Like the regions they reflect, global markets are diverse.

Naturally, then, this diversity can result in diverse outcomes. For discerning investors, comparing and understanding the benefits of global stock exchanges like the London Stock Exchange (LSE) and New York Stock Exchange (NYSE) is important; clearly, which you choose can impact your portfolio’s returns.

The (possibly multi-million) dollar question is: which is the better choice, the LSE vs NYSE?

These two stock exchanges are certainly not similar. They vary by their listing requirements, market capitalisation, and number of listed companies, among other factors.

So, unsurprisingly, there is definitely a difference in the risk and return that the LSE vs NYSE can provide your investment portfolio.

In this article, we will consider the major differences between the LSE and NYSE, ultimately explaining why Sarwa has decided that — at this moment — the NYSE is still the better choice.

We’ll look at:

- ETFs in the LSE and the NYSE

- Why the NYSE benefits investors more than the LSE

- Lower fees

- Higher returns

- Better diversification

- Lower rebalancing costs

- Higher liquidity

- The effects of withholding tax

- The future: why the LSE’s tax advantages can become more significant

While this article examines the current state of things, the evaluation is an ongoing one as various government and inter-government policies continue to affect the conclusions detailed below.

1. ETFs in the LSE and the NYSE: New York, the world’s biggest ETF market

ETFs provide the best opportunity for passive investors to grow their money over the long term. They are low-cost (fees and taxes), high-liquid, low-risk, highly transparent, and flexible investments, helping investors maximise their returns and minimise their risks.

So, as supporters of long-term and passive investors, our main concern is with the performance of ETFs in both stock exchanges.

Unlike mutual funds, ETFs are traded like stocks on the stock exchange market. The LSE and NYSE are two of the stock exchanges where investors can buy and sell ETFs.

The NYSE, located on New York’s Wall Street, is the largest ETF market in the world. At the end of 2018, there were 2,224 ETFs in the United States. On the other hand, at the end of 2018, there were 1,160 ETFs in the United Kingdom.

While the UK had over £230 billion in turnover in 2018, the US had an average daily turnover of $102 billion, of which 20% was in the NYSE.

Consequently, the NYSE is a bigger ETF market than the LSE.

2. Why the NYSE benefits investors more than the LSE

So, does that size of the ETF market affect my return and risk?

Simply put: Yes.

The NYSE is not only a much bigger ETF market than the LSE; it is also a better choice according to numerous performance indicators: lower fees, higher returns, diversification, lower rebalancing costs, and higher liquidity.

1. Fees

ETFs in the UK market have higher fees (expense ratio) than ETFs in the US market.

For example, the iShares Developed Markets Property Yield UCITS ETF (IWDP), a real estate ETF in the UK, has an expense ratio of 0.59%. Its US counterpart, the Vanguard Real Estate ETF (VNQ), has an expense ratio of 0.12%.

Similarly, the iShares Core S&P 500 UCITS ETF (CSPX), an equity ETF in the UK, has an expense ratio of 0.07%. In contrast, the NYSE-listed Vanguard Total Stock Market Index ETF (VTI) has an expense ratio of 0.03%.

On the bond side of things, the iShares US Aggregate Bond UCITS ETF USD (IUAG), a bond ETF in the UK, has an expense ratio of 0.25%, compared to the NYSE-listed Vanguard Total Bond Market Index Fund ETF (BND), which has an expense ratio of 0.03%.

Generally, US ETFs on the NYSE are cheaper than the UK ETFs on the LSE. This is the first advantage the NYSE has over the LSE.

Why should this be important to you?

Fees obviously eat into your returns. For two ETFs exposed to the same assets (same returns before expenses), the investor will earn more returns on the one with the lower fees. Suppose the returns on IWDP and VNQ above are 10%. After deducting expenses, your real return on IWDP is 9.41%, while it is 9.88% on VNQ.

For better real returns (returns after expenses), the NYSE is the better choice over the LSE.

[Want to learn more about Vanguard ETFs? Read this guide to understanding the best Vanguard ETFs for 2021.]

2. Returns

Just like the NYSE is better than the LSE cost-wise, it is also better returns-wise.

For real estate ETFs, the IWDP has a 10-year annualised return of 3.80% and an annualised return from inception of 3.70%. On the other hand, the VNQ has a 10-year annualised return of 8.89% and an annualised return from inception of 8.56%.

Similarly, CSPX has a 5-year annualised return of 15.88% and a 10-year annualised return of 13.46%. In contrast, VTI has a 5-year annualised return of 16.69% and a 10-year annualised return of 13.80%.

Finally, IUAG has a 3-year annualised return of 4.42% and a 5-year annualised return of 2.86%, while BND has a 3-year annualised return of 4.67% and a 5-year annualised return of 3.08%.

So far, data shows that the NYSE is better with returns before expenses, as much as with real returns.

3. Diversification

We have seen that NYSE ETFs are cheaper and provide better returns. However, for investors, risk management is directly linked to the outcome of your returns. It’s not enough to maximise returns; a good investment portfolio must also minimise risk for the given level of returns.

If you have read Warren Buffett, you probably know that “Rule No. 1 is never lose money. Rule No. 2 is never forget Rule No. 1.” Losing money sucks, doesn’t it?

One way to minimise risk is through diversification. The more broadly diversified a portfolio, the less the risk.

How does this affect the LSE versus the NYSE discussion?

The NYSE provides better diversification when compared to the LSE.

This added ability to diversify is important for building portfolios. For example, Sarwa diversifies your portfolio in two major ways: by asset class and by market. In the latter, Sarwa ensures that your investments are not in a single market — having your money in a single market means you are 100% exposed to the risks in that country/region.

Therefore, a Sarwa investor is exposed to the US market, the developed markets, the emerging markets, and the global market.

Such broad diversification helps to minimize risk.

However, while the NYSE has a developed market ETFs like the iShares Core MSCI EAFE ETF (IEFA) that exposes investors to the European, Australasian, and Far Eastern markets, the LSE does not have a counterpart of the IEFA.

Instead, an investor in the LSE has to purchase three ETFs — iShares MSCI Europe Ex-UK UCITS ETF (IEUX), iShares MSCI Japan UCITS ETF (CJPU), and iShares MSCI UK ETF (EWU) — to try and match the diversification the IEFA provides. However, the diversification those three markets provide (Europe and Japan) is not as broad or extensive as the IEFA (Europe, Australasia, and the Far East).

What’s more, with the NYSE trading almost 2X as many ETFs as the LSE, it provides a wider range of options, making it easier to achieve broad diversification.

Do you want to reduce your risk? Then the NYSE provides the means through diversification.

4. Lower rebalancing costs

Every investor has an optimal/efficient portfolio mix that helps him maximise returns and minimise risk for his time horizon and risk tolerance.

To keep maximising returns and minimizsng risk, it’s essential to keep the portfolio mix intact.

However, the portfolio mix often changes based on the performance of the assets that constitute it.

Consider an investor who has a portfolio that is 60% stocks and 40% bonds. If the bonds are decreasing in value and the stocks are increasing in value, the portfolio mix will change – the value of stocks will exceed 60%, and bonds will fall below 40%.

Rebalancing helps restore the portfolio in keeping with the investor’s financial goals, risk tolerance, and time horizon.

How is this relevant to our discussion of LSE vs NYSE?

“The US portfolio will have less rebalancing because the ‘developed world ex-US’ self-rebalances,” said Jiro E. Kondo, Assistant Professor of Finance at McGill University’s Faculty of Management and Head of Portfolio Construction at Sarwa. “Meanwhile, by constructing an alternative to ‘developed world ex-US’ (i.e., IEFA) with three ETFs (UK, Euro ex-UK, and Japan), we have smaller holdings in each and it becomes easier to trigger a rebalance.”

There are two costs to rebalancing a portfolio: capital gains tax and brokerage costs. Rebalancing a portfolio involves selling some investments (the ones who have exceeded their portfolio allocation) and buying others (those who have fallen below their portfolio allocation).

Consequently, the more often you rebalance a portfolio, the higher the cost of rebalancing.

While the IEFA self-rebalances, the three LSE alternatives trigger rebalancing more often, leading to a higher rebalancing cost.

As investors, your goal is to keep costs (that parasite to all portfolios) to the minimum. Hence, the NYSE, which increases your real return by reducing your rebalancing costs, is a better option.

5. Higher liquidity

ETFs trading on the NYSE are more liquid than those trading on the LSE. This should not be surprising since the NYSE is a much bigger market generally and a bigger ETF market specifically.

Liquidity measures how often an asset is traded, which determines how fast an investor can convert such an asset into cash without a loss in its value: the more liquid an asset, the better.

Trading on the NYSE means your investments are more liquid than trading them on the LSE.

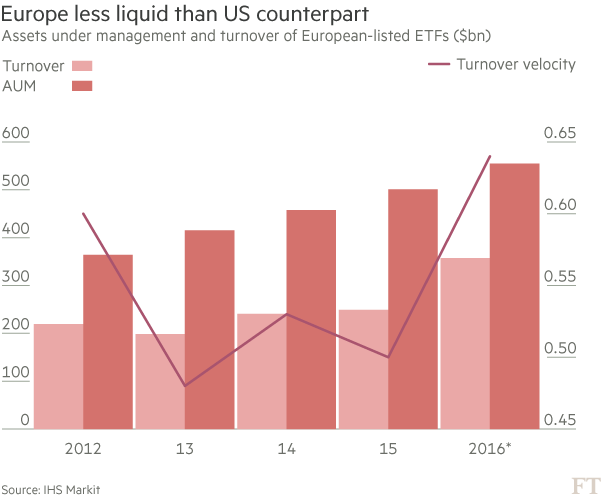

The charts below show the wide difference between liquidity (measured by turnover and turnover ratio) in the US ETF market and the European ETF market from 2012 to 2016.

The entire European market had its highest turnover (just above $500 billion) in 2016. The US lowest turnover in 2013 (just above $4 trillion) is about 8 times the European market’s highest turnover in 2016. And that’s the entire European market, not just the UK (where the LSE operates).

Currently, VTI has an average daily volume of 4.37m trades, while the CSPX has an average volume of 124,250. Similarly, BND has an average daily volume of 5.3m, while IUAG has an average daily volume of 902. Also, VNQ has an average daily volume of 4.5m, while IWDP has an average daily volume of 40,631.

The difference in liquidity is dramatic.

This should concern any discerning investor. The more liquid the market, the easier it is to quickly sell your assets without them losing value due to a long waiting period.

3. The effect of withholding tax

You probably feel like the LSE has no advantage over the NYSE, don’t you? Well, it does have an advantage. It’s a tax advantage.

Before you receive dividends on your stock ETFs/REITs ETFs and interest on your bond ETFs, you are charged a withholding tax (WTH) that varies based on where you live and where the dividend and interest are earned.

A withholding tax is a tax collected when the income is earned rather than when it is received. Governments withhold taxes to reduce tax evasion and increase tax revenue.

Stock/REIT Dividends

As a UAE resident earning dividends in the US, generally speaking, you will be charged a 30% WTH for both US and non-US stocks in your ETF – it doesn’t matter if the stock is a US or non-US stock, as long as you are trading it in the US (through the NYSE).

Alternatively, when you earn dividends through US stocks in your ETFs in the UK (via the LSE), you are generally charged a 15% WTH. And if you earn the dividends through non-US stocks purchased in the UK, you are exempted from WTH.

Put simply, for dividends on US stocks, you are charged 15% in the LSE and 30% in the NYSE, while for dividends on non-US stocks, you are charged 0% in the LSE and 30% in the NYSE.

Bond Interest

Similarly, as a UAE resident, when you earn interest from bonds in the US (NYSE), you will be charged a 30% WTH. However, when you earn interest from bonds in the UK (LSE), you will be charged a 20% WTH.

Note: While Sarwa provides professional investment advice, we do not provide tax-related services. If ever in doubt, we recommend speaking to a tax lawyer.

So why choose NYSE?

It’s clear from the above that purchasing your ETFs in the LSE has tax advantages over purchasing them in the NYSE.

However, Sarwa operates under a corporate account for the NYSE, allowing our clients to no longer be exposed to estate tax on the NYSE.

For this reason, Sarwa prefers the NYSE — it offers clear performance advantages while allowing us to bestow your investments with tax advantages. This effectively takes away the main advantage of the LSE.

4. The future: why the LSE’s tax advantages can become more significant

While Sarwa currently favours the NYSE over the LSE, this is a data-backed position rather than an ideological one.

Therefore, Sarwa is always monitoring the situation to help customers maximise returns and minimise risks. (It’s all about you and your best interests).

For example, the UK and UAE signed a double taxation treaty on April 12, 2016. The treaty currently exempts the following from paying WTH on interest earned in the UK:

- A company whose principal class of shares are substantially and regularly traded on a recognized stock exchange;

- A pension scheme;

- A financial institution which is unrelated to and dealing wholly independently with the payer; and

- Any other company, provided the competent authority determines that its main purpose or one of its main purposes was not to secure the benefits of Article 11 (Interest)

If such a treaty later extends to individuals, it will make the WHT tax advantage of the LSE on interest on bonds (which will then be 0% in the LSE versus 30% in the NYSE) much more significant.

Sarwa is on the lookout for any such changes and is always willing to review its preference for the NYSE if such policy changes occur.

However, you must also remember that the NYSE has two other advantages we didn’t quantify – lower rebalancing costs and higher liquidity – that are also significant for an investor.

Look to this blog to stay updated.

[Now that you learned a bit more about the construction of a portfolio, you can better dive into how to build one from scratch. We produced this popular ultimate guide to portfolio creation that explains exactly how investment allocation is done.]

Takeaways

- The NYSE is a bigger ETF market than the LSE, with more ETFs, greater liquidity, and more assets under management (AUM)

- The advantages of the NYSE over the LSE include lower fees, higher returns, more diversification, lower rebalancing costs, and higher liquidity.

- However, the LSE is better than the NYSE when it comes to WTH on interest and dividends.

- When the advantages of both exchanges are quantified, the NYSE comes out on top.

- While Sarwa currently favours the NYSE because of the above, it will continue evaluating the exchanges and reviewing its preferences.