One of the largest communities of Sarwa’s clients is management consultants. What do we know about consultants? They are hard-working, busy, and smart professionals who trust us with their money to invest it and plan for their future.

Consultants use a rigorous, analytical application of their expertise to come up with insights and roadmaps that will help their clients succeed. Their go-to words? — information, expertise, insight, and execution. After many coffees and post-it notes to better understand what sets them apart – we found out that they share 3 main traits and a mindset that helps them adapt and succeed. In between all the coffees, we also decided that these traits are not exclusive to consultants and anyone can start applying them right away.

They know the science and follow the data: People can’t pick stocks nor can they time the market.

Passive beats active

Information about investing is more available than ever. Expertise and studies have shown countless times the same outcomes. Go passive.

Passive investing is a “buy and hold” approach. Passive investors purchase certain assets and hold on for the long run as they bet on the assets’ appreciation in value. An example of passive investment would be purchasing an exchange-traded fund (ETF) that tracks any market index.

Active investing is an investment strategy in which investment managers claim to know which asset will outperform the rest, and cherry-pick these assets from time to time to try and achieve exceptional returns.

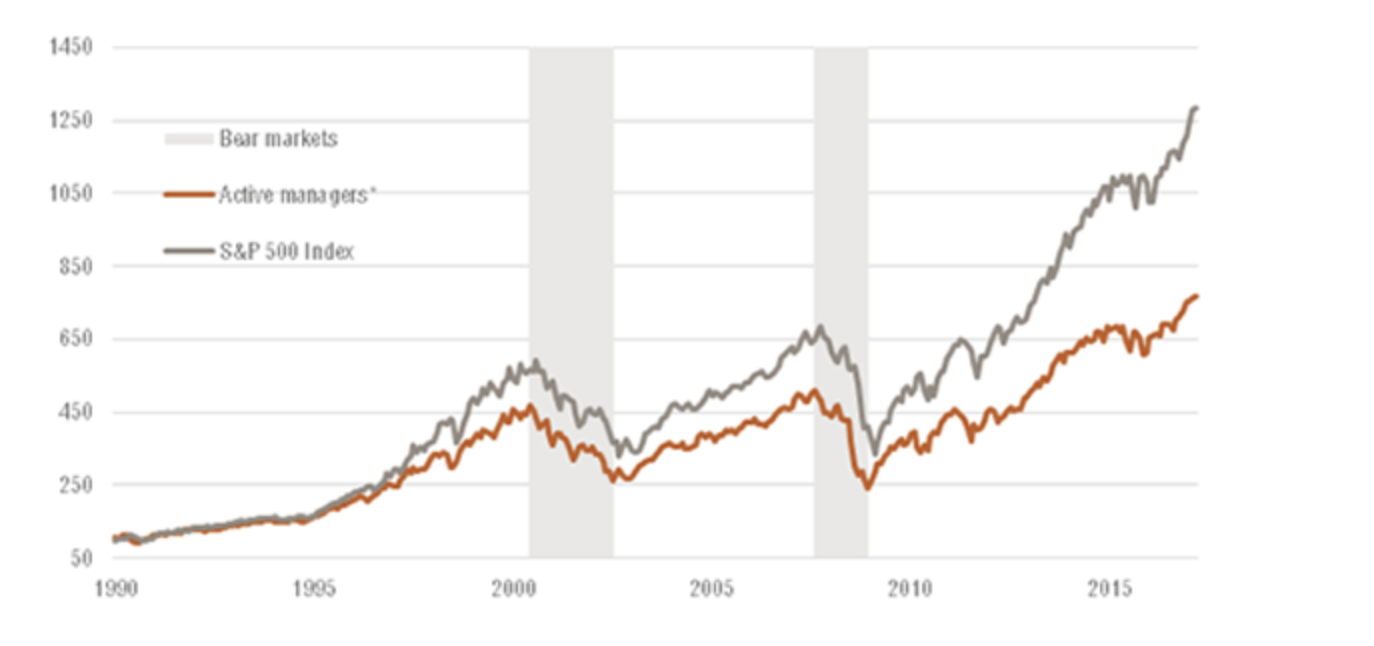

The following graph shows the difference in performance between the S&P 500 index and Active managers since 1990.

Source:Morningstar

Long story short, you could have achieved much higher returns if you simply replicated the S&P 500 index instead of giving your money to fund managers who claim that they can beat the market.

The main issue with active investing is the fees associated with it. Here are some of the major fees that differ between passive and active investing:

1- Management fees: Management fees for actively managed funds are higher than those of passive funds because active funds will have a professional money manager overseeing them and thus cost more.

2- Performance fees: Active fund managers are compensated for their work by performance fees. If fund managers happen to achieve returns that exceed a certain target, they are entitled to receive a certain percentage of the profits.

3- Transaction fees/Commissions: Active managers tend to make large amounts of trades as they try to enter and exit positions at the right time to outperform the market. This high frequency of trades leads to much higher trade commissions from brokers compared to passive funds who only perform transactions to rebalance their allocation and maintain a similar exposure to the asset they are tracking.

4- 12b-1 fee: A 12b-1 fee is a marketing fee that mutual funds charge in order to promote themselves to other potential clients. It is used to advertise the fund and mail prospectuses in attempt to attract more investments.

There are many other hidden fees for actively managed funds that we can include, but these four are enough to show how expensive it is to have someone managing your money.

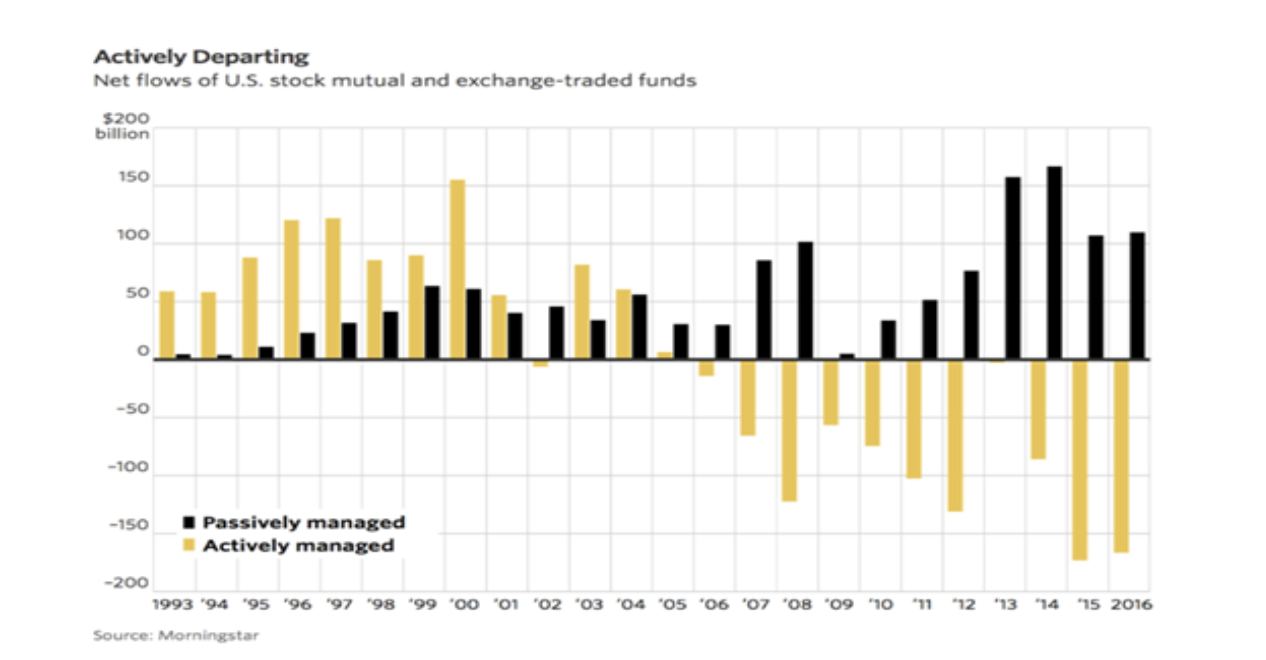

The following graph shows the net flows of mutual funds vs exchange-traded funds.

These days, investors want affordable financial advice tailored to their individual needs. They want to know how much they’re paying for that advice. This requires a change in the way that advisors do things.

Looking at this graph above, we can see that people are starting to realize that they are better off investing in passive funds. The higher fees and poorer performance are driving a shift from actively managed funds to passive ETFs. Mutual funds witnessed an outflow of over 150 billion US dollars in 2016, compared to an inflow of around 100 billion US dollars for ETFs.

But it’s not just about costs. People also demand convenience, with on-demand access to their investments across platforms. To be successful, wealth management needs to blend seamlessly into our lives, making it easy for us to invest and manage our money.

The best time to invest is now

Waiting for the “best” time to invest is rarely a successful strategy. For investors seeking to grow wealth over the long term, the best approach is almost always best to invest right away.

The next question to answer is: ‘Do I invest one lump sum or gradually?’

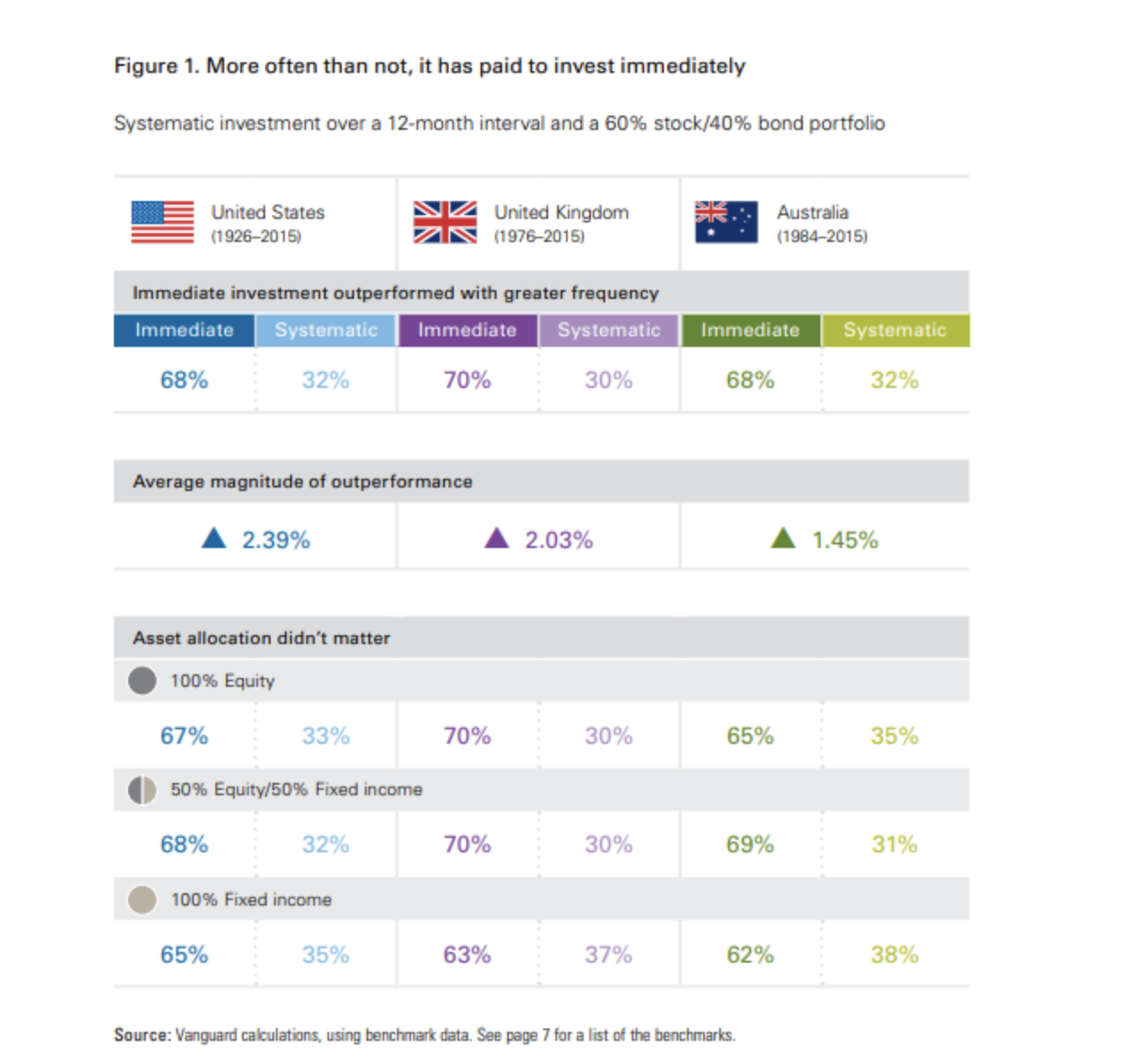

Vanguard, one of the largest investment management firms in the world, published a study in 2016 that proves that investing a large sum of money into the market yields higher returns than investing systematically.

The following table shows how immediate investment into the market outperformed systematic investment by 1.45% to 2.39% depending on the country. People who invested in the market right away instead of sticking to a schedule, received returns higher by 1.45% in Australia, 2.03% in the United Kingdom, and 2.39% in the United States.

Even though the numbers prove that it is better for your returns if you invest early, most people who have large sums of money are too afraid to go all out straight away. These people usually use a strategy of investing in a regular and fixed method to protect their lump-sum in case the market takes a dip.

Investing systematically can ease you into the market without your emotions coming into play. It is psychologically easier for an investor to enter the market with small amounts periodically than entering with a large sum of money and risk witnessing large losses. The study shows that if you want to use that method to avoid the stress of investing all at once, you should invest the full amount within one year. This could be either done by putting money on the side-line and entering the market periodically, or for even better results, investors should invest the entire amount in safe securities such as bonds, and gradually move them into riskier assets.

Sarwa helps you remove this stress by scheduling deposits using the dollar-cost averaging method for all its premium clients (50k+ portfolio balance) free of charge.

They like to automate as much as possible

Respect your own time

“Pretend Your Time is Worth $1,000/Hour and You’ll Become 100x More Productive.” At some firms, management consultants executives charge these rates and more to their clients – and as a result, the pressure and efficiency required to deliver forces them to automate “non-value added” time/chores to do their best work and enjoy free time properly rather than spend it on chores.

When it comes to investing, consultants don’t like to waste time trying to time the market (we showed earlier that active investment barely ever works) and don’t waste time making manual deposits. By automating their deposits, consultants (and all other investors) would eliminate all the hassle and time associated with personally adding money to a portfolio, which would allow them to focus on their daily tasks while making sure that their portfolio is growing.

The power of automation is opening wealth management up to a much broader audience.

Save Money – Always

How many times have you decided to only spend a certain percentage of your salary in a given month, but end up spending much more than you expect? Automating money deposits into your portfolio leaves less money lying around for discretionary spending. This way, you are constrained to only a certain amount of money to spend in a given time period.

Follow The 50/30/20 rule

The 50/30/20 rule is a famous rule that says: You should allocate 50% of your income towards necessities and day to day operations, 30% towards your hobbies and wants, and invest the 20% that is left to achieve your financial goals – of course after having put aside an emergency fund of 3 to 6 months living expenses. Always pay yourself first before paying anyone around you. Invest in your future and make sure that the 20% is being put to work, and you should be able to plan your spending accordingly. There are other rules and tools out there that help you manage your finances but this is a great one to comportalize your finances.

They keep it simple

Investing is not complicated. If you are planning on investing and the investment manager is making it sound complex, it is probably a bad investment and you should run the other way. From our experience since launch, we’ve found very few management consultants venture into the expensive saving plans that were popular in the UAE. Mostly, they’re too complicated to begin with and are known for being opaque and for hiding fees and commissions. If a plan mentions lock-in periods, cancellation fees, and other weird jargon, re-question it.

Simplicity wins.

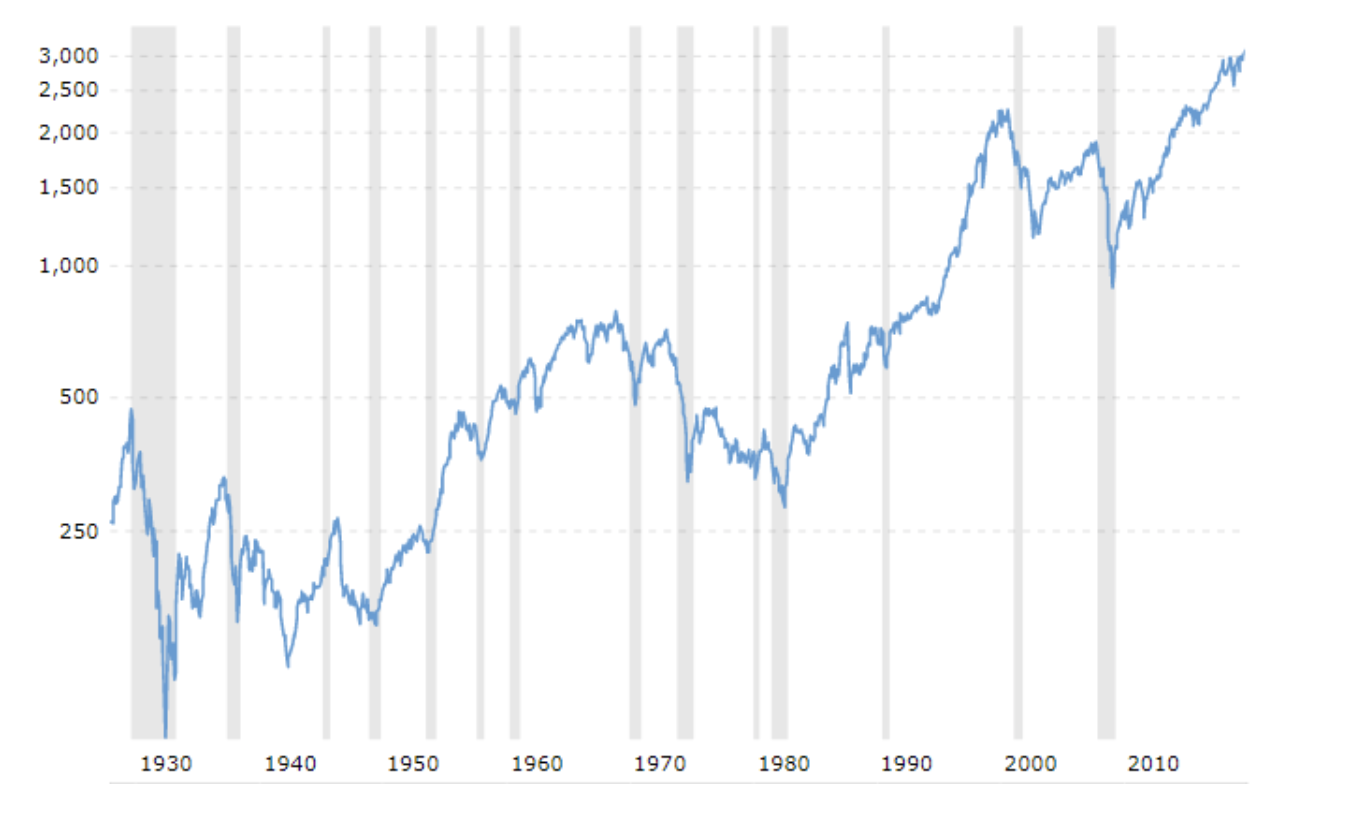

Let’s look into numbers. Here is a graph of the S&P 500 index throughout history:

Source: https://www.macrotrends.net/2324/sp-500-historical-chart-data

As you can see, the general trend of the stock market has always been upward. Companies are growing, technology is developing, and businesses are expanding. Do not worry about when to invest, but worry about not being in the market.

In investing, try to focus on what you can control instead of what is out of hand. Do not think about what returns you will be getting on your investment, but rather, think about how you can maximize these returns. Here are three things you should consider when investing your money:

1- Fees: Your investment fees should have a cut-off point of 1%. Consider any investment that has fees higher than 1% as a bad investment. Higher fees will feed off your profits and leave you with very low profits after everything is deducted.

2- Time-horizon: As seen in the S&P graph, no matter how much the market dipped in certain time-periods, it always managed to recover and perform even better in the long-run. Do not try to bet on short-term gains as it is almost impossible to make money with all the fees associated with active investments. In fact, you should look at long-term returns by riding the passive wave of the market.

3- Emotions: It is hard not to check your portfolio from time to time to see how your hard-earned money is doing. It is human nature to feel stressed when you see your portfolio not doing well and to feel ecstatic when you see it making good returns. However, you should always control your emotions as to not withdraw your money when the market is down, and deposit more money when the market is up.

In conclusion, management consultants make sure that they are investing in a smart and non-time consuming manner. Trust the data, automate your investments, keep it simple, and you should be on track for a successful investment.

Ready to invest in your future?