In times of economic stress, markets tend to be volatile with big swings. Some investors wonder if it is best to wait until the ‘uncertainty’ passes to invest their money.

The reality is the market is uncertain by nature. Studies have shown that even bad timing in investing pays off more than not being in the market. For those already invested, selling investments during times of market volatility is likely to do more harm than good -and to derail sound financial strategies.

We wanted to run the numbers and ask the questions. Even if we can not predict the future, there are many lessons we can take from the past.

What is the biggest investment mistake?

According to Dr. Jiro Kindo, our Head of Portfolio Construction and MIT Ph

Does an average active retail investor trade well?

The short answer is no. Effectiveness of active trading is controversial at best. Theoretically, to do this well, you have to “know more than the market”. Academic research has a lot to say about this. Retail investors trade badly in several ways:

- Typically trade too much and accrue substantial transaction costs.

- The stocks they sell outperform those they buy – referred to as the “disposition effect”

- They also trade on the basis of stale news

Can retail investors reliably hire institutional investors to actively trade for them?

Again the answer provided by research is: NO. Few institutional investors reliably beat their passive benchmark on a risk-adjusted basis. The very few that do are lucky and become “popular” to all investors. This allows them to either raise their fees or grow their funds – both result in a decline in performance for their clients. Thus, at best, finding the “right” institutional investor to speculate for you, will only generate benefits for a limited amount of time. This is unlikely to be worthwhile.

Choosing the best

At the end of the day, no one can time the market and retail investors have the tendencies to react to stale news and sometimes irrelevant news.

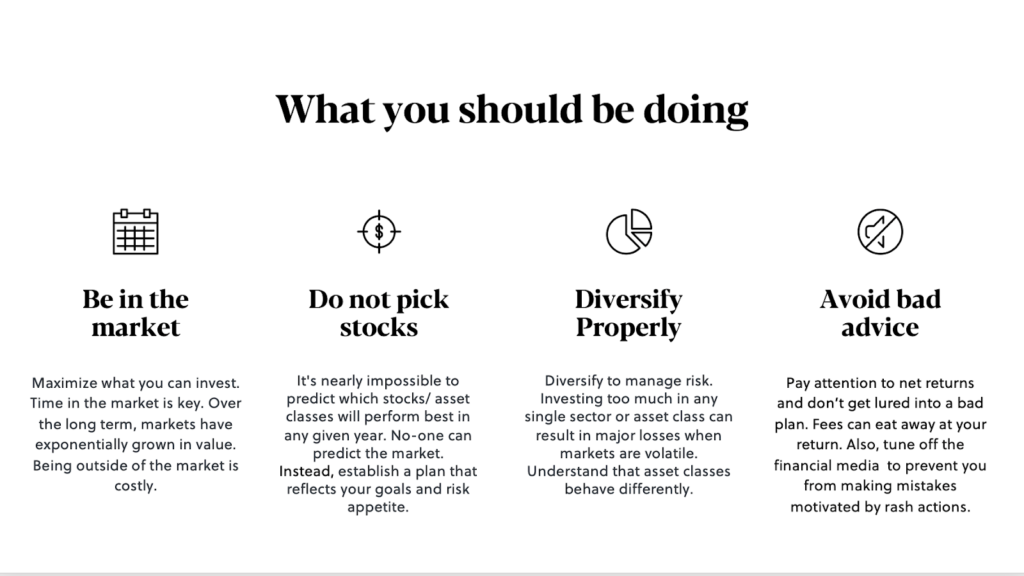

So if you should not actively trade what can you do? Does Diversification work?

There is a fundamental difference between diversification and speculation. The benefits and importance of diversification is a finding that is agreed on in the academic circles: it adds value to the investors. As we discussed before, competition between different events erodes the effectiveness of speculation. This does not apply to diversification. My ability to benefit from diversification is not harmed by other people diversifying. You can even make the argument that diversification for everyone makes it even more effective.

But how to properly diversify?

Proper diversification requires taking into account different factors in a unified approach and tracking:

- The best risk-return combinations available in financial markets: We do this by using principles from modern financial economics, along with statistics and mathematical optimization, to determine which portfolios offer the best such combinations.

- The risk bearing capacity of the client: This is a function of their natural level of risk tolerance, their short- and medium-term liquidity needs, their investment horizon.

Do retail investors do this well on their own?

The reality is that they do not. Many fail to recognize the benefits of diversification. Meanwhile, those who do often do it wrong. For instance, they incorrectly believe that diversification is about holding many assets but forget that it should mean holding “complementary” assets with low correlation to each other. They also fail to rebalance their portfolios over time which leads to portfolios becoming progressively less well-diversified over time.

Do all forms of financial advice fix this?

The simple answer again is: NO. Research shows that the same customer gets very different financial advice from different advisors. At the same time, a given financial advisor gives far too similar advice to their different customers… even if those customers are very different. You will see much less link between equity exposure and risk tolerance and very little variation with age – even though almost any diversification advice recommends lowering exposure to equities as you get older. Evidence also suggests that different styles of advice by financial advisors stem from these advisors’ own biases. Clients invest similarly to their advisors, which leads to correlation in their investment performance.

What’s the take on Mutual Funds and traditional advice?

There exists long literature on the underperformance of Actively-Traded Mutual Funds as a group. Very few mutual funds beat a passive index and, among those that do, most were luck based. In his research, Barras et al. (2010) found that less than 1% of mutual funds have the skill to beat the market, 75% of mutual funds have no skill… and 24% have “negative skill”!

The reason explained behind why so many professionals sell these services is: market forces (Berk and Green, JPE, 2004): Investors “compete” for services of the best investment manager out there, making ‘good funds’ raise their fees and grow larger. Evidence shows that as a fund grows larger its performance suffers (Hong et al., AER, 2004) and performance doesn’t persist or scale.

Timing the market: Does it work?

Dr. Jiro

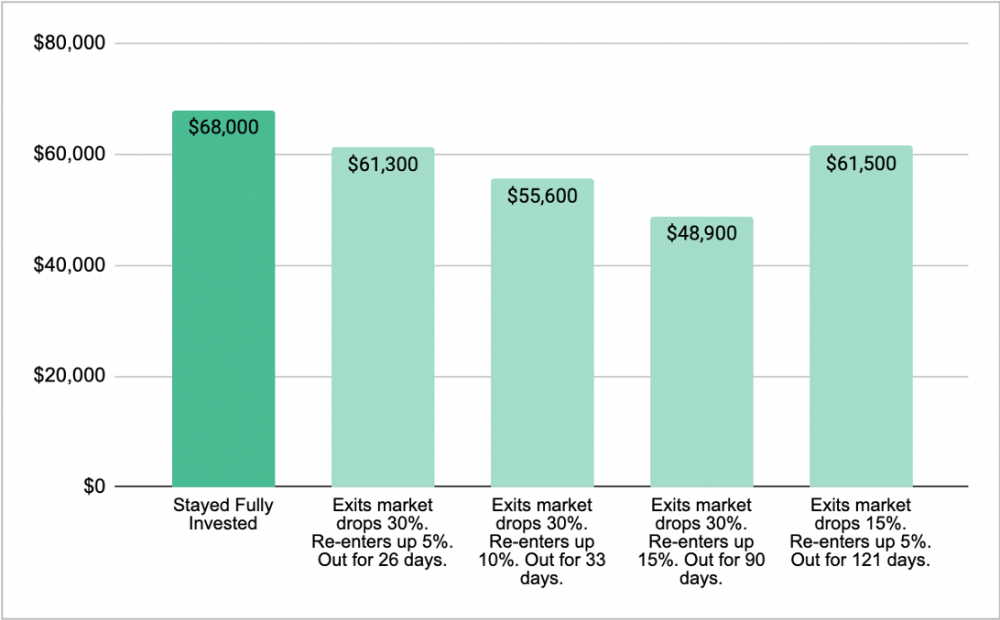

Given the current market environment, we wanted to look into the actual return data ourselves and assess some of the natural market timing strategies. Sarwa analyzed an initial investment of $10,000 in 1990 with zero additional contribution and what that investment would be worth today under different ‘market timing’ strategies.

The simple strategy of just staying fully invested throughout beats the ‘timing the market’ strategies explored.

There is no cherry picking. The data showed that you lose on your growth percentage by moving in and out of the market. In some cases, the difference in performance is substantial. For instance, the market timing strategy that exits when the market drops by 30% and re-enters following a run up of 10%, you would earn 21.5% less. This major shortfall occurs despite only being out of the market for 33 days – highlighting how exiting the market for even a short period of time can greatly harm investment performance.

We’ve looked at several other investment periods as well (e.g., post-1970, post-World War II, post-2000) and similar results arise. Our conclusion: at best, market timing does not work and is based on speculation and luck.

If you sell during a downturn, you actually realize your losses. More generally, history suggests that being out of the market in times of high uncertainty, which follow market downturns, has been quite costly because it reduces an investor’s ability to benefit from market recoveries. These recoveries usually occur in quick bursts that are unpredictable and almost impossible to time.

Abandoning the course can be costly. Keep calm and keep

Ready to invest in your future?