Over the past three months, the fixed-income market has experienced considerable volatility, and conservative risk-averse investors — who are typically heavily invested in bonds — have become increasingly frazzled. They are now wondering: “Is my conservative portfolio riskier than I thought?”

These worries come from understandable origins.

After all, isn’t it natural that we prefer to make money, not lose it?!

However, what is also quite natural is that our emotions tend to get overly excited during times of market turbulence, ultimately hijacking our logic to throw long-term strategy out the window.

But the last thing a successful investor does is panic.

That’s where we come in: to help investors in the stock market overcome their own emotions. Gaining control of our emotions will help steer our investment outlook toward long-term goals that will so greatly counteract the market’s neurotic short-term temperament.

Let’s be clear: the market is a rollercoaster ride that can only be fully understood on long-term time horizons.

This approach requires time for new investors to harness. We can tell you from experience that this type of calm long-term attitude toward investing is not easily won, but it is much valued.

We know this precisely because the ability to control our emotions is what differentiates successful investors from unsuccessful ones over the long term.

Charles Swindoll, a life coach, pastor, and founder of Insights for Living, once said that life is 10% what happens to us, and 90% how we react. Success or failure is thus in our reaction.

Benjamin Graham, the godfather of value investing, agrees: “Individuals who cannot master their emotions are ill-suited to profit from the investment process.”

Those are pretty bold words from the man that taught Warren Buffett the fundamentals of investing!

So, what has been happening in the bond market these days, and what should you do and not do about it?

In this article, we will consider the following:

- What happened to the bond market in 2021 Q1?

- Why is there a downtrend in the bond market?

- Volatility in the bond market versus volatility in the stock market

- Inflation, high-interest rates, and stocks

- Long-term performance of bonds

- What should you do about the current decline

1. What happened to the bond market in 2021 Q1?

Historically, movements in the US 10-year Treasury Bond are the standard measurement of the bond market’s performance and sentiment.

Since the beginning of 2021, the US 10-year Treasury Bond has been experiencing unusual volitaitly.

The yield on a US 10-year Treasury Bond opened at 0.93% on January 4, 2021. As of April 12, 2021, it was up to 1.69%. That’s an 81% increase in yield so far this year. .

Why is this a bad thing? If yield is increasing, shouldn’t we all be glad (maybe throw a party?).

Well, not so fast. In the bond market, there is an inverse relationship between the yield and the bond price. As the yield of a bond goes south, the price goes north. Therefore, the continuous rise of the yield on the US 10-year Treasury Bond means bond prices are falling.

As of March 2, 2021, the US 10-year Treasury Bond was down 4%. As of April 12, 2021, it was down 6.4%. The Financial Times describes the current decline as the worst start to a year in the bond market since 2015. And that’s saying something.

However, it is worth emphasising that you don’t actually lose your money in a downward trend unless and until you decide to sell your bonds.

2. Why is there a downtrend in the bond market?

There are two major reasons for this downtrend.

First, investors have a positive outlook on the global economy because of the development and distribution of the COVID-19 vaccine and the massive amounts of money that the US and UK are spending to hasten the full opening of their economies.

It’s important, in this respect, to understand the relationship between the bond and the stock market. When an economy is down (like it was for most of 2020), people turn to low-risk assets like treasury bonds to protect their funds.

As the market begins to open up and recover, institutional investors gain more confidence and money is moved into equities at larger volumes, reducing the demand for bonds (which causes a fall in price).

Therefore, the expanded distribution of vaccines, the recent $1.9 trillion stimulus package in the US, and the UK government’s continuous spending to stimulate a recovery has increased investor confidence.

Secondly, commodity prices have also been increasing in 2021. When commodities (crude oil, gold, coffee, etc.) price increase, raw materials become more expensive, then finished goods follow, and inflationary pressure settles in.

Inflation is the boogeyman of the market because it reduces the real value of the coupon (the interest on your bonds) you will earn in the future. Fixed-income securities pay a predetermined interest (coupon) that does not increase with inflation. Consequently, when inflation rises, the real value of that interest decreases.

As investors expect a reduction in the real value of bond coupons, there is a drop in demand for bonds, and prices fall.

The expected recovery of the market and the expected increase in inflation rates are responsible for the decline in the bond market. These are the two culprits eating into the value of your bonds.

So, what then should you do? All the above are what happened — the 10% of the problem — but how you react determines how you solve the other 90%.

However, before telling you what you should do, we feel the need to tell you exactly why.

3. Now let’s put the decline of the bond market into clear context.

Most investors selling their bonds because of the current decline are going into the stock/equities market.

However, it is important to look beyond the present (leaving the panic-driven emotions aside) and consider the volatility of both markets.

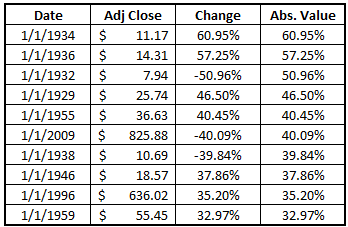

The bond market (again, the US 10-year Treasury Bond is the standard measurement) has only experienced double-figure yearly volatility in prices twice – in 1982 (32%) and 2009 (11%). This means that the change between the opening and closing prices for the year has only exceeded 10% twice.

Let’s contrast that with the stock market.

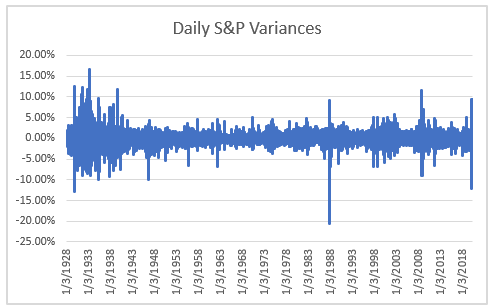

Below is a chart showing the daily volatility in the stock market (the S&P 500 is the standard measurement) for some selected days:

On ten of these days (52.6%), the stock market experienced double-figure volatility in prices.

You can see those 10 days below:

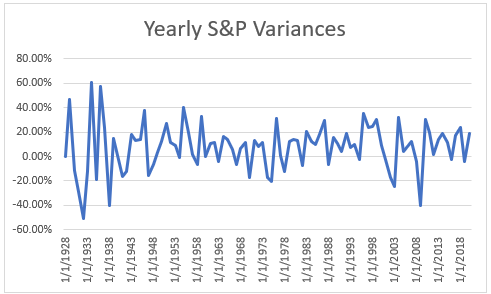

Now, let’s see the yearly variances.

Overall, the stock market has experienced more than 30% yearly volatility in 10 years. It was more than 10% over 39 years.

As a long-term investor, you must look beyond the current situation and consider the market’s long-term volatility.

From a historical perspective, the bond market is still the least volatile market and the best way to protect your money and reduce your portfolio’s risk.

Moreover, if you can’t bear the volatility of the bond market, what will you do with the more volatile (to put it mildly) stock market when volatility comes knocking?

If you can’t outrun footmen, how will you cope against horses?

4. Inflation, high-interest rates, and stocks

Remember that one of the factors causing the decline in the bond market is the expected rise in inflation due to a rise in the prices of commodities.

However, inflation does not only affect bond markets. When the inflation rate is high, the central banks respond by increasing interest rates to reduce the money supply in the economy.

High interest rates, thus, increase the cost of borrowing and reduce consumer demand. The increased cost of borrowing and reduced consumer demand can reduce companies’ earnings, which will lead to a decline in the stock market.

It is therefore not surprising that some stocks are already sliding down just as the bond market is declining.

“The world’s rampant stock markets responded by going into reverse in February,” writes Arman Hassanniakalager, a lecturer at the University of Bath, “as they factored in higher interest rates, as well as higher production costs because of surging commodity prices.”

Much to the pain of high-growth investors, the NASDAQ Composite Index declined by 10% from February 12 to March 8.

Lessons were learned: While value stocks perform well in an inflationary environment, growth stocks and dividend stocks don’t. Also, stocks tend to become more volatile in an inflationary environment.

Put simply, the stock market is not necessarily a haven or a hiding place from a declining bond market.

5. Long-term performance of bonds

When considering the performance of your bonds, take a real hard look at the bigger picture. Bonds produce returns over the long term, and this is historically proven.

In 2020, the New York Times ran a story that showed that from 2000-2020, bonds outperformed stocks in annual returns. In that period, the S&P 500 returned 5.4%, while long-term treasury bonds gained 8.3%, and long investment-grade corporate bonds 7.7%.

Surprised? Don’t be.

Of course, this data doesn’t tell the whole story. Bonds outperformed stocks during that period because the early part of 2000 was one of the worst entry points into the stock market over the past decades. If we change that date to 2002, stocks outperform bonds.

However, the point of this example is that in the long-term, bonds produce annualized returns that are not too far away from stocks.

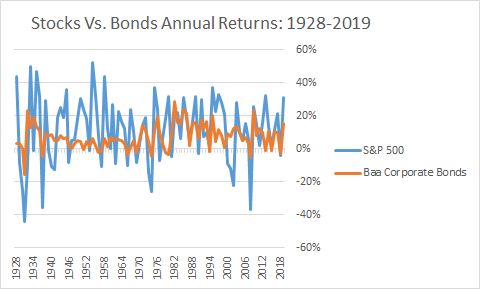

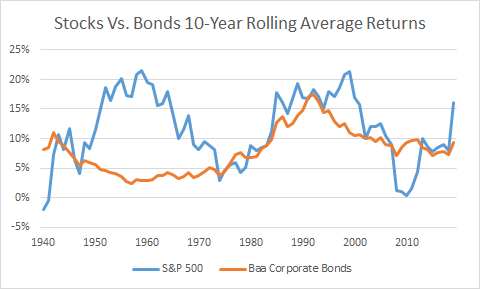

The chart below compares the returns of stocks and bonds from 1928-2019.

Here,stocks outperformed bonds more than bonds outperformed stocks. But when you consider the 10-year annualised return, the gap between stocks and bonds narrows.

Also, rising interest rates can have a positive effect on bonds in the long term. While it causes the bond price to fall, it increases the returns you will get from reinvesting your coupon/interest.

While the market will still adjust (interest rates will come down when inflationary pressure becomes deflationary), long-term investors will still enjoy the benefits of a higher rate of return on the reinvestment of their coupon payments.

Therefore, whether the interest rate is high or low, the long-term bond investor always always has a strategy to find gains — by taking advantage of an increased rate of return in the former, and a higher price in the latter.

6. What should you do about the current decline?

We are here at last.

Let’s take this step by step.

1. Stick with long term investing

The first thing to do is to remember why you are a long-term investor, to begin with. You are a long-term investor because you know that “the stock market is a device to transfer money from the impatient to the patient,” as Warren Buffet so fondly has said.

You know that fear and greed (that lead some “investors” to time the market) are the greatest enemies of investors.

You have probably heard that “investing is like watching paint dry or watching grass grow,” as Paul Samuelson, the Economic Sciences Nobel Prize winner, puts it.

Don’t let your emotions get the best of you because of the current decline in the bond market. Historical data shows that bonds are the least volatile assets in the long term, they perform closely to stocks in the long term, and you profit from high-interest and low-interest-rate environments in the long term, as well.

So keep the long-term perspective and don’t let short-term declines derail you.

2. Remember risk and return

Secondly, remember that investment is both about risk and return. Stocks may have higher returns but remember that they are very volatile.

Bonds are there in your portfolio to reduce your portfolio’s risk – diversification – so you don’t lose your money. When you take them out, you are exposing yourself to the high volatility of stocks.

So while you consider returns, don’t forget risk. Remember why bonds are there in the first place. And as a conservative investor, remember why you have more bonds than others — maybe you don’t have the right time horizon to expose yourself to stocks.

3. Diversify

The third thing to consider is whether your portfolio has broad diversification. If you invest with Sarwa, you can be sure that your portfolio is well diversified to maximise return and minimise risk.

Sarwa uses the Modern Portfolio Theory, developed by Nobel Prize laureate Harry Markowitz to construct efficient portfolios.

Healthy portfolios are well-diversified across asset classes (stocks, bonds, REITs) and markets (emerging, developed, global, United States) and in low-cost ETFs.

Sarwa considers this healthy because whatever might happen in whatever market, you have the broad diversification that protects your money and grows it steadily over the long term.

4. Keep reinvesting

One of the benefits of making money work for you instead of the other way round is that money has the power to generate compound returns. That is, the money you invest earns interest and the interest also earns interest, ad infinitum.

Only by reinvesting your interest regularly can you multiply the ability of your money to earn more money — this is called compound returns.

Don’t allow the current decline in the bond market prevent you from earning compound returns on your money.

Moreover, an increase in interest rate, as already explained, is a good opportunity to earn more returns from the reinvestment of your interest (coupon) — the new bonds you buy with those coupons have higher returns in a higher interest market. As market interest rate increases, your coupons earn more returns and grow faster.

Reinvesting in bond ETFs, such as BND or BNDX, is a strong strategy that benefits an investor’s portfolio, especially over a long time horizon.

Therefore, rather than discouraging reinvestment, lower bond prices (with the higher interest rate that goes with it), is a good incentive for continuously reinvesting your coupons rather than leaving the market.

5. Stay invested

Similarly, don’t leave the bond market altogether because of the present decline. The longer you stay in the market, the better.

Why is this so?

The longer your money remains in the market, the more it can work for you and generate compound returns. When you leave, the opportunity cost of the returns you could have made and the returns those returns would have made.

According to a study by Market Watch, an investor that stayed in the stock market from 1996 to 2015 (via the S&P 500) would have earned an average of 8.2% returns per year. [We have another study on this subject with our in-house financial expert Dr. Jiro Kondo here.]

However, if an investor missed out on the top 20 days during that period, he would have earned only an average return of 2.1% per year.

The person who remained in the market is almost 4 times better off than the person who leaves and rejoins later because they are more likely to miss the top trading days. It’s the same in every market: the longer you stay in the market, the better.

It’s the long-term investor that wins.

Takeaways

- Though there has been a decline in the bond market, it remains the least volatile market.

- The stock market is not necessarily a haven in an inflationary environment.

- In the long term, bonds earn annualizsd returns that are closer to stocks.

- Risk is as important as returns in investing. Research shows that bonds are the least risky profitable asset class.

- Instead of panicking, keep focusing on the long-term.

- Ensure you have broad diversification, then keep reinvesting and stay invested.