To build wealth consistently over the long term, investors need a strong strategy, and one of best such strategies is the Systematic Investment Plan (SIP). But what is an SIP and how exactly can it help investors build wealth?

Simply put, the SIP is a strategic and systematic plan that helps investors achieve their financial goals slowly and steadily.

As we all know, forming good habits requires some work. That’s true of exercise, starting a diet, and even the way that you save and invest money. As aviation pioneer Antoine de Saint-Exupéry famously said: “A goal without a plan is just a wish.”

That’s also true of investing. If you don’t make a plan that sets out how and when you’re going to invest, you’ll struggle to hit your financial goals.

Today, one of the most tried and tested ways to invest successfully is with an SIP, which in many ways practically applies the long-term investing principles set out in the Nobel-prize winning Modern Portfolio Theory, as well as the benefits that come with consistent lump-sum investing.

In this article, we will consider what a SIP is and how it can help you build wealth and achieve your financial goals over time. We’ll cover:

- What is an SIP investment plan?

- How SIP works

- What are the benefits of SIP

- Are SIP plans safe?

[Do you want to create an SIP that will help you achieve your financial goals? Register with Sarwa to get you started.]

1. What is an SIP investment plan?

A Strategic Investment Plan (SIP) is a financial planning tool whereby investors can build long-term wealth by consistently and regularly investing a definite amount of money in an investment portfolio.

Let’s unpack this definition by considering some of its elements.

Consistency and regularity

First, an SIP involves consistency and regularity. For example, Mr. Ahmed, using an SIP, can invest AED 1,000 at the end of every month while Mrs. Yusuf, using an SIP, can invest AED 2,000 on the 15th day of every month.

While their investment plans are different, they have the two common characteristics that make them both an SIP – consistency and regularity.

To emphasise the importance of these two elements, let’s contrast the examples above with others.

If Mr. James invests AED 1,000 in one month and then invests AED 3,000 some three months and 15 days after and then another AED 2,000 a month after, what he is doing does not qualify as an SIP. Suppose Mrs. James also invests AED 5,000 in January and then AED 10,000 in December; what she is doing does not also qualify as SIP.

In all the above examples, only Mr. Ahmed and Mrs. Yusuf are deploying a SIP.

Definite amount

Notice also that apart from investing at a regular interval – every end of the month or 15th day of the month – Mr. Ahmed and Mrs. Yusuf are also investing a definite amount – AED 1,000 and 2,000, respectively. It’s about creating a habit, through regular recurring amounts, sort of like auto-deposits.

This is also crucial to identifying an investment system as an SIP.

An investment portfolio

Since SIP is consistent and regular, investors in such plans should have an investment portfolio they regularly invest into.

Most SIP investors embrace passive investing, whereby they invest their definite amount consistently and regularly into a passive portfolio of index funds or ETFs. They can do this through a digital wealth manager such as Sarwa Invest that creates portfolios specifically designed to achieve an investor’s goals, given their unique risk tolerance, time horizon, and current financial situation.

[For more on how to become a successful passive investor in the UAE, read “How to Invest Money In The UAE: All You Need To Know”]

However, there are also SIP investors who embrace active investing. These types of investors prefer to create their own portfolios by actively buying and selling stocks and ETFs in a bid to achieve their financial goals. They can do this through trading apps such as Sarwa Trade, which allows investors to trade stocks and ETFs at zero commission.

[For more on how to be a successful active investor in the UAE, read “How to Buy US Stocks in the UAE (The Easy and Commission Free Way)”]

Long-term wealth building

Building wealth slowly and steadily is the sure way to become rich without being a victim of market timing or unscrupulous investment fads.

An SIP ensures that you’ll be committed to this slow and steady approach to investing. Instead of chasing fads, an SIP investor commits funds consistently and regularly to a well-crafted investment portfolio.

How does an SIP differ from a DCA?

Those who have read our article on dollar-cost averaging (DCA) may wonder how it differs from an SIP.

In that article, we emphasised that DCA is a strategy where someone who has a lump sum at hand (say AED 100,000) decides to invest that lump sum systematically over an extended period of time (say AED 10,000 at the end of every month for the next 10 months). This also involves a definite amount invested consistently and regularly until the lump sum is exhausted.

However, with an SIP, the investor does not set aside total investable income for periodic investments. Instead, the investor is setting aside a portion of their regular income and investing that portion consistently in the market.

In this way, the SIP investor follows what is called lump-sum investing, by investing the total investable income they have at their disposal on regular intervals (usually every month).

The SIP investor is not worried about putting a lump sum in the market at once; rather, they are concerned about investing their regular income systematically.

For example, Mr. Ahmed does not have AED 12,000 at once at the beginning of the year; instead, he is removing AED 1,000 every month from the salary he earns.

Therefore, while the two systems enjoy some of the same benefits, the mindset differs with SIP because it is used in the form of a long-term investment strategy.

2. How SIP works

Compound interest is the engine that drives an SIP.

To ask what is an SIP is to ask what is compounding. Simply put, compounding is the process where money earns extra money and that extra money earns extra money, ad infinitum.

The extra money that money earns is referred to as compound interest. An interest is compound, rather than simple, if it also earns additional interest that also earns additional interest.

This compounding effect is the engine of wealth building. Albert Einstein famously called it “the eighth wonder of the world”.

But how does it relate to SIP?

SIP encourages investors to invest regularly and consistently in the market, which allows them to earn more compound interest over time.

Similarly, SIP encourages the use of lump-sum investing, which is a strategy that guides investors to put all their investable cash into the market immediately (usually every month after being paid a salary), rather than spreading out the same amount over longer periods.

By doing this, investors can spend more time in the market, earning maximum potential compound interest.

Let’s take an example to explain the two points above. The person who invests AED 5,000 at the end of January is better positioned than the one who invests that same amount as AED 500 every month for the next 10 months.

Why?

The former starts earning compound interest on AED 5,000 from the get-go, while the latter only earns compound returns on AED 500. By the end of October, the former would have accumulated potentially more returns by way of compound interest (if there was a bull market). And since the market rises more than it falls (see below), this scenario is more likely than the alternative.

However, the person who invests AED 5,000 is even better positioned than the one who invests AED 5,000 in January and then another in July. The regular and consistent investor would have acquired more compound returns month in, month out, compared to the one who only invests twice in a year.

The SIP investor is the one who invests AED 5,000 every month. In the scenarios above, he is the one best positioned to earn maximum returns from the market.

3. What are the benefits of SIP

Having identified how SIP works, let’s now consider some of its benefits.

- Compound interest: As we saw in the previous section, an SIP creates more potential wealth-building channels through compounding than other unsystematic investment systems.

- Opportunity for protection in a bear market: Because an SIP involves a definite amount that is consistently and regularly invested, it offers some similar benefits to dollar-cost averaging (DCA). One of these is mitigated losses in a bear market.

- Opportunity to gain long-term exposure benefits: Instead of holding on to your cash and investing a part of it regularly, SIP promotes lump-sum investing – investing all you have to invest at once. With this approach, the SIP investor spends more time in the market, earning maximum compound interest from the get-go rather than delaying and waiting for a more “opportune” time.

- Takes away emotional investing: According to Warren Buffett, there are two emotional hindrances to successful investing: fear and greed. Fear occurs in bear markets when prices are falling, and greed occurs in bull markets when prices are rising. While the former leads people to sell at a loss, the latter leads people to buy just when the market is due for a correction.

With SIP, this fear and greed cycle can be escaped. SIP investors, as we have seen, can better handle bear markets instead of being afraid. Also, bull markets provide opportunities for them to earn compound interest on all their wealth-generating channels.

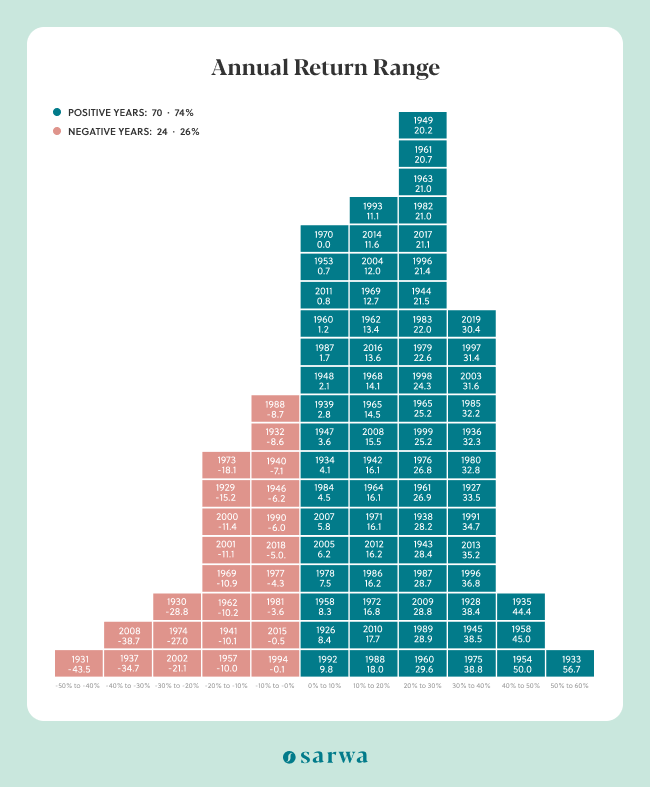

Also, since SIP investors are focused on the long term and the market rises more than it falls (as the graph below shows), they can be relaxed and confident in a strategy while others are fearful or greedy.

Performance of the CRSP US total stock market index between 1926 and 2019

As the graph above shows, between 1926 and 2019, the market rose 74% of the time and only fell 26% of the time. The SIP investor who was committed to the long term would have thus benefited over this time period.

- Builds the discipline needed for successful investing: A commitment to a strategic plan helps investors build the discipline they need to achieve their financial goals.

If we only invest when we feel like it, we won’t do much because spending is more natural than investing. But with an SIP, we gain control over our finances by investing consistently and regularly.

SIP investors who use passive investing can even deploy automatic investing (a service available with Sarwa Invest), which ensures that a definite amount is immediately deducted from their accounts into their investment portfolios on the specified date.

4. Are SIP plans safe?

When it comes to the safety of SIP plans, there are three important things to consider:

Time in the market reduces risk

SIP plans take away emotion out of investing. Instead of worrying about how the market performs this month or the next, the SIP investor keeps committing a definite amount to the market consistently and regularly. But is this safe, especially when the market is falling?

For one, we have already noted that SIP investors (like DCA investors) can find more protection in the bear market in a way (by getting more shares for the same amount over a period of downturn).

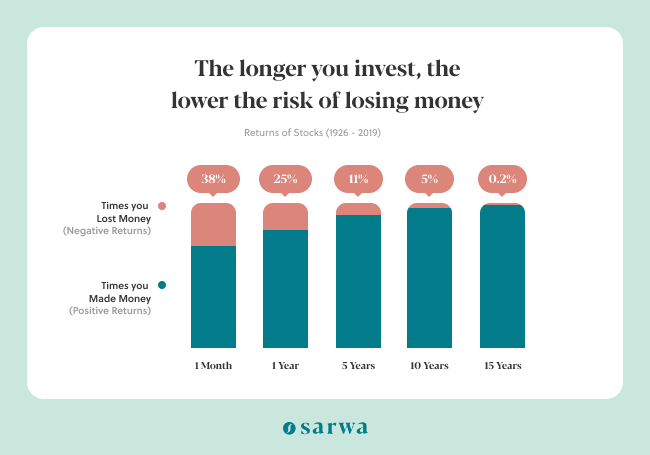

The second point to be made is that the more time an investor spends in the market, the less their overall risk of losing money. Consequently, by staying in the market for the long term, SIP investors can remain calm about intermediate volatility and instead focus on the end goal.

As the chart below shows, investors who stayed only a month in the market, at any time between 1926 and 2019, had a 38% chance of losing money. At the far end, those who stayed in the market for 15 years, at any time between 1926 and 2019, had only a 0.2% chance of losing money.

As we saw above, the market went up 74% of the time between 1926 and 2019.

So, investing consistently in the market without considering the current state of market volatility will be profitable in the long term. In this way, SIP offers a strategy to do so.

Use a reputable digital wealth manager

While some SIP investors prefer to create their own portfolios, others prefer to invest in a portfolio created by a digital wealth manager who has the knowledge, expertise, and experience in creating asset allocations.

If you are in the latter group, you’ll need a reputable digital wealth manager that will create a portfolio well attuned to your unique financial goals, risk tolerance, and time horizon.

Also, you’ll need a digital wealth manager that embraces broad diversification in portfolio construction, has a system for automating your investment, a responsive customer service, anda process for rebalancing your portfolio to stay in tune with your goals.

These and more are what Sarwa Invest provides.

If you go the active investing way, you’ll need a trading app that is commission free, safe, allows fractional trading, and has no minimum investment requirement.

Look to Sarwa Trade for those services.

[Now that you know what SIPs are and how they can benefit you, it’s time to consider creating your own SIP portfolio. Are you unsure how to start? Schedule a free call with a Sarwa Wealth Advisor and we’ll be glad to guide you through the process.]

Takeaways

- SIP involves investing a definite amount consistently and regularly into an investment portfolio for the long term.

- Compounding is the engine that drives SIP and makes it profitable.

- SIP helps to take away emotional investing as investors focus on the long term benefits of compounding.

- SIPs are safe because the market rises more than it falls and time spent in the market reduces the risk of losing money.

- SIPs can be profitable for both passive and active investors.