Discovering exactly what are stocks and bonds as they relate to your investments is like a construction worker learning about bricks.

These assets are quite literally the building blocks of your investment portfolio.

Chances are, you already have at least a basic grasp of these foundational assets. Today there are countless investing channels on YouTube that teach greater familiarity of what stocks and bonds are.

But just subscribing to a YouTuber — unfortunate as it is! — hardly guarantees many viewers will clearly understand just how to use stocks and bonds for their long-term benefit.

While YouTubers often talk about stocks and bonds, this is different from truly learning exactly how they work and — most importantly — how they impact your portfolio’s returns. To do this, you’ll need to take a more comprehensive, in-depth look at stocks and bonds.

To start, the right mix of stocks and bonds support one of the core principles of smart investing — diversification. It is important to keep a certain percentage of stocks and bonds in your portfolio, and this is broken down into an allocation formula that matches your risk profile, such as 60%-40% or 50%-50% splits.

Indeed, a proper understanding of how bonds and stocks affect your portfolio will help you make more accurate investment decisions.

In this article, we help you understand how stocks and bonds impact your portfolio by answering the following questions:

- What is a stock?

- What is a bond?

- How do stocks and bonds complement each other in a diversified portfolio?

- How do you achieve broad diversification with stocks and bonds?

- How can you build a diversified portfolio of stocks and bonds?

At the end of this article, you will not only know what stocks and bonds are, but also understand them enough to be able to make better financial decisions.

So, to start off, what exactly are stocks and bonds?

1. What is a stock?

A stock is a security/investment asset that represents a portion of ownership in a publicly traded company.

When companies try to raise money from the public, they offer some portion of their ownership to investors.

So in exchange for giving part of your money to the company, they give you a portion of ownership in the company in the form of shares. Your stock is the sum of all the shares you have in a company.

Let’s take Microsoft as an example.

At the moment, Microsoft (MSFT) has 7.53 billion outstanding shares. This means that the ownership of Microsoft is divided into 7.53 billion pieces.

To own a part of Microsoft, you can decide to buy 1,000 of these shares, for example — but you can buy one and still be a shareholder.

To own a stock in a company, all you need do is enter the stock exchange through a broker and place a buy order for the number of shares you want to own in the company.

The broker executes the order and you are given a share certificate as a proof of ownership.

Since investors don’t spend money without expecting to make more (who doesn’t want more money), the question is how do you make money from having a portion of ownership in a company?

[Looking to buy and trade stocks? Sarwa has just launched Sarwa Trade, a simple, accessible, and affordable stock trading platform where you can purchase stocks with zero commission.]

Making money with stocks

There are two ways shareholders make money with the stock of a company:

Dividend payment

When a company aggregates all the money they got from the purchase of their shares, they invest it in their operations or in a capital investment.

Whenever the company declares profit, they may decide to set aside a portion of their income as dividend and pay to their shareholders according to the number of shares they hold. Dividends are always declared per share.

For example, Microsoft’s next dividend payment is $2.24 per share; so for your 1,000 shares, you can expect to receive $2,240.

Companies that pay dividends do so every quarter (4 times in a year).

The beauty of stocks is that you will continue to receive dividends, for as long as the company decides to pay it, and for as long as you hold the stock.

For example, if you hold your Microsoft stock for 30 years, you will continue to earn dividends 4 times every year for 30 years.

But why would a company refuse to pay dividends (and deny you that cool $2,240)?

Stock Appreciation

Answering that question requires a grasp of the second way stocks help investors make money: stock appreciation.

When a company manages its funds well and earns income from its investments and operations, it becomes more appealing to investors. As earnings increase (among other performance indicators), more investors will want to have their money in such a company.

As demand for the company’s stock increases, the price of a share increases.

For example, if you bought Microsoft’s stock on January 15, 2021, you would have purchased it at $212.65. If you sold it on May 10, 2021, you would have sold it for $252.46. For a single share, you would have earned $39.81. For 1,000 shares, you would have earned $39,810 in just 4 months (not bad, right?).

Let’s go back one year and see how this profit can increase.

Now suppose you bought the shares on May 1, 2020, just about a year ago, at $174.57. If you sold it on May 10, 2021, you would have earned $77.89 for one share. For those 1,000 shares, you would have earned $77,890 in just 12 months.

This is why some companies refuse to pay dividends.

Instead of paying dividends, they choose to reinvest that money to further improve the company’s earnings. The higher the earnings, the greater the demand; the greater the demand, the higher the share price; the higher the share price, the more money the investor makes and more appealing the company’s stock becomes.

However, paying dividends and growing share prices are not mutually exclusive — there are still many companies like Microsoft who grow their share price quite well and still manage to pay dividends.

In this regard, we can break down stocks into the following categories:

- Dividend stocks: Stocks of companies who prioritise paying dividends and growing dividend per share.

- Growth stocks: Stocks of companies who prioritise growing their share prices

- Value stocks: Stocks whose prices are lesser than their perceived intrinsic value. Since prices will move towards the intrinsic value over time, these stocks have great opportunities for appreciation in price.

- Speculative stocks: These are stocks with uncertain fundamental prospects (and high volatility) that traders buy due to their potentials to earn significant returns. Since these stocks lack fundamental prospects, there can also be an extreme loss. The trader is merely hoping that things go his way.

- Defensive stocks: These are stocks of companies that are resistant to the uncertainties of the general economy. These stocks are stable and solid even in uncertain times.

- Blue-chip stocks: They are stocks of companies with large-cap and high financial stability. These companies are usually the leaders in their industry.

What are the benefits of stocks to an investor?

Why are stocks so popular?

Why is it that every investor has most likely heard about stocks even when they don’t have a firm grasp about them?

High returns

The first benefit of stocks is the high returns on investment (the $77,890 return on Microsoft above probably got your attention!).

In the example above, within a year, Microsoft’s stock price grew by 44.6%. In the past five years, the stock has grown from $46.9425 to $252.46, a 437.8% increase (!) and an annualised return of 87.5% per year.

That’s tremendous returns to say the least (who wouldn’t want to grow their money at that rate?)

However, not every stock will perform like Microsoft’s.

A better way to see the returns that stocks provide is to look at a stock index — they track the performance of a number of stocks instead of just a single stock.

The S&P 500 index, for example, tracks the performance of the top 500 stocks (by market capitalisation) in the US.

The S&P 500 has grown by 106.80% in the past five years, at an annualised return of 21.36%.

To keep this in perspective, the best you can earn in a savings account in UAE is an annualised return of 1.75%. The latest 50-year bond issued by the Federal Government has a yield of 2.7%. And the highest average gross yield in the property market is 8.32%.

Stocks offer an unparalleled return opportunity, right?

Compound Interest

The second benefit of stocks is that you can reinvest your dividends and earn compound interest.

If you have stocks in companies that pay dividends, you can reinvest those dividends in the same company or other companies to earn more returns on them. With this, every return you generate will also continue to generate returns, which means your money can grow even more.

“Returns matter a lot. It’s our capital,” said Abigail Johnson, American billionaire and businesswoman.

Perhaps no one has better captured the importance of returns as opportunities to earn compound interest. Every return becomes a capital that earns more returns.

[To learn more about the importance of compound interest for your investments, read “Dollar-Cost Averaging vs Lump-Sum Investing: How Should You Invest”]

Grow with the economy

When the economy grows, companies perform better and report higher earnings.

As companies’ earnings improve, their stock prices increase. The more the stock prices grow, the more money you can make. By investing in stocks, you can gain from the growth in the economy.

The downsides of stocks

You have probably heard the cliche: everything that has an advantage has a disadvantage. Well, sadly, that cliche applies to stocks.

Stocks do have certain downsides and disadvantages (sorry to break your heart).

High volatility and high risk

Just as a stock can grow in value at a high rate, it can also fall in value at a high rate. Just think of that $77,890 above if it was a loss!

Experts call this volatility.

Volatility measures how much a statistical variable can change rapidly or in an unpredictable fashion. A common measure of volatility in finance is standard deviation, which measures how much a variable deviates from the mean. The greater the standard deviation, the higher the volatility.

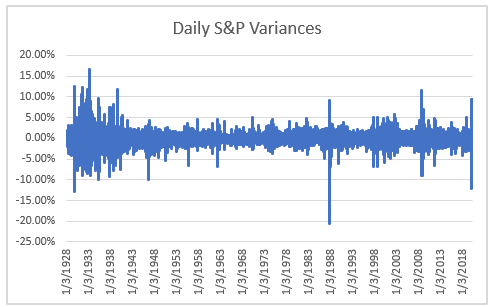

Stocks are very volatile, and as much as prices can move up speedily, they can go down just as fast.

The chart below shows the S&P 500 daily volatility for some selected days between 1928 and 2018.

Source: E-investing For Beginners

In 10 of these days (52.6%), the S&P 500 experienced a double-figure volatility (more than 10%).

In another chart showing the yearly volatility, the S&P 500 experienced more than 30% volatility 10 times and more than 10% volatility 39 times. .

Source: E-investing For Beginners

No guarantee for your initial investment

Because stocks are so volatile, there is no guarantee that you won’t lose your initial investment.

If you bought shares of Microsoft valued at $57.625 on December 31, 2019 and sold them a year later at $21.688, you would have lost 62.3% of your initial investment.

So while stocks can earn you huge returns on your initial investment (and compound interests on reinvestment), they can also present high risks for your money.

Lose with the market

Just as you can grow with the market, you can also lose with the market.

On October 9, 2007, the Dow Jones Industrial Average (DJIA), an index that tracks the performance of thirty large companies in the US, closed at $14,164.53.

By March 5, 2009, it had dropped to $6,594.44, more than a 50% loss in value. If you were invested in the DJIA at that time, you would have lost 50% of your investment.

When you invest in stocks, you lose with the market.

This is why investing only in stocks or the S&P 500 is not a good investment strategy.

Here, our friend the humble bond enters the stage.

[This is why Sarwa discourages investing in just a single market index. To learn more about this, read, “Why Not Only Invest in the S&P 500?”]

2. What is a bond?

A bond is an asset of indebtedness that companies and governments use to raise funds from the public.

When a company or a government wants to raise money from the public, they issue bonds that the public can purchase. In return for the money the government or company will collect, the buying public will have a bond certificate that shows they are creditors to the company or government.

There are three types of bonds:

- Corporate bonds: They are issued by companies.

- Treasury bonds: They are issued by a government

- Municipal bonds: They are issued by government agencies, municipalities, counties, and states.

For every bond issue, the issuer is the debtor (government, company) and the buyer is the issuer’s creditor.

Components of a bond issue

There are three major components of a bond:

- Face value: If a company wants to raise $10 billion through bonds, they can divide this into 10 million bonds valued at $1,000 each. The 10 million units is similar to the outstanding shares of a stock and the $1,000 is similar to the price of a stock. Like stocks, you can buy many units of a bond (for example, you can buy 1,000 units for $1,000,000). The price of the bond ($1,000) is known as the face value of the bond. This is the amount the company will pay back when the bond matures.

- Maturity date: This is when the debt is expected to be due. There are 3-year, 5-year, 10-year, 30-year, and 50-year bonds. For a 10-year bond, for example, the bond matures after 10 years from the issue date. On that day, the debtor is expected to pay back the face value of the bond.

- Coupon rate: The coupon rate is the interest rate the debtor will pay the creditors for agreeing to part with their money for a given period of time. The coupon rate is in percentage (e.g. 5%) and they are paid twice in a year. So if you hold a bond with a face value of $1,000 and coupon rate of 5%, you will earn $50 every year, paid as two $25 payments.

You should immediately recognise three differences between bonds and stocks:

- Bonds are held for a defined period while you can hold a stock forever. When a bond matures, you can’t hold on to it again.

- Bonds earn a fixed rate of return, unlike stocks where you don’t know how much you will earn.

- You will recoup your initial investment. With bonds, there is a provision for the debtor to pay you back the face value of your bond holdings at maturity. There is no such guarantee with stocks. If a bond issuer defaults, they can be forced into bankruptcy so they can repay the bond holders from the sale of their assets.

You can purchase bonds when they are originally issued in the primary market or buy them from someone else in a secondary market.

Making money with bonds

Now to the juicy part: how can you make money with bonds?

Like stocks, there are two ways to make money from bonds.

Interests payments

The bond issuer (debtor) will pay you a fixed interest every year (paid twice in a year).

In the above example, that’s $50 every year. If it’s a 30-year bond, you will earn $50 for thirty years and get your $1,000 back at maturity.

Unlike stocks where companies can decide to pay dividends or not, every bond issuer has to pay the fixed interest (except in the case of zero-coupon bonds).

Bond appreciation

You can also sell your bonds at a premium in the secondary market.

If you sold the $1,000 bond in the above example at $1,200, you have sold at a premium and earned $200 (in addition to the interest you have received already).

The price of a bond at any time will depend on the maturity date (how soon or how far it is), the current interest rate (how valuable is this bond compared to the ones being issued at this time), and the bond ratings (which shows how likely it is for the debtor to pay or not).

For example, a 5-year bond is less risky than a 15-year bond lower risk of default), thus, the former will have smaller returns compared to the latter. Therefore, when you are selling a bond that is maturing soon (in five years, for example), it will be cheaper, ceteris paribus, than a bond that is maturing much later (in 15 years, for example).

Similarly, when the current interest rate is higher than the interest rate when you bought the bond, the price of your bond will be lower since people can buy fresh ones that will pay higher coupons. If the current interest rate is lower than it was when you bought the bond, the price will be higher since the available bonds will pay a lower coupon compared to the one you are selling.

The ratings of the bond will also determine its attractiveness to others. A highly-rated bond, ceteris paribus, will command a higher price than a lowly-related bond.

What are the benefits of bonds to an investor?

Why have bonds become so popular in the investment world? Here are some of the most important advantages of bonds:

Low volatility and low risk

The bond market has only experienced double-figure yearly volatility twice – in 1982 and 2008.

In contrast, as we have seen above, the stock market has experienced it 39 times.

Because of low volatility, bonds are less risky and they help protect investors’ money.

[For more on the volatility of bonds compared to stocks, read, “Should What’s Happening To The Bond Market Affect Your Portfolio”]

Guarantee for your initial investment

Even if the bond issuer is not solvent (which would only happen with corporate bonds), your initial investment in a bond is guaranteed at maturity.

So if you purchased 1,000 units at $1,000 face value, you will get your $1,000,000 at maturity.

This return of the initial investment almost always happens, even with corporate bonds. In fact, companies prioritise paying back their bond holders over paying dividends to their stockholders.

In the case of treasury bonds issued by governments, the chances of default are almost zero.

For corporate bonds, investors use bond rating agencies like S&P and Moody to identify credit-worthy bond issuers with very low risk of default. With that, investors can have almost an absolute guarantee that your initial investment will be recouped at maturity.

Protection in a bear market

Unlike stocks that flow with the market, bonds offer protection when there is a bear market.

When the national economy is down and there is panic, people move their money to the bond market (because of its low volatility and low risk) to protect themselves from a volatile stock market. Therefore, when negative macroeconomic trends are resulting in exit from the stock market, there is increased entrance into the bond market.

“Markets need not be in sync with one another,” said Seth Klarman, billionaire investor and author of Margin of Safety.

“Simultaneously, the bond market can be priced for sustained tough times, the equity market for a strong recovery.”

The downside of bonds

Despite all these advantages, bonds also have their downsides.

Low returns

Bonds don’t offer the high returns that stocks provide.

Currently, the yield on the US 10-Year Treasury Bond (a standard measurement of the performance of the bond market) is 1.575%.

The chart below shows that the annual average returns of stocks exceed that of bonds.

Source: New York University STERN

Though the gap in returns narrows with the 10-year annualised returns, it is evident that stocks outperform bonds.

Source: New York University STERN

Possibility of default

While the possibility of default can be minimised, it is not zero. Companies with good ratings can still mess up and default on interest payments or repayment of the face value of the bond at maturity.

Exit in a bull market

Once the bear market turns into a bull market, many people tend to exit the bond market and go back to the stock market to earn higher returns.

This fall in demand can lead to falling prices in the bond market in the interim.

This is obviously an important downside to consider. But only for short-term investors. Over the long-term the bond market has historically been a strong bastion for diversified investors.

As Seth said above, stocks are priced for a strong recovery.

[To understand why this fall in demand should not affect long-term investors, read, “Should What’s Happening To The Bond Market Affect Your Portfolio?”]

3. How do stocks and bonds complement each other in a diversified portfolio?

So which one should you buy? Stocks or bonds?

Now this is where answering the question ‘What are stocks and bonds’ goes beyond explaining the terms to understanding how they affect your portfolio.

Should you take higher returns with higher risk or lower returns with lower risk?

Should you protect your investments and earn lower returns or expose them in a volatile stock market in expectation of higher returns?

Should you flow with the market or hedge yourself against market volatility?

The good news is that with the development of the Modern Portfolio Theory, stocks and bonds are not mutually exclusive.

Instead, they complement each other.

How is this so?

Harry Markowitz developed the Modern Portfolio Theory in 1952 as a way to help investors measure and minimise risk. He discovered that every investor is risk-averse and strives to earn higher returns at the same level of risk and lower risk for the same level of returns.

Harry believed that the best way to achieve this is by having a portfolio of assets with less correlation to one another.

“Correlation is a concept from statistics that measure the tendency of two random outcomes, like returns, to move together (positive correlation), in unrelated ways (zero correlation), or in opposite directions (negative correlation),” said Jiro Kondo, Assistant Professor of Finance at McGill University and Head of Portfolio Construction at Sarwa.

“The higher the correlation between assets, the lower the diversification benefit the investor gets from holding multiple assets.

So, when selecting portfolios, the best way to diversify is to pick assets with low correlation to each other — the opposite of what novice investors do.”

Two assets are said to be correlated when the same factors that affect A affect B in the same way. The same assets are not correlated if the same factors that affect A do not affect B. They are negatively correlated if the same factors that drive A to one direction drive B to an opposite direction.

Therefore, the more unrelated or negatively related two assets are, the better.

This means that if asset A is falling, B is not falling (in the case of zero correlation), or, in the case of negative correlation, if A is falling, B is rising.

So, when an investor holds assets A and B that are unrelated or negatively correlated, his risk is less and his returns higher than if he held only one of them.

For Harry, the way investors can minimise risk and maximise returns is to have a portfolio of diversified assets that are unrelated or negatively correlated.

So how does this affect stocks and bonds?

[To learn more about Harry Markowitz and the Modern Portfolio Theory, read, “The Brilliance of Modern Portfolio Theory: A Nobel-Prize Winning Formula To Cut Investment Risk”]

The correlation between stocks and bonds

As discussed above, many investors enter into the bond market in mass when the economy is doing poorly and the stock market is bearish. This increases demand and the bond market rises.

Consequently, bonds serve as a buffer when stocks are underperforming.

Also, when the market recovers, many people take money away from the bond market and enter the stock market again.

The negative direction of the relationship between stocks and bonds (which holds most of the time) means, according to the Modern Portfolio Theory, that a portfolio that holds stocks and bonds together produces more returns and less risk than the one that holds only one of them.

As Jiro Kondo puts it, “Some exposure to the bond market, which is often ignored by novice investors, is important because it historically has both low risk and low correlation with equity markets”

“Every portfolio benefits from bonds; they provide a cushion when the stock market hits a rough patch,” adds Suze Orman, personal finance expert and author of The Nine Steps To Financial Freedom.

She goes on: “But avoiding stocks completely could mean your investment won’t grow any faster than the rate of inflation.”

Therefore, a combination of the two in a portfolio is a good way to achieve the best return-risk ratio.

This is also evident from the fact that stocks provide higher returns while bonds provide lower risks.

Therefore, a combination of stocks with bonds will provide higher returns than could have been earned with bonds alone. Similarly, a combination of bonds with stocks will provide lower risk than could have been achieved with stocks alone.

4. How do you achieve broad diversification with stocks and bonds?

The traditional wisdom in investing is to have a ratio of stocks to bonds that reflect your risk tolerance (e.g. 60% stocks and 40% bonds for people who are growth investors and the reverse for those who are conservative).

However, investors are discovering that this simplistic approach does not maximise returns or minimise risks.

What is needed is what Harry Markowitz called broad diversification. In addition to diversification by asset class (stocks and bonds), investors need to diversify by market, industry, and by market cap. Moreso, investors need to consider other asset classes like REITs (real estate investment trusts).

[To understand why REITs are far better than buying individual real estate properties, read, “Is Investing in Real Estate Safe?”]

Why is diversification by market necessary?

When all of your stocks and bonds are in the same market (e.g, US market), then all your investments are exposed to the macroeconomic trends in the US. If the US market enters a recession, all your investments lose value.

Instead, by investing in markets that are uncorrelated or negatively correlated to the US market — e.g, developed markets outside the US (North America, Western Europe, Australasia, East Asia) and emerging markets (Brazil, Russia, India, China) — risk is further minimised and returns further maximised.

Why is diversification by industry necessary?

Stocks and bonds in the same industry will move in the same direction. To achieve broad diversification, you need stocks and bonds from different industries that are uncorrelated or negatively correlated. In that case, when an industry becomes bearish, other industries can stay the course. So instead of having all your stocks and bonds in the technology industry, consider other industries like consumer supplies or basic materials, for example.

Why is diversification by market-cap important?

Large-cap companies tend to be less risky with stable returns while small-cap companies tend to provide higher returns but with higher risk. Mid-cap companies are in between. By buying stocks across the three market-cap, you can minimise your risk (enjoy the lower risk of large-cap companies) and maximise your returns (enjoy the higher returns of small-cap and mid-cap companies) with the lesser correlation between those companies.

So instead of a simple stock-bond ratio diversification, investors can achieve broad diversification by adding assets like REITs and further diversifying by market, industry, and market-cap.

[To understand why diversification is so important to your portfolio, read, “The Importance of Portfolio Diversification”]

- How can you build a diversified portfolio of stocks and bonds

To help you achieve a broad diversification, Sarwa provides a diversified portfolio that includes REITs as well as market, industry, and market-cap diversification.

Sarwa does this by purchasing stock ETFs, bond ETFs, and REITs ETFs in the US market, developed market, and developing market.

Why ETFs instead of individual stocks, bonds, or REITs?

An ETF is a basket of securities that tracks the performance of an underlying index and are traded on the stock exchange market.

Because a single ETF contains many securities in itself, it offers diversification that individual assets can’t offer. When you buy one stock, you are exposed to just one company with a single market-cap in one industry and market. But with a single ETF, you are exposed to hundreds of companies diversified across various industries and market-cap.

[For more on ETFs and why they are becoming so popular, read, “Why Invest in ETFs? Explaining the Popularity of The Go-To Fund”]

So when you buy a stock ETF (e.g. the Vanguard Total Stock Market Index ETF, VTI, that has 3755 stocks) you immediately enjoy diversification by industry and market-cap.

When you buy a bond ETF (e.g. the Vanguard Total Bond Market ETF, BND, that has 18,391 bonds), you enjoy diversification by industry. The same goes with REITs (Vanguard Real Estate ETF, VNQ, has 152 different REITs).

When you combine the three, you also have diversification by asset class. Now, add stock ETFs from developed (e.g. iShares MSCI EAFE ETF, IEFA, with 2799 companies) and emerging (e.g. iShares MSCI Emerging Markets ETF, IEMG, with 2554 companies) markets and bond ETF from the global market (e.g. Vanguard Total Bond International Market Index ETF, BNDX, with 6042 bonds) and you have diversification by markets (in addition to the diversification by industry and market cap already in these three ETFs).

Jiro Kondo, the Head of Portfolio Construction, best summarises this approach: “At Sarwa, we seek to achieve best-in-class diversification by optimising a portfolio of ETFs that covers many important segments of the investment universe – not just US stocks in a particular industry. This includes exposure to the broad US equity market, equity markets from other countries in both the developed and developing world, the real estate market, and both US and international bond markets (both government bonds and corporate bonds)”

Consequently, when you invest your money with Sarwa, you enjoy broad diversification that perfectly matches your unique profile while minimising your risk and maximising your return.

You don’t just have a simple 60% stocks and 40% bonds portfolio but a well-diversified portfolio that helps you achieve your investment goals.

Now that you truly understand what stocks and bonds are and how they impact your portfolio, it is time to start investing your money in a broadly diversified portfolio that minimises your risk and maximises your returns.

Want to learn more about how you can start your investment journey? Schedule a free call with a Sarwa Wealth Advisor, and we’ll answer all your questions.

Takeaways

- A stock is a security that represents a portion of ownership in a company.

- Stocks generate high returns and help investors earn compound interest and grow their money with the economy. But they are volatile and risky.

- A bond is an instrument of indebtedness that governments and companies use to raise money from the public.

- Bonds are less risky and they provide protection in a bear market. But they provide lower returns.

- When stocks and bonds are combined in a broadly diversified portfolio, they help investors minimise risk and maximise returns