Estimated reading time: 5 minutes

The Case for Going All-In

There’s a question worth asking every growth-focused investor: what is the cost of playing it safe? More investors today are asking a more direct version of that question: should I be in a 100% equity portfolio if my goal is long-term growth?

Everyone says they want higher returns, but the reality is that fewer people are comfortable with what it actually takes to get them.

Over the past few years, I’ve had countless conversations with clients about portfolio risk. There is a consistent pattern. In calm markets, most investors lean toward growth. But when volatility shows up, the same portfolios suddenly feel too aggressive.

That gap between what we think we can handle and what we can actually stick with is where most long-term outcomes are decided.

Which brings me to an interesting shift we’ve been seeing. More investors, especially those with longer time horizons, are asking themselves why they’d hold bonds at all if the goal is long-term growth.

Introducing the 7/7 Aggressive Portfolio

This month, Sarwa launched the aggressive 7/7 Risk Level Portfolio, our highest risk level that allocates 100% of capital towards equities.

It’s already live across four portfolio types: Conventional, SRI, Conventional Crypto, and SRI Crypto.

100% Equity Portfolio vs Bonds: What Actually Changes?

Historically, the role of bonds has been clear. Reduce volatility, provide stability, and generate income. But that stability comes at an opportunity cost. Over long periods, equities have consistently outperformed bonds, and even small allocations to lower-return assets can meaningfully drag on compounding. In practical terms, that “small” allocation matters more than it seems.

The 7/7 Aggressive removes it entirely. All capital is now allocated to US equities, VTI for Conventional portfolios and SUSA for SRI, across all four tracks.

A portfolio that is 94% equities and 6% bonds behaves differently from one that is fully invested in equities, for both returns and in how quickly it recovers. During strong rebounds, fully invested portfolios tend to regain losses faster, while more diversified portfolios take longer to catch up.

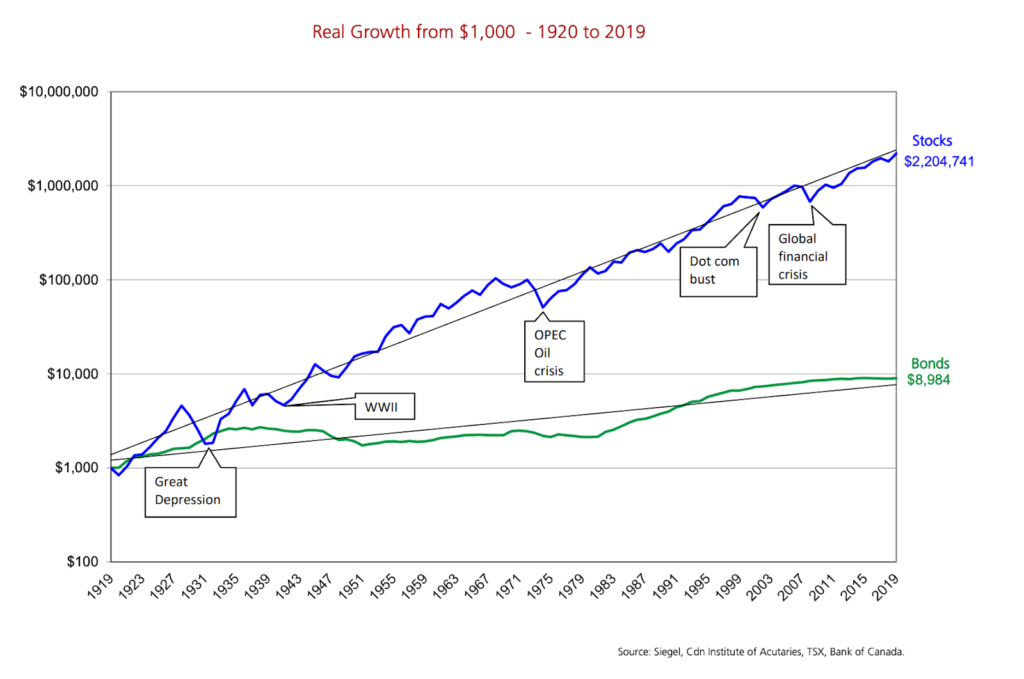

The graph below helps illustrate this more clearly. Over long periods, the difference between being fully invested in equities versus partially allocated to bonds is not marginal. It compounds into a materially different outcome.

Why US Equities, and Why Now

The US equity market is the dominant force in global investing. The US represents 64.6% of the MSCI ACWI Index, the broadest measure of global equity markets. When you hold US equities, you’re holding the largest, most liquid, most researched slice of the global economy.

Long-term economic trends continue to support this. US markets have historically outperformed bonds over multi-decade horizons by a significant margin. The data isn’t ambiguous. For investors measured in decades, not months, equities are where wealth is built.

The 2020 recovery was an example of how this played out. Portfolios completely invested in equities rebounded faster than those weighed down by bond allocations. When markets snapped back, growth portfolios captured the full upside. Diversified portfolios with bonds recovered, but slower.

Should You Invest 100% in Equities?

Going all-in on equities comes with a clear trade-off, and we won’t obscure it.

Short-term volatility will be higher. Market swings will feel larger. In a down year, the 7/7 will fall further than a blended portfolio, but that’s the mechanism that makes higher returns possible over the longer time horizon. Periods of uncertainty will feel more uncomfortable. And unlike more balanced portfolios, there is no built-in cushion to soften those movements.

For some investors, that trade-off is worth it. Especially if:

- Their time horizon is 10+ years

- They are consistently contributing, not withdrawing

- They are comfortable seeing short-term losses without panic selling

The question is not whether equities outperform over time, because we know they do, it is whether you can stay invested long enough (through that discomfort) to benefit from that outperformance.

Is This Your Portfolio?

The 7/7 Aggressive risk level is not for everyone. It’s for investors who know they can handle the volatility. It’s for those of you who understand that the price of maximum long-term growth is short-term discomfort, and who know this won’t burden them emotionally.

The reality is that a smoother experience can actually lead to better outcomes. Not because of how it performs on paper, but because it is easier to stick with.

And that is the part that often gets overlooked.

The best portfolio is the one you can hold through uncertainty without second-guessing yourself, even if that isn’t the one with the highest expected return.

Check out How to Choose the Right Investment Strategy for You for more in-depth insights.

In that sense, a 100% equity portfolio is actually a behavioral commitment. Because in the end, long-term investing is about staying in the game long enough for those returns to compound.

Visit our FAQ page to compare the various portfolio types across risk levels.

Key Takeaways

- Investors often underestimate the long-term cost of avoiding a 100% equity portfolio, especially during market volatility.

- The 7/7 Aggressive Portfolio allocates 100% to US equities, removing bonds to maximise long-term growth potential.

- Historically, equities outperform bonds significantly, leading to faster recovery during market rebounds.

- Going all-in on equities carries short-term volatility risks, which is manageable for those with a long investment horizon.

- The right portfolio is one that investors can maintain through uncertainty, prioritizing behavioral commitment to stay invested.