So I’m still young, I’m still figuring out my career, I don’t have any major responsibilities yet. Why should I start investing right now? Why should I have an additional thing I need to save for?

According to Jabbour, there are two reasons why there’s no time like the present. “Number one, there’s no savings culture in the UAE,” he says. “And what I mean by that is that companies don’t offer pension plans at all. Here it’s tax-free money, you do what you want, you’re using what you have, and no one’s sitting there constantly talking about savings and making you put money aside. People have a lot of cash just sitting there. From a finance perspective, that is the worst thing you can do. If you’re parking it in cash, you’re losing money because it’s not keeping up with inflation. Year over year, your money’s value starts to go down if it’s just staying put and not gaining any returns, especially as the dollar starts to inflate. So one main reason to start now is the simple ideology that if you’re not investing, then you’re losing money.”

It’s helpful to think of investing in the same way you’d think about flossing. You know it’s important, you know you should do it consistently, and yet… “No one does it, until you get a root canal and you’re like, oh my God, I’m going to floss every day so this never happens again! But creating that sense of urgency is difficult,” Jabbour says. But while flossing is a chore that stops bad things from happening to your teeth, consistent investing lets you reap much more satisfying rewards.

What is the actual impact of starting now?

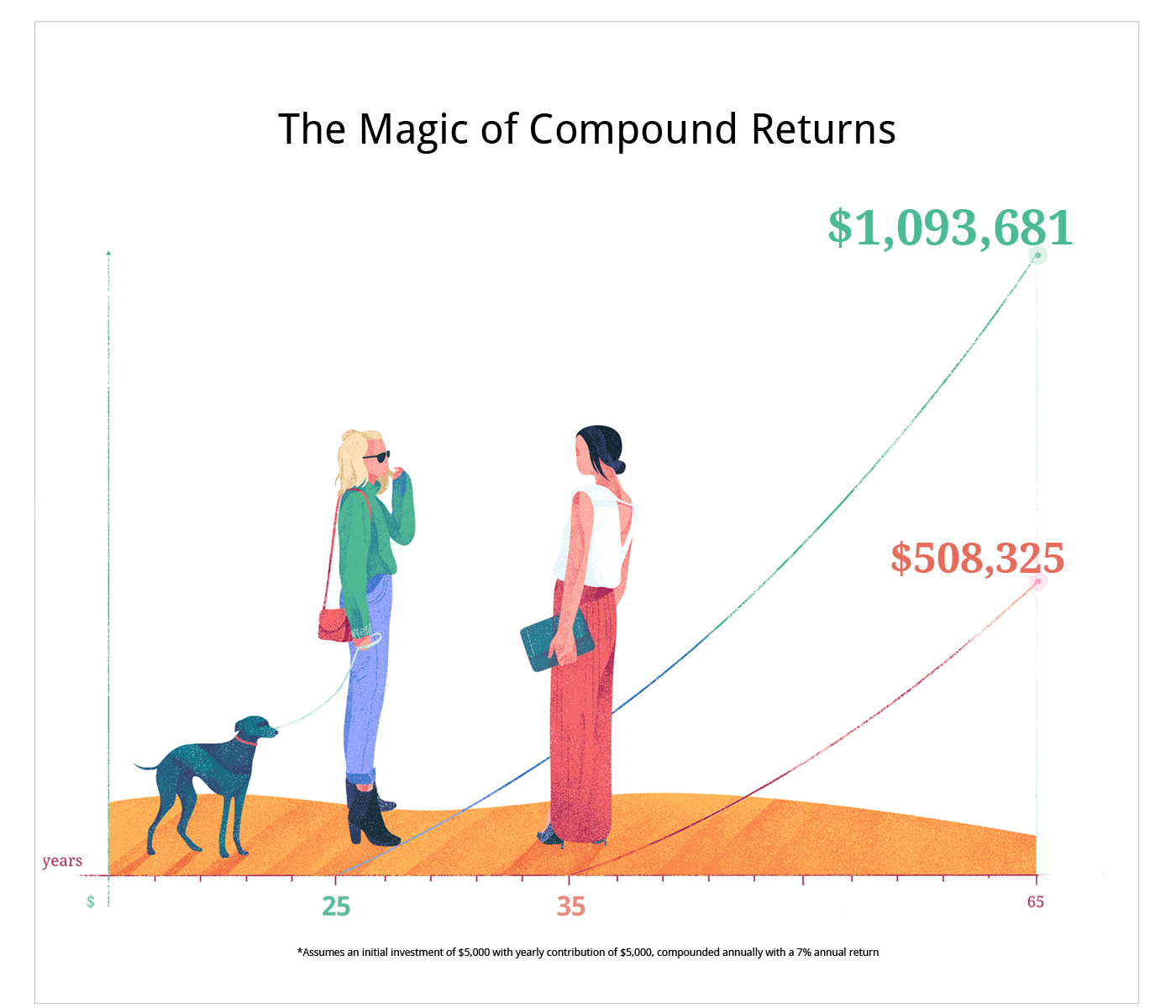

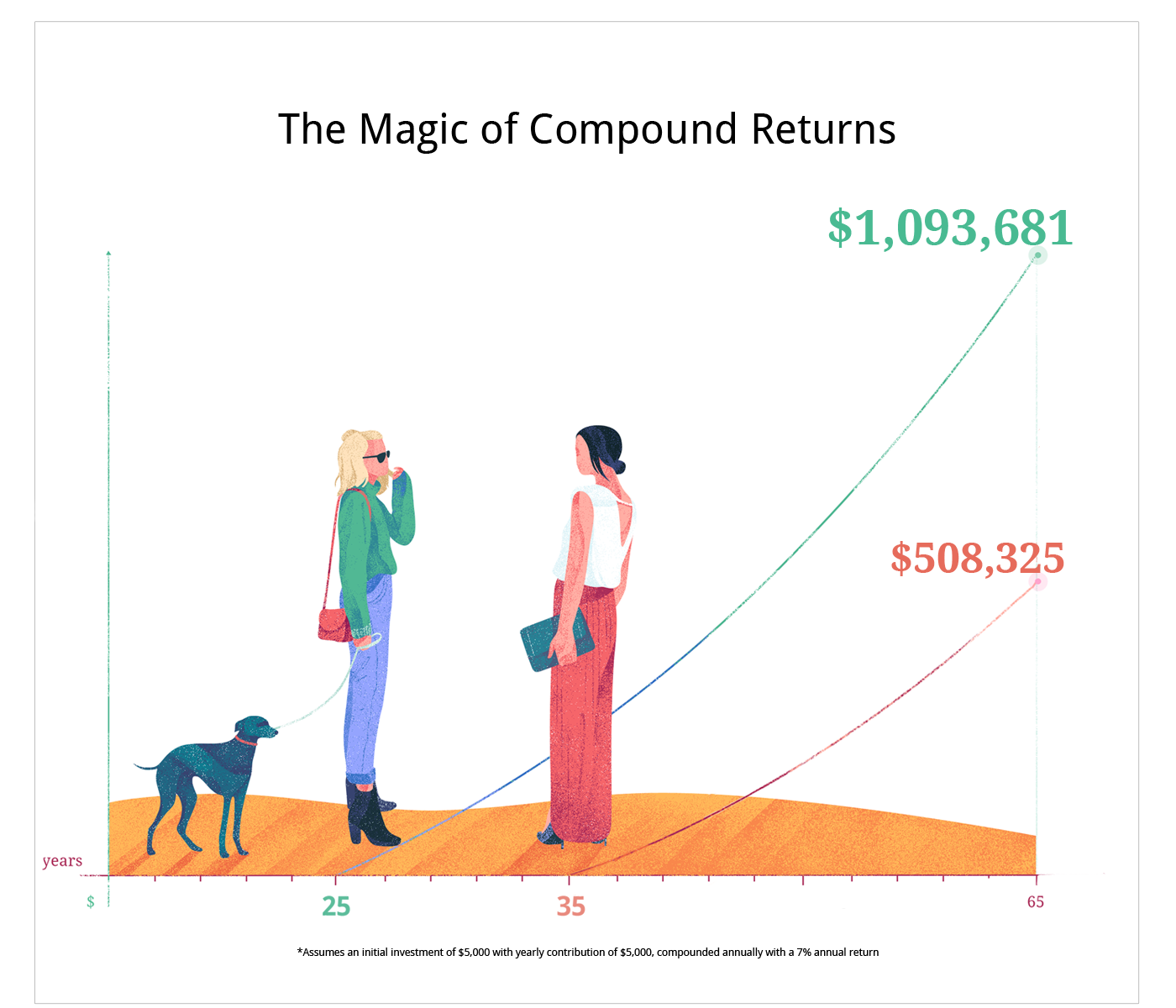

“So Albert Einstein – pretty smart guy – he’s quoted as saying that the eighth wonder of the world is compound interest. Thanks to compounding, someone who is starting to save the same exact amount in their 20s is going to have significantly more money than someone who started to save a substantial amount more in their 30s,” he explains.

Take two friends: Alia starts investing $5,000 a year at the age of 25, and Sara starts investing the same amount at the age of 35. They both retire at 65. this $50,000 invested over the years ($5,000 x 10 years) will translate to a difference of $500,000+ between the two!

This is the magic of compounding and the importance of starting as soon as possible.

So even if you’re just 26 and investing the occasional $100 a month that you’d be spending on something like dinners out anyway, the greater your benefits will be in the long run. You think $100 can get you a nice meal? Think about what several thousand dollars can do for you thirty years down the line.

This all sounds great. But I know nothing about the stock markets! Don’t I have to be some sort of market wizard to make this whole thing worthwhile?

Absolutely not, Jabbour says. And it’s the job of companies like Sarwa to help navigate the confusing waters of the stock markets. “We want to change this ideology that finance and investing is this really complicated thing. At the end of the day, the one concept you need to understand is diversification,” he explains. Diversification is basically the concept of not putting all your eggs in one basket.

Instead, “you want to spread your money out across so many different investment instruments and companies. Otherwise, if you’re trying to time the market, if you’re trying to pick what’s going to do the best, you might as well go put money on a roulette table. No one knows.”

So no, you don’t have to be the next Gordon Gekko in order to benefit from the market. In fact, Jabbour insists that the best kind of investors are passive investors. “A dead person does better at investing than someone living,” he jokes. “Because if both have the same portfolios, a dead person is going to do better. Because they don’t touch it. They don’t react to the news saying something is going to happen. They don’t react to the market tanking one day, one week, one month. They hold tight. And if they’re diversified, they’re going to be fine in the long run!”

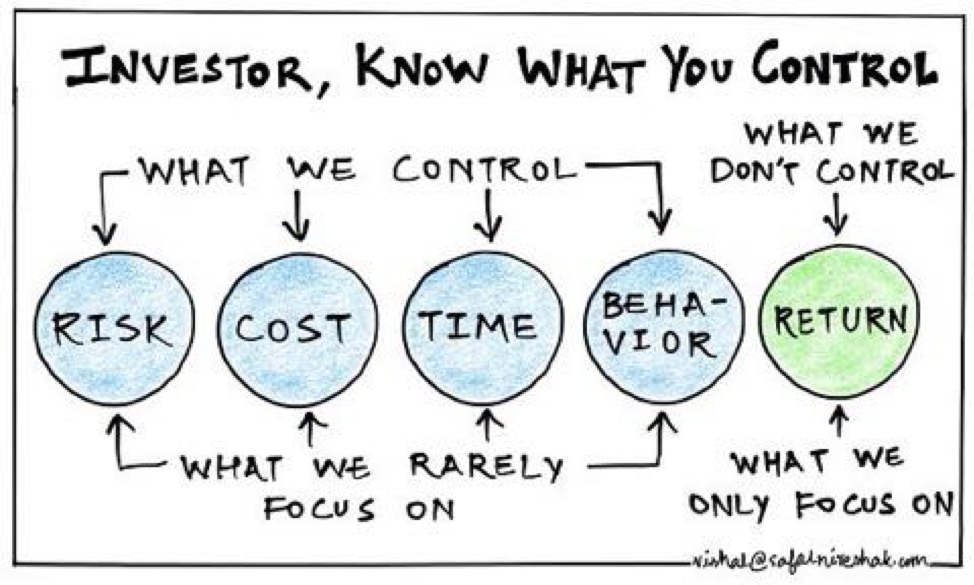

Instead of trying to game the market by rushing to buy fad assets like Bitcoin and selling them in a panic when prices start to drop, a passive investor focuses on the four things Jabbour says they can actually control: “Their risk, the cost, the time that they’re going to be investing, and their behavior. What you can’t control is how the market is going to do, and the returns that are going to happen. No one has any control over that. The four things that I told you that we can control are the things that people think least about, and returns are what people think the most about. All you can do is take care of the things you can control, and the rest is going to happen, but as long as you strap in your seatbelt, you’re going to be fine.”

So tell me more about these diversified portfolios you create.

Sarwa’s portfolios are customized to fit each client’s unique risk tolerance. The portfolio’s themselves consist of ETFs, Exchange Traded Funds. “All they need to know is that they are the most efficient way to achieve diversification,” Jabbour says. “These funds have hundreds, if not thousands, of securities within them. So bonds, stocks, commodities, real estate assets. And they’re fully diversified, meaning they’re giving you full exposure to the global economy.

So there you have it. Investing doesn’t have to be this scary, confusing thing that’s only accessible to a select few. And if you think that maybe the time to start investing is now (spoiler, it is!), try us out!

Ready to invest in your future?