Last Week’s Highlights…

🤖 Apple Wants its 30% Slice of Profits

Although Apple (AAPL) has embraced cryptocurrencies and NFTs by allowing apps to list and sell tokens in countries where they have licensing to operate, the devil is in the details of its new restrictive rules. The catch? Apps must use Apple’s in-app purchase system to sell NFTs and other related services and “may not include buttons, external links, or other calls to action that direct consumers to purchasing mechanisms other than in-app purchase,” Apple said in a statement. This could potentially renew debates across the crypto and NFT industries. Why? Well, Apple wants its 30% cut, and it’s not leaving much room for debate on whether it’s pushing for a monopoly on profits. Last month, Fortnite developer Epic Games entered a legal battle contesting Apple’s 30% cut on in-game NFT profits. Apple’s making some enemies, and many are ready for a fight.

🎃 Halloween Treats Ending on a High

Spooky costumes, spooky movies, and even spookier prices. Inflation has jacked up the trick-or-treating this year, with products like Skittles, Twix, Reese’s, M&M’s, and many more products experiencing massive price increases. According to US inflation data, the average cost of sweet treats this year increased by 13% in September from the year before. The price of certain brands is soaring far higher than others. According to Bloomberg, “Twix is up a whopping 53%, Skittles has jumped 41%, and Reese’s has risen 35% over last year, according to retail analytics firm, Datasembly.” Inflation has impacted your favourite tasty treats differently in the past via a process called shrinkflation. Shrinkflation happens when products get smaller in weight, size, or quantity while prices stay the same (or even increase) – it’s a cute little marketing strategy that tries to sway consumers into continuously buying products even though inflation might be frightening away affordable prices. Maybe start taking a measuring tape with you to the grocery store?

🛢️Oil Giants with Giant Gains

Major profits are rolling in from Europe’s energy behemoths: the UK-based Shell company (SHLX), and Paris-based TotalEnergies (TTE) raked in almost $10B in profits each. Both companies have doubled their profits this year due to sanctions on Russia in response to its invasion of Ukraine in February. While Shell and Total have almost doubled their earnings, shares of Exxon and Chevron have also increased by 75% and 50% respectively. Although banks and other oil companies see oil demand plateauing before 2030, OPEC+ is quite hopeful about demand and the future prospects of oil (predicting that demand for oil will peak around 2045). As the world moves and changes, maybe the energy sector is one investors should look into a little bit more?

The Big Story: What does the term ‘investor’ truly mean? Re-wiring our understanding

With the holidays just around the corner and consumer spending (about to be) on the rise, most of us will be celebrating discounts, special offers, and the ability to buy more for less. So, why do we intuitively celebrate these discounts in our day-to-day, except when it comes to our portfolio?

Here’s the thing, we know it’s a nerve-wracking experience. And we know that seeing 5 or 6-digit losses in our portfolio incites panic. The secret is everybody feels pain from seeing your portfolio go down. In theory, just because something makes sense doesn’t mean it won’t affect us. We’re not underestimating the impact of loss, but we are trying to understand and quantify it in order to truly understand what “loss” means to an investor.

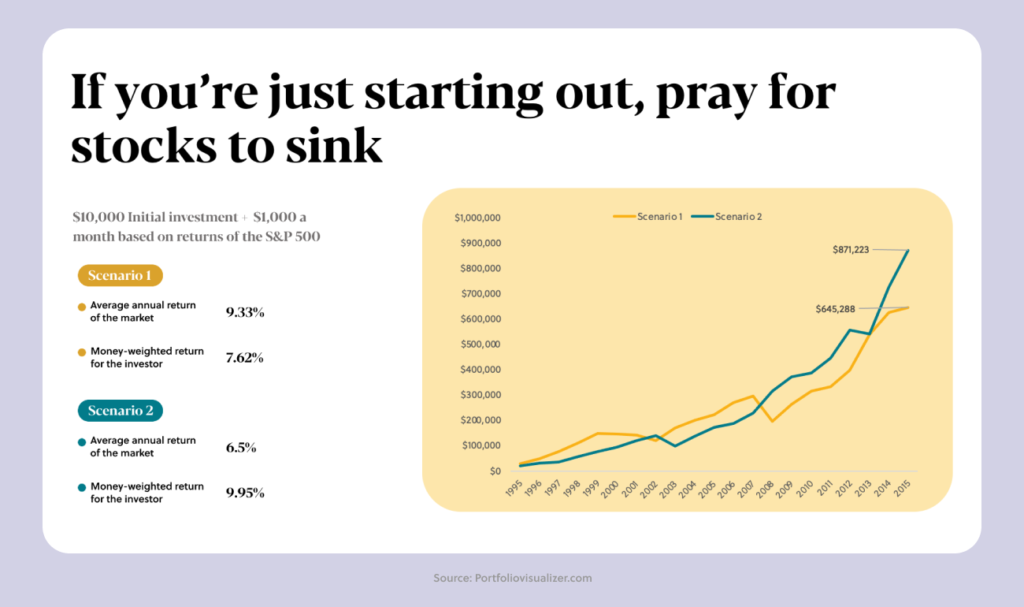

Let’s consider the two scenarios below:

In scenario 1, labelled warm start, stocks are averaging a 9.33% annual return for the next 20 years and soaring for the first three years. In scenario 2, the cold start scenario, stocks are averaging 6.5% per year for 20 years, but they’re dropping for the first three years during that time. If we ask you which of these scenarios you prefer, many investors might consider the answer obvious: scenario 1, right? Well, actually, wrong.

It would be strange for us to consider a stock market drop to be a fantastic benefit to us, but the fact of the matter is that investors win when the stock market drops. What’s intuitive for most investors, especially those relatively new to investing (meaning investors who’ve been investing for 10 years or less), isn’t necessarily what’s good for them or their portfolios. And here’s why.

For one, Warren Buffett says that investors adding money to the markets should much prefer to see the market drop instead of rise, especially, as William Berstein points out when they’re just starting their investment journey.

Here, we see the two different scenarios outlined earlier, with someone who started with an initial investment of $10,000 and dollar-cost averaged $1,000 every month since. In scenario 1, with the annualised return of 9.33% and a warm start, the money-weighted returns (your investor returns) are 7.62% – less than the value of the market’s overall growth in that period.

In scenario 2, however, you can see that the markets made 6.5% annual returns, but your returns as an investor surpassed even the market’s growth in scenario 1. You made an average annualised return of 9.95% in the scenario where markets dropped three years in a row. Boom.

Now, regarding scenario 2, you’re probably asking: how can the market earn a 6.5% yearly return in 20 years when you’ve far surpassed that? This is because, with your dollar-cost averaging approach, this market allowed you to buy a lot more units for much less. When those units ended up recovering, you boosted your personal money-weighted returns.

As an investor, you need to start thinking of yourself as a collector of market assets. When you invest in a global portfolio, you are buying businesses. When the prices of those businesses are low, corporate earnings are still rising over time. So, eventually, when that market recovers, your portfolio is going to soar.

To learn more about how to make your portfolio soar, check out the webinar we did with Andrew Hallam (as the above topic was an example discussed in his book Millionaire Expat) here.