Across the world, the rise of digital wealth management sites and apps has revolutionised how so many people understand money.

The experience has had the positive effect of making investing more accessible and lower cost to more people than ever before.

Truly remarkable is the fact that digital wealth managers like Sarwa now allow accounts to be opened starting at just $5.

Today, making financial tools accessible has made way for even more revolutionary services.

Digital wealth managers are bringing once-elitist financial services within the grasp of all by making investing and financial advisory more digitalised and personalised, work that has greatly transformed how new investors experience the power of wealth creation.

Now, wealth management is no longer just for the mega-rich.

However, many people still don’t take full advantage of the now ultra-accessible digital wealth management services out there.

Some continue to (wrongly) equate digital wealth management to traditional brokerage services or exclusive investment advisory firms.

Yet, a closer look will show that digital wealth management is a broader service than just an investment brokerage or advisory offering many of the prerequisite tools that the average person needs to build wealth.

In this article, we unearth everything you need to know about how digital wealth management has evolved to become the open and accessible service it is today, finally arriving at the emerging technology-driven services that now define robo advisors.

To jump directly into what is digital wealth management without the background info (though we recommend you understand this for context), click on section 3 below.

- Wealth management hits the mainstream (a brief history)

- The rise of digital wealth management

- What is digital wealth management?

- Modern Portfolio Theory

- Portfolio Diversification

- Low-Cost Investing

- Automated Investment

- Portfolio Rebalancing

- Automatic Dividend Reinvesting

- Connect to a host of financial experts

- Data and Communication

- Safety and Regulations

- How robo advisors can help you

1. Wealth management hits the mainstream (a brief history)

Understanding how wealth management hit the global mainstream requires a review of how defined-contribution retirement plans eclipsed defined-benefit plans.

A defined-benefit plan is a pension plan where a worker gets a definite amount of money, either as an annuity or a lump-sum payment, upon retirement. Importantly, a defined-benefit plan is employer-sponsored — meaning that the employer is responsible for managing the funds and bearing any investment risk.

Under this plan, employers have a defined formula that considers the length of employment and salary history to calculate how much pension payment an employee can expect upon retirement.

Because it is employer-sponsored, the employer has to ensure the employee gets the calculated pension payment.

Defined-benefit plans were the mainstream retirement plans across much of the world for a long period. However, in 1978, the defined-contribution plan arose as an alternative option that became quickly popular.

In a defined-contribution plan, the employee contributes to the plan from their salary.

The employee is also responsible for selecting investments within the plan from a given menu.

Unlike the defined-benefit plan that was employer-sponsored, the defined-contribution plan put the responsibility on the employee.

Also, the employee does not expect a defined, fixed pension payment at retirement; what he/she gets at retirement depends on how much he/she contributes and how well the chosen investment plan performs.

Over the years, defined-contribution plans overtook defined-benefits plans and became the mainstream retirement plan.

One of the major consequences of this change is that workers who did not know anything about investments or investment management (since the employers previously handled it all) now had to choose the right investments.

Consequently, the need for personalised wealth management services boomed.

Flash forward to today: Now the average worker — not only the rich — needs to be properly educated to make the right investment decisions, which will inevitably have major impacts on when he/she retires.

Put simply, wealth management has become mainstream.

2. The rise of digital wealth management

Defined-benefit plans began to lose popularity due to their inability to meet up with the money they ‘promised’ employees at retirement.

Market returns were sometimes lower than expected, and many of these funds became insolvent — that is, they did not have enough cash to pay retirees.

This problem came to the fore during and after the global financial crisis of 2008/2009.

More than $5.4 trillion was lost in 2008 across OECD (Organization for Economic Co-operation and Development) countries.

The financial crisis would then increase the adoption of defined-contribution plans, further mainstreaming a wealth management trend that was already well underway.

In the beginning, most of the defined-contribution plans invested in mutual funds. Wealth managers had the job of helping employees choose the right mix of mutual funds that would build their retirement nest.

A mutual fund is a pool of money from many retail investors that are invested in stocks (equity mutual funds), bonds (bond mutual funds), fixed-income instruments (income mutual funds), etc. under the supervision of professional money managers.

An investor with a portfolio of mutual funds will have some of his money in stocks (equity mutual funds) for their high returns, bonds (bonds mutual funds) for their low risk, and fixed-income instruments (income mutual funds) for regular income.

Mutual funds are actively traded (buy and sell regularly) by professional traders who time the market in an attempt to help investors outperform the market.

Since stocks provide the highest returns, a mutual fund’s ability to outperform the market depends on how well their equity funds can outperform the market.

However, the continued underperformance of mutual funds, relative to the market, began to raise doubts about their ability to give retirees the returns they sought.

In 2019, an incredible 70% of domestic equity funds (mutual funds that invested in the stock market) underperformed their benchmarks.

For the tenth year running (2010-2019), 71% of large-cap mutual funds (mutual funds that invested in the stocks of large-cap companies) also underperformed their benchmarks.

Over five years (2015-2019), 82.29% of large-cap equity funds, 78.38% of equity-linked savings schemes, and 40.91% of mid/small-cap equity funds underperformed their benchmarks.

The problem is that investing in mutual funds is expensive. In a bid to outperform the market (which they hardly do, as stated above), they charge high management fees and incur higher taxes.

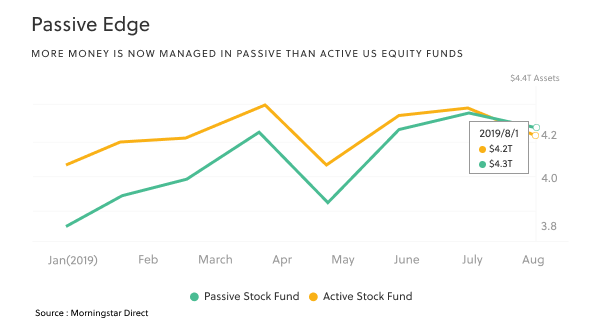

The continuous underperformance of mutual funds led to an interest in passive investing as an alternative investment philosophy.

In passive investing, the investor seeks to match a certain index’s performance (instead of beating the market). Consequently, passive funds are cheaper — as a result of lower fees and lower taxes — and have been proven to provide better long-term returns.

[Read “What is the Difference Between Active and Passive Investment” to learn more]

Passive investing got its start with the creation of The Vanguard Group in 1975 by John Bogle.

But the constant underperformance of mutual funds (especially considering their high cost) increased the appetite for passive investing over the past decade.

The chart below shows how passive stock funds have now overtaken active stock funds.

Vanguard Group, now widely considered the pioneer is passive investing, founded by John Bogle, became the second-largest investment house in the world in 2019.

Digital wealth management arose from the popularity of indexing and passive investing.

All of sudden, there was a growing demand for wealth managers to bring the benefits of indexing and passive investing to the average investor.

3. What is digital wealth management?

Put simply, digital wealth management is the use of financial technology, big data and artificial intelligence, and risk management to provide digital financial and investment services to a wide range of customers.

Over the past decade, the shift from active investing to passive investing meant that there was more demand for investments to be automated.

Technology-first wealth managers, commonly known as robo advisors, began to automate investing with financial technology, eliminating the need for frequent direct contact between investors and wealth managers — and importantly cutting out emotions from the investing experience.

But how do digital wealth managers such as technology-first robo advisor do this?

The anatomy of a robo advisor

1. The Modern Portfolio Theory

One of the most important developments that made passive investing possible is the Modern Portfolio Theory.

Harry Markowitz developed this Nobel Prize-winning theory in 1952 to help investors understand the place of risk in investing.

Before Markowitz, investors focused almost exclusively on the potential returns of an investment. Then Markowitz introduced a way for investors to quantify and measure the risk of their investments in addition to returns, proposing that people are more likely to be risk-averse than was previously thought.

According to MPT, the most important goal in investing is to maximise return for a given level of risk and minimise risk for a given level of return.

Since return and risk are measurable, wealth managers can determine the risk/return relationship of a portfolio and choose the optimal investments to achieve the right balance for the investor — maximise return for a given level of risk and minimise risk for a given level of return.

Every portfolio that achieves this balance is called an efficient portfolio.

Consequently, digital wealth managers and the robo advisories they serve use the MPT to create efficient portfolios tailored to unique risk tolerance levels.

So whatever personal level of risk you are comfortable with, there is an efficient portfolio that a digital wealth manager can create for you.

For example, Sarwa uses the MPT to create asset allocations that maximise returns for numerous different risk-tolerance profiles, defined as conservative, moderate conservative, balanced, moderate growth, and growth investors.

Whatever your level of risk tolerance is, it is the job of digital wealth management teams to help you discover it and build your portfolio around it.

2. Portfolio Diversification

Since most investors are naturally risk-averse, according to Markowitz, they don’t want to lose money.

As it would turn out, most wealth managers ended up prioritizing ways to minimise their clients’ risk irrespective of their risk tolerance.

Markowitz discovered that the risk of a portfolio (basket) of assets that are not positively correlated (that is, they are not directly linked by the same factors) is lower than the risk of any one asset in that portfolio.

In essence, that means that by having a portfolio of non-positively-correlated assets, an investor can reduce his/her risk exposure.

This is the technical explanation of what is commonly called portfolio diversification, a strategy that is today widely understood to be the best way to minimise risk and protect investors’ money.

The efficient portfolio is also (naturally) a diversified portfolio.

In the case of Sarwa, digital wealth managers work with investors to create a diversified portfolio of low-cost ETFs from the most reputable investment houses, such as Vanguard, BlackRock and Franklin Templeton.

Sarwa uses ETFs because they are low-cost, traded on the exchange market like stocks, and diverse (allowing for many options for diversification).

[Watch “Simplifying Investing: Diversification and ETFs” to understand more about ETFs and diversification]

3. Low-Cost Investment

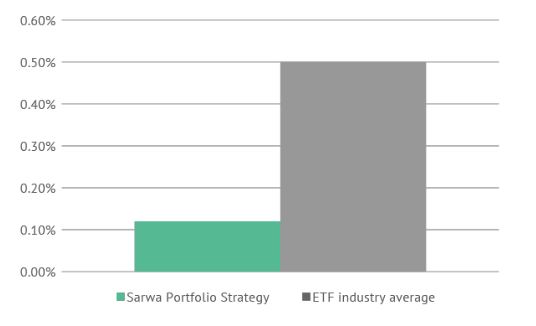

As a modern robo advisor, Sarwa also seeks to reduce the cost of investing to the barest minimum by choosing low-cost ETFs or index funds.

Sarwa even outdoes other robo advisors by investing in the most low-cost ETFs compared with other digital wealth managers.

In the chart below, you’ll see the average asset-weighted expense ratio of Sarwa’s portfolio strategy is far lower (0.12%) than the ETF industry’s average (0.50%).

Robo advisors reduce the cost of investing by passing on these lower fees to their investors, providing an accessible entry to investing that is much lower compared to traditional financial advisors.

For example, Sarwa charges an advisory fee of between 0.5% and 0.85%, which is less than half of the average fee in the Middle-East financial advisory industry (2%).

4. Automated Investment

Robo advisors provide a technological spin on investing by allowing investors to put their portfolio on auto pilot.

This helps to encourage a healthy habit of sustained, on-schedule investments, before you are tempted to spend the money on anything else.

“Do not save what is left after spending, but spend what is left after saving,” wisely said Warren Buffett. In other words, take out your savings for investment from your income before spending it on anything else.

Robo advisors help you achieve this through automation — the platform automatically takes money from your account on a particular date.

Automated investment is also great for people who prefer dollar-cost averaging (DCA).

While lump-sum investing is better, investors with less confidence in the market may prefer to choose DCA.

Those who do prefer DCA can benefit from putting their investments on automatic schedules.

5. Portfolio Rebalancing

Markowitz’s Modern Portfolio Theory shined the way forward for how robo advisors today create efficient portfolios for investors.

However, once the portfolio is operative, its structure begins to change as some assets grow in value and others fall.

When this happens, the portfolio deviates from an efficient portfolio (your target mix of investments), which is not optimal.

For example, suppose an efficient portfolio has 50% of its investment in VOO (Vanguard S&P 500 ETF), 30% in BND (Vanguard Total Bond Market ETF), and 20% in VNQ (Vanguard Real Estate ETF).

Let’s assume that at the end of a particular week, the portfolio’s structure has changed to 60%:20%:20%. Now the portfolio is no longer efficient for this investor.

Through emerging financial technology, Sarwa’s platform automatically rebalances portfolios to ensure that the investment is always efficient.

6. Automatic Dividend Reinvesting

The major advantage of investing is the compounding effect of money. That is, money earns compound returns when you keep reinvesting the returns it generates.

Digital wealth managers that you connect with at Sarwa give you the option to reinvest the dividends from your portfolio automatically.

So if you choose this option, all dividends generated by your investments are reinvested in a way that maintains the structure of your efficient portfolio.

By automatically reinvesting your dividends, you can continue to earn compound returns.

7. Connect to a host of financial experts

All the above can make it seem like robo advisors are all technology and automation.

But this is far from the truth! Robo advisors have a host of financial experts working behind the scenes who manage and oversee the technical and academic aspects of financial advisory.

However, unlike active fund managers, robo advisors don’t have their experts working to timing the market by conducting daily trades.

Instead, their finance experts aim to provide low-cost advisory that is accessible to all and without the high risks of day trading.

For example, Sarwa has a team of former Merrill Lynch, UBS, Accenture, and Goldman Sachs employees.

Sarwa also has team members who have chaired the board of J.P. Morgan Chase Switzerland and other banks.

Mark Chawan, the CEO, is a former employee at Accenture, while Robin Harb, Sarwa’s Head of Strategy, is a former employee at McKinsey and Co.

Sarwa also has investment experts and board advisors with decades of experience in the finance industry.

Dr Jiro Kondo, the Head of Portfolio Construction, is an Assistant Professor at McGill University, Canada.

Moreover, Sarwa has ambassadors who are public figures and industry leaders. One such ambassador is Karl Tlais, Senior Director at Visa.

8. Data and Communication

First and foremost, digital wealth managers rely on understanding your financial situation and risk tolerance before setting out to create an efficient portfolio.

To do this, they require new clients to fill out a questionnaire. Some robo advisors also rely on artificial intelligence to learn about customer’s behaviour and promote the solutions that will best help them.

Sarwa requires every new customer to answer a questionnaire, through which the wealth associate team will be able to understand your unique needs, goals and personal risk tolerance.

Sarwa uses the latest in behavioural economics research to identify your risk tolerance with just a few questions (rather than a list of 20-30 questions).

Furthermore, Sarwa regularly communicates with investors to determine if anything has occurred that has changed your risk tolerance.

To make interactions more social and convenient, digital wealth managers at Sarwa also have various other channels where they communicate with customers, answer questions, and attend to concerns.

9. Safety and Regulations

As with any digital financial platform, the security of the customer is paramount.

With digital wealth managers, the security concerns are two-fold: the security of your data and money.

To this end, digital wealth management requires adherence to strict financial regulatory standards designed to protect the customers.

Sarwa, for example, is regulated by the Dubai Financial Advisory Services (DFAS) and the Financial Services Regulatory Authority of Abu Dhabi (FSRA). Regular audits are also carried out as part of the regulatory process.

One of the main regulatory requirements is the separation of the digital wealth manager’s assets from the clients’ by using another financial institution as a custodian of clients’ assets (Sarwa uses Saxo Bank in Denmark, in this case).

Some digital wealth managers like Sarwa also have Professional Indemnity Insurance as an added level of security.

On the data side, Sarwa, like other digital wealth managers, use 256-bit encryption, backups, and firewall technology to protect your data.

They also have secured servers and use physical security to verify privacy. Sarwa also employs an external security firm that regularly checks security protocols to ensure conformance to industry standards.

[Read “Is Sarwa Safe: How Sarwa Protects Your Investments?” to learn more about Sarwa’s security protocols]

4. How robo advisors help you

Whether your financial goal is retirement or some big-ticket expense, robo advisors have emerged as the most accessible, low-cost and convenient way to maximise your returns and minimise your risks.

So what are some advantages of hiring a digital wealth management company that offers robo advisory features?

- Low cost: Today, even the average investor who doesn’t have the financial capital of the mega rich can access wealth management at little cost (low fees, low taxes).

- Low risk: By helping you create diversified portfolios, robo advisors reduce risk to the barest minimum.

- Long-term return: Digital wealth managers help you focus on the long-term rather than short-term fluctuations in the market. In addition to helping you nurture a long-term mindset (thus reducing emotional investing), they help you maximise your returns over the long term.

- Accessibility: Most traditional financial advisors have minimum investment requirements that most average investors can’t meet. With Sarwa, you can open an account for as little as $5.

- Personalised and data-driven investing: Digital wealth managers evaluate your financial goals and risk tolerance to construct an efficient portfolio that matches you perfectly. If any of the data changes, they can easily modify your portfolio to create another efficient portfolio.

- Automation: Automated investing and reinvesting can help you get the emotions out of the way while focusing on compounding your investments.

- Easy to use: Robo advisors provide platforms that are easy to use for anyone and everyone.

Takeaways

As the change from defined-benefit plans to defined-contribution plans has mainstreamed wealth management, mutual funds’ failure to outperform the market has mainstreamed digital wealth management.

By using a digital wealth manager, you will get access to:

- Efficient portfolios created based on the Modern Portfolio Theory.

- Automatic rebalancing of your portfolio to keep its efficiency

- A diversified portfolio of index funds or ETFs that minimise your risk

- The opportunity to automate your investment and the re-investment of your dividend

- A host of financial experts that use the best ideas in the industry to help you achieve your goals

- Personalised and data-driven investment strategies that match your goals and risk tolerance

- Regulated and secured investment platform that protects your data and money