the farther away from +1 and the closer to -1, the better.

A diversified portfolio

Consequently, the best way for an investor to minimise risk is to create a portfolio of assets that are negatively correlated, such that when one is falling and losing value, the other assets can compensate by rising and growing in value.

Consider a brief example. Suppose Investor A invests all his $100,000 in a single stock; if it falls by 50%, he has lost half of his investment ($50,000).

Suppose he invested in two stocks that are perfectly positively correlated (+1), the same factor that causes stock A to fall by 50% will now cause B to fall by 50%, which means he is still in the same situation as before (lose $50,000).

This often happens with novice investors, who assume that by investing in several tech stocks they are gaining diversification; they are not. The tech stocks end up being mostly positively correlated to the same industry.

However, suppose the two stocks have a negative correlation of -0.5. Then, what causes stock A to fall by 50% causes B to rise by 25%. In that case, you only lose $12,500 (A loses $25,000, but B gains $12,500).

This is the core objective of portfolio diversification, and achieving it requires spreading investments across:

- Industries

- Regions

- Market cap sizes

- Asset classes

Ideally, the less positively correlated assets are, the less the risk of the portfolio.

The best diversification is perfect negative correlation. In that case, what causes A to fall by 50% causes B to rise by 50%, and your loss is only at $0 (A loses $25,000 and B gains $25,000).

When a portfolio contains less positively correlated or more negatively correlated assets, such a portfolio is said to be well diversified. And when a portfolio is really diversified, the portfolio’s overall risk becomes far less than any of the risk of the individual assets in the portfolio.

Suppose you bought only A or only B. In that case, the risk (loss of $50,000) is always greater than if you bought both A and B in a less positively correlated portfolio of +0.5 (loss of $37,500), a negatively correlated portfolio of -0.5 (loss of $12,500) or a perfect negative correlation (loss of $0).

The importance of diversification can be seen in how a $50,000 potential loss can become a $0 loss. It’s so powerful.

[Want to learn how to construct a diversified portfolio? Read “Building an Investment Portfolio from Scratch: The Ultimate Guide.”]

2. The importance of portfolio diversification: A study of benefits

If you don’t fancy calculations, you probably wonder how any of the above makes any difference to you. What’s the actual importance of portfolio diversification in your investment strategy?

Remember Tom and Mitch?

The problem with Tom is that he didn’t have a diversified portfolio — whatever happens to the banana crop affects him 100%. What’s more, if he had two fruits affected by moisture level in the same way and at the same rate (perfect positive correlation), he would still lose everything.

But if the other fruit is affected by the moisture level in the same way but not at the same rate, he would not have lost everything. If the correlation is +0.5, he would still have had 50% of the other fruit to sell, thereby reducing his risk.

Even better, if he had followed Mitch’s strategy and planted fruits that are negatively correlated to bananas in terms of moisture level, he would have had many more fruits to sell like his co-farmer.

Poor Tom.

To make it more concrete, let’s consider the importance of portfolio diversification by looking at the main benefits for investors.

Minimising risk

Portfolio diversification helps reduce the risk of losing your money; the more diversified your portfolio, the less your risk exposure.

If Warren Buffett is right and the first rule in investment is to avoid losing your money, creating a well-diversified portfolio is the best way to follow that rule.

“If you invest and don’t diversify, you’re literally throwing out money,” said Jeff Yass, co-founder of Susquehanna International Group, one of the leading firms on Wall Street.

“People don’t realise that diversification is beneficial even if it reduces your return. Why? Because it reduces your risk even more.”

Reducing volatility and preserving capital

Related to risk reduction is capital preservation. It’s only when you don’t lose money that you can grow it.

Therefore, by minimising risk, you can reduce the volatility of your investment and preserve your capital.

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for,” said Robert Kiyosaki, investor, entrepreneur, and author of Rich Dad, Poor Dad.

Portfolio diversification ensures that your money keeps working for you for a long time by reducing your risk of losing it.

Maximising long-term returns

This is where it gets even more interesting.

Actually, you can minimise your risk by just investing in bonds (with low returns). If preservation of capital is all that matters, a portfolio of treasury bonds is the best (and all that correlation stuff won’t matter too much).

However, remember that returns and risks are both important. You are not merely seeking to minimise risk but minimise risk for a given level of returns and maximise returns for a given level of risk.

The question is not “how can I minimise risk” per se, but “how can I minimise the risk of earning a 10% return (for example) on my investment?”

The yield on the US Treasury 10-year bond is currently 1.58%. Are you happy growing your money at that rate? You shouldn’t be.

Treasury bonds will be a good answer to the first question above (how can I minimise risk?) but a poor answer to the second. If you want 10% returns, no treasury or corporate bonds will give that to you. For that, you will need some stocks and REITs.

What portfolio diversification does is combine assets that can give you the returns you desire in a way that minimises your risk to the level you are comfortable with. It does this by ensuring that those assets are less positively correlated or more negatively correlated.

And if you have a target risk level (say, a standard deviation of 0.4), portfolio diversification is the best way to maximise returns for that given level of risk.

It will combine stocks, REITs, and bonds in a way that you can still earn higher returns for that risk level than if you just invested everything in treasury or corporate bonds.

To illustrate this point, the chart below shows that some individual assets in this portfolio have lower volatility than the overall portfolio.

Though the overall portfolio has lower volatility than the average of the individual assets, why not just invest only in PCY (a bond ETF) with the lowest volatility at 0.06?

That would only be a good decision if minimising risk is the only thing the investor wanted. But most investors want their returns as well.

Consider the next chart.

The overall portfolio has 15% returns compared to the 10% returns of PCY.

Besides, the current volatility is not the maximum volatility attainable. The maximum is 0.08%, which is just 0.02% less than the volatility of the best bond ETF in the portfolio.

Also, in the long term, the gap between the returns of this portfolio and the bond ETF (PCY) will expand.

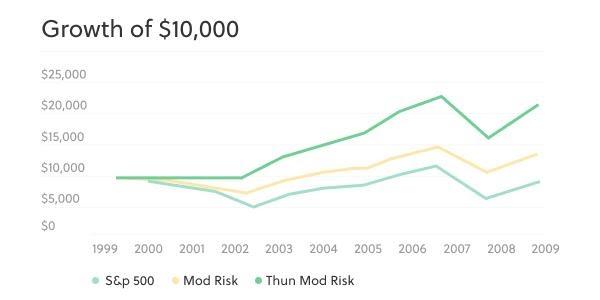

In the long-term, the more diversified a portfolio, the better the returns.

For example, the chart below shows a positive correlation between diversification and returns that grows with time.

The S&P 500 is invested in the S&P 500 index — an index that tracks the performance of the top 500 companies (by market cap) in the US.

The Mod Risk portfolio contains 40% US stocks, 30% global stocks, and 30% high-quality bonds, while the Thun Mod Risk is “a portfolio globally diversified across multiple asset classes including stocks, bonds, real estate, and commodities.”

The broader the diversification, the higher the returns over the long term. The Mod Risk portfolio with broader diversification than the S&P 500 has higher returns, and the Thun Mod Risk portfolio with broader diversification then beats out the Mod Risk portfolio.

[To understand more about investing with stocks, bonds, and REITs, read “Where to Invest $100k: A Smart Strategy For The Future You”]

3. How to achieve portfolio diversification

How then can an investor achieve this type of well-oiled portfolio diversification?

As mentioned above, there are four main ways to diversify an investor’s portfolio:

1. Portfolio diversification by asset class

Investors use three major asset classes to create wealth: stocks, bonds, and REITs. One way to diversify is by investing in all these three asset classes rather than putting all your money in one.

Stocks and bonds, for example, are negatively correlated in many ways (but not at all times). People move money to the bond market when the stock market is down, or the prospects are on a downtrend, and they move money back to the stock market when performance improves.

So when the stock market is down, the bond market is rising, vice versa. Creating such a negative correlation in your portfolio helps you reduce your risk.

Think about this: while bonds have low returns and low risk, stocks complement them with high returns and high risk. Combining the two not only helps to reduce overall risk, but it also helps to minimise risk for a given level of returns and maximise returns for a given level of risk.

REITs are stocks of companies in the real estate market. Adding a different market (with different risk factors and another negative correlation) to the mix also reduces risk. Furthermore, REITs pay a high dividend income (minimum of 90% of income), which supplies more money for reinvestment.

As an investor, you can begin your portfolio diversification by understanding these three asset classes.

2. Portfolio diversification by market/geography

A second strategy is to diversify by market. While unsystematic risks only affect a company or an industry, there are systematic risks that can affect entire economies. A rise in interest rate in the US, for example, will affect the whole US stock, bond, and REITs market.

If you are only invested in the US market, you will expose all your assets to economic conditions in the US. And when those conditions turn negative, you might lose a lot of money.

The way to minimise such risk is to diversify by investing in other markets that are less positively correlated or more negatively correlated to the US market.

You can invest in:

- Developed markets: These are markets in North America, Western Europe, East Asia and Australasia. As long as these markets have “less positive correlation” to the US or even zero correlation (what happens in the US does not affect them at all), a portfolio with investments in these markets will further minimise your risk.

- Emerging markets: They include markets in Brazil, Russia, China, India, etc. These markets are rapidly growing, though infrastructure and household income are not at the level of the developed markets. Emerging markets are riskier, but like stocks, they have higher returns to go with (due to rapid economic growth). Their high risk is diversified (and reduced) with the reduced risk of the developed markets. And with the correlation between emerging markets and the US market below +0.70 since 2013, a portfolio with investments in emerging markets will have even less overall risk.

- Global market: You can also diversify by investing in the global market, without distinction between emerging and developed markets or a limitation to only developed or emerging markets.

3. Portfolio diversification by industry

Diversification is also commonly achieved by purchasing assets across various industries.

As long as two industries have a less positive correlation or a negative correlation, a portfolio that contains those two industries will be less risky than if you invested only in any one of the two industries.

Remember that zero correlation also reduces your portfolio risk. Investing in two unrelated industries (zero correlation) is less risky than investing only in any of the two or investing in two industries with a positive correlation.

Popular industries with investors include financial services, tech, healthcare, energy, basic materials, and consumer cyclical.

Spreading your investments across all of those industries in February 2021 would have been of great benefit.

At the time, the tech-heavy Nasdaq took a plunge, while stocks in the energy, financial services and constructions sectors surged. Having a portfolio that incorporated a balance between industries would have helped blunt the blow of the Nasdaq downtrend.

4. Portfolio Diversification by market capitalisation

Market cap is another diversification strategy.

There are three types of categories by market cap: small-cap, medium-cap, and large-cap.

Like developed markets, large-cap companies are less risky with modest and stable returns. Low-cap companies are like emerging markets — more risk and more returns. Middle-cap companies are in the middle of the pack — moderate returns and moderate risk.

Investing in the three types of companies can further increase returns for a given level of risk and reduce the risk for a given level of returns.

4. Investing in a diversified portfolio

Embracing ETFs

Having understood the importance of portfolio diversification, what’s the best way to invest in a diversified portfolio?

The best way to invest in a diversified portfolio is by creating a portfolio of ETFs. An ETF is a basket of securities that tracks a particular index (passive investment) and is traded like a stock on the exchange.

The primary reason why ETFs are the best is that a single ETF is a diversified fund in and of itself.

Instead of buying five stocks to achieve diversification, you will get more diversification by buying an ETF of stocks. An S&P 500 ETF, for example, has investments in all the companies that make up the S&P 500.

Through the share of a single ETF, you are exposed to all the companies in the S&P 500, which gives you diversification by industry.

If a single ETF already gives you diversification, imagine combining several ETFs in a portfolio. You will have a broader level of diversification that you can’t achieve by buying individual stocks, bonds, or REITs.

[Want to know more about ETFs and their advantages over buying individual assets or mutual funds? Read “Why Invest in ETFs: Explaining the Popularity of the Go-To Fund”]

Diversified portfolio with Sarwa

For example, every Sarwa investor has a portfolio that contains:

- Vanguard Total Stock Market Index ETF (VTI): This is a stock ETF that invests in US companies across various industries. The ETF currently contains the stocks of 3755 companies in the US. In addition to industry diversification, it also provides diversification by market cap, with a good mix of large-cap, medium-cap, and small-cap stocks.

- iShares MSCI EAFE ETF (IEFA): This is a stock ETF that invests in the developed markets. With this, you enjoy diversification by market. Moreso, since it is an ETF (with 2,799 companies), you also enjoy diversification by industry and market cap within a diversification by market. It’s diversification galore.

- iShares MSCI Emerging Markets ETF (IEMG): Likewise, with this stock ETF, you enjoy diversification by market (the emerging markets) while also enjoying diversification by industry and market cap within the ETF itself.

- Vanguard Real Estate Index Fund ETF (VNQ): VNQ is a REITs ETF. It adds diversification by asset class (REITs) to your portfolio. By investing in 152 different REITs, this single ETF provides its own diversification.

- Vanguard Total Bond Market Index ETF (BND): This is a US bond ETF that invests in various treasury and corporate bonds. The 18,391 bonds in this ETF are diversified in themselves. But when you add them to your portfolio, they add diversification by asset class.

- Vanguard Total Bond International Market Index ETF (BNDX): BNDX provides both diversification by market (international market) and asset type (bonds). And the ETF is diversified with 6,042 bonds.

Truely, the best way to achieve broad and thorough diversification is by investing in ETFs. This is why Sarwa invests your money in ETFs that provide diversification by asset class, industry, market, and market cap.

[The need for broad and thorough diversification is why you should not invest only in the S&P 500]

Sarwa seeks to understand your risk tolerance (very conservative, conservative, balanced, moderate growth, growth) and time horizon, and then determine the asset allocation formula that will maximise returns for your risk level.

That is, what percentage of your money will be in VTI, IEFA, IEMG, VNQ, BND, and BNDX depends on your risk tolerance, time horizon, and investment goals.

Whatever allocation formula best fits you, with Sarwa, you will have a diversified portfolio that minimises your risk and maximises your return.

[Wondering why 4 of the ETFs above are Vanguard ETFs? Learn more about Vanguard ETFs in “What is the Best Vanguard ETF?]

5. Maintaining portfolio diversification: The place of rebalancing

Once you have a diversified portfolio, you need to keep it diversified based on your asset allocation formula.

Due to short-term price variations, some of your assets will rise, and some will fall, distorting the asset allocation formula of your portfolio. For example, if you allocated 30% to VTI and 20% to BND, a rising bond market may change that allocation to 15% VTI and 35% BND, which is not ideal for you.

This is where rebalancing comes in. It helps restore the ideal portfolio allocation designed to fit your risk tolerance, time horizon, and financial goals.

Sarwa helps you rebalance your portfolio automatically to keep the allocation formula and ensure your portfolio stays maximally diversified.

Now that you understand the importance of portfolio diversification to your investments, it is time to start building wealth by putting your money in a diversified portfolio.

In this ultimate guide to building wealth from nothing, you will learn how to get started step-by-step.

Takeaways

- Risk and return are both important to an investor.

- Portfolio diversification helps to minimise risk for a given level of returns and maximise returns for a given level of risk.

- A diversified portfolio contains assets that are “less positively correlated” or negatively correlated.

- You can diversify by asset class, market, industry, and market cap.

- ETFs provide the best opportunities for diversification. Their inherent diversification added to portfolio diversification provides an unmatched level of diversification.