Here’s a question: When the stock market is up or down in a month as much as it could be in a year, who has the patience to think rationally about long-term retirement planning?

People get excited when they see positive interest earnings on their investments. There’s no doubt that it is tempting to withdraw the balance of your interest as soon as it is earned. But, there is an opportunity to make a lot more money by reinvesting those earnings instead of withdrawing them. It’s not about how much money you can take from your investment portfolio. It’s about focusing on what financial planning can do to increase your total wealth – and your quality of life.

Many new investors believe that they lose the opportunity to earn money if they do not move any short-term profits made on their investments into their bank account before an inevitable dip in the performance of their funds. This misconception causes investors to miss out in more ways than one!

Time and interest: The keys to long-term gains

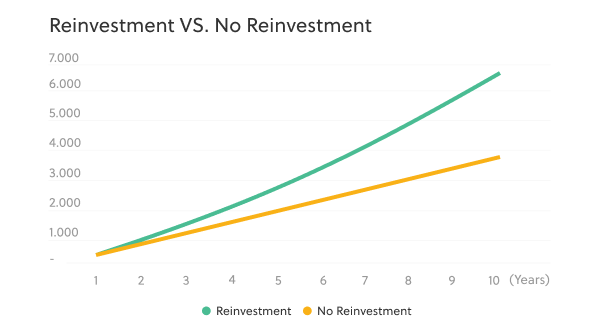

Albert Einstein once said that “compound interest is the 8th wonder of the world” – or so the legend says. This is the concept of interest earning interest on itself. When put into practice, the benefits of an investment continuously reinvesting overtime allows investors to maximize their gains. The longer someone is able to stay in the market then the more compounding periods they’ll undertake and the interest accumulation accelerates. Graphically, the difference between reinvesting interest and not doing so is clear:

Still not convinced? Let’s consider a hypothetical scenario and see if you’re still tempted to immediately withdraw or instead side with reinvestment. A savvy investor decided to invest a sum of $10,000 for 10 years. He is earning a net return of 7% (compounded annually). Here are the calculations:

You’ll see that the investment grows from $10,000 to $21,049. That’s more than double your money for simply letting it sit quietly in a separate account! Alternatively, if our (not so) savvy investor had withdrawn the $700 interest each year, he would have pocketed $7,000 over the 10 year period. Combine this with his initial principal of $10,000, gives him a total sum of $17,000. This is $4,000 less than what was achieved by reinvesting all of the interest as it was earned. Oh yes. It’s time to get comfortable with staying invested!

Cost of living erodes your wealth

If you choose to take money out of your investment portfolio, you’ll likely be faced with two options.

- Spend it or;

- Keep it in a bank account, and overtime it will slowly be eroded by inflation

Inflation averages around 2-3% per year. This means that your $1,000 cash saving, in 10 years, will only be worth around $780! Earning interest on your money is the only way to combat inflation. If you withdraw interest every time it’s earned then it won’t compound to fight off the ongoing inflationary impacts. Being patient and leaving your money parked is wise and the most effective way to invest. As Warren Buffet says, “the stock market is a device for transferring money from the impatient to the patient.”

So, when can you withdraw from your portfolio?

Knowing when to sell out of your portfolio is key to financial success. However, whether you should sell or hold mostly depends on your AGE. If you’re closer to (or at) retirement age, then you’ve likely been investing for a while. So, you can start to sell your investments to live off of for your retirement. Although, if you’re younger there are only two good reasons to withdraw:

- You need money for an emergency

- You achieved a specific goal

For the readers that are already approaching retirement and thinking about an exit strategy, you want to figure three things out. How much money you’ll need, when you’re going to need it and how to make it last. Imagine if we all knew exactly when we’d ‘kick the bucket’. We could ensure that we spent our last dollar at the same time. Actually, maybe that’s a grave thought. However, thinking about this for a moment is considerably better than running out of money before you run out of time. So, how do we work out a safe withdrawal rate?

Bengen’s 4% rule

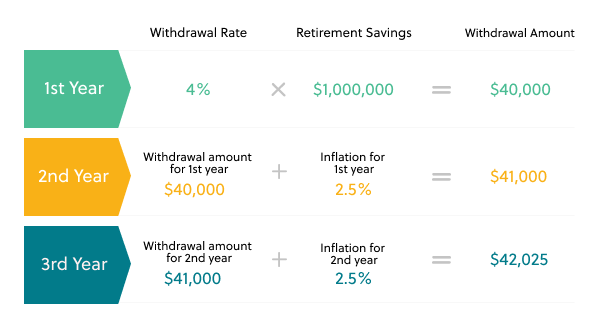

Retirement experts suggest William P. Bengen’s 4% rule to ensure you don’t run out of money. It’s a simple idea created in 1994. Using historical data on stock and bond returns over a 50-year period: A retiree can withdraw 4% from their investment portfolio each year and the amount adjusts annually for inflation. Let’s see this in action: Samer has $1,000,000 in retirement savings and plans to retire at age 65. Here’s how much he could look to withdraw each year:

However, times have changed and retirement can last for more than 25 years. Your situation could also look different. For example, you may wish to travel in the early years of retirement and therefore require larger withdrawals than that of later years. [Rather than take this rule as the absolute truth, you should use it as a handy guideline for planning whilst taking other factors into account.] The 4% rule is a handy guideline but should be adjusted based on factors that impact your personal situation. There are factors that you can’t control – like how long you live, inflation, market returns. Other factors, you can control – such as your retirement age and investment risk-level.

What your retirement time horizon looks like

The good news is that retirees today are living more active lifestyles and living longer than ever before! Although, the longer you live, the more you risk outliving your savings. One of the biggest factors that affects how much you can withdraw from your investment portfolio is how many years of retirement you plan to fund from your savings.

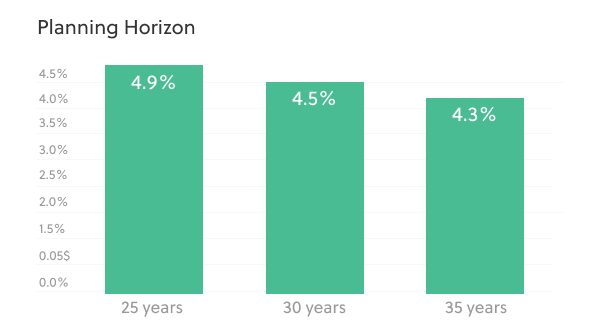

As we’ve seen, historical research shows that if you plan a retirement of 25 years then a 4% withdrawal rate should ensure that you don’t run out of money. But if you work longer – maybe you expect to continue working until 70 and plan on a shorter retirement then you could afford to take a higher withdrawal rate of 5%. On the other hand, like most of us, if you want to retire earlier then you may need to plan for a 35 year retirement and therefore need to consider a 3% withdrawal rate.

Depending on how much you earn on your investments and how much you withdraw from these assets each year, you will either eventually spend all of your money or have remaining assets available for legacy potential. The takeaway here is that the longer your retirement lasts, the lower the safe withdrawal rate.

Your risk tolerance

Most of us are familiar with the term “Low-risk, low-return versus high-risk, high-return.” When you start saving towards retirement in your younger years you may decide to look at higher risk investments, like equities. This type of investment can sometimes lose value, but when retirement is more than 30 years away, you have the time in the market to recover your losses.

However, the closer people get to retirement, typically their focus shifts towards capital preservation over potential returns. This means that by the time you’re in your mid-to-late fifties, you may want to consider looking at lower-risk options, like bonds. It’s important to keep your portfolio in line with your risk tolerance and time horizon as you want to avoid selling at a loss when you need a withdrawal. Dialing down your risk-level should provide you with the confidence for a more reliable safe withdrawal rate as your investments will not be exposed to the same price swings that come with a stock portfolio.