Congratulations, you have just received a financial windfall that can set you up for life. It may have come from a lottery win, an inheritance, selling your equity stake in a startup, a professional athlete contract, or something else.

What are you doing next? Different ideas are probably popping into your mind already. And that’s where the problem arises. With financial windfall comes the sudden wealth syndrome, which can be manifested in:

- The tendency to splurge on luxuries and large purchases you have been eyeing for a long time

- Confusion about what to invest in and what portion of the money to invest

- The fear and anxiety of misusing the money

- Distress arising from pressure from friends and family members who need financial help

Knowing how to manage sudden wealth is not easy. It is no wonder that about 70% of lottery winners in the US end up being broke, according to Search Logistics, a digital management company. However, if used well, windfalls can relieve financial stress and provide a means of social mobility, according to The Roosevelt Institute, a think tank.

In what follows, we consider seven smart steps you can take immediately to manage sudden wealth and position yourself for a prosperous financial future.

Do you want to know more about creating financial plans and building wealth in the stock market? Subscribe to Sarwa’s Fully Invested newsletter for weekly financial management and investment tips.

1. Stay calm

In today’s hyperactive digital age, this might be the hardest of all these seven steps.

It may be difficult looking at your newfound wealth in a bank account and doing nothing, especially when you are being bombarded with phone calls and text messages from people seeking help. Or you may happen to be driving by your dream car or house.

However, moments of excitement are not the best for making life-transforming decisions like how to manage sudden wealth. Allowing the excitement to wear away can give you much-needed clarity and help you make smart decisions.

In other words, a smart decision three months after you have gotten a good fortune that improves your well-being is better than a series of poor decisions made hours or days after that wrecks your finances.

One more point: you might be better off taking the following steps with the help of a wealth manager, financial advisor, or financial planner.

These professionals can help you make the right financial decisions and also prevent you from making the wrong ones. Most importantly, they can help you develop a calm mind that is not controlled by mere emotions and also handle things like tax planning, estate planning, and retirement planning.

Digital financial advisors like Sarwa use the latest financial technology solutions to provide low-cost, automated, data-driven, and personalized financial advice. Moreover, they are easier to use because of streamlined processes that can be conveniently completed without stress, as well as the help of customer service that is available 24/7.

You can schedule a free call with a Sarwa wealth advisor who will help you through the following steps. The result will be a personalized financial plan well adapted for attaining your financial goals.

If the windfall is a large amount of money, you should consider exploring Sarwa Private Wealth for more comprehensive financial services (financial planning, tax optimization, access to private markets) and access to a team of professionals (including investment advisors, estate planners, tax consultants, and lawyers, etc.).

2. Review your current financial situation

The second step is to review your current financial situation. Some of the relevant questions for this exercise include:

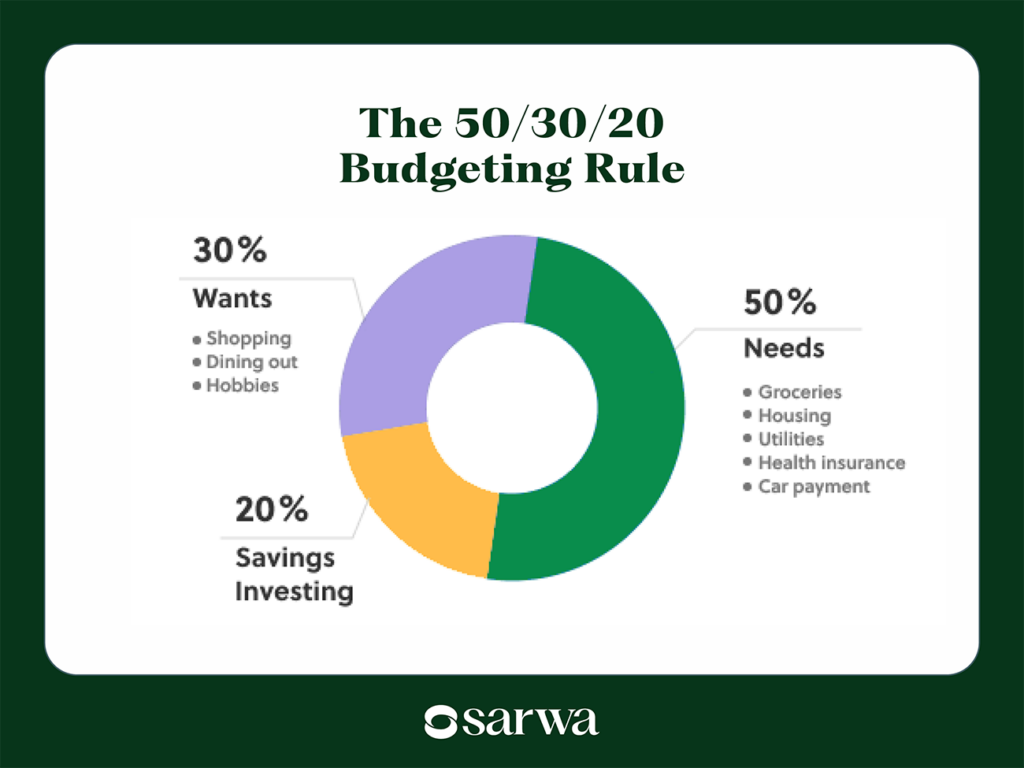

- Do you have a budget? If you have been living your life pre-windfall with a monthly budget like the 50/30/20 rule, you will be in a better position to learn how to manage sudden wealth.

But it is not too late to create a budget and put your personal finances in order.

Ignore the new wealth for now and focus on creating a budget for your regular monthly income. The 50/30/20 rule requires that you spend 50% of your income on your needs, 30% on your wants, and 20% to saving/investing.

A budget like this one helps to put your financial house in order, avoid overspending, and prepare you to make smarter decisions along the way.

- Do you have emergency funds? An emergency fund is a pool of funds that you can count on when financial emergencies arise. Learning how to start an emergency fund saves you from going into debt or selling off your assets at a discount to meet unexpected expenses.

Financial professionals advise that you should have up to six months of your living expenses (needs plus wants) in an emergency fund. If you don’t have such a fund, building it up should be a priority.

- Are you in debt, and what is the cost of servicing your debt? If you have debt, you need to divide it into good and bad debt. Good debt is low-interest debt that helps you build wealth or make some form of personal progress. Examples include a mortgage (your property is an asset), a student loan (improves future earning potential), and a business loan (your business is an asset).

Bad debt is high-interest consumer debt that does not increase your future earning power. Examples are credit card debt, payday loans, and vacation loans, among others.

Source: Waterstone Mortgage

It is also important to specify the interest rate you are paying on each debt. This will become useful later on.

3. Clarify your financial goals

Of course, almost everyone wants to attain financial security (or financial independence) and create wealth for future generations.

However, for our purposes, your financial goals need to be SMART (specific, measurable, achievable, relevant, and time-bound). The specificity of these goals will make it easier to create a plan to achieve them.

Financial goals often come in three forms – short-term, medium-term, and long-term. Short-term goals are those you want to achieve in less than a year, medium-term goals can take between two to five years, and long-term goals can be anything greater than five years.

Your task at this point is to ignore the windfall for now and highlight the financial goals that will contribute to your self-actualization.

Another task is to rank these goals in order of priority. You can do this for your short-term, medium-term, and long-term goals or all of your financial goals as a whole.

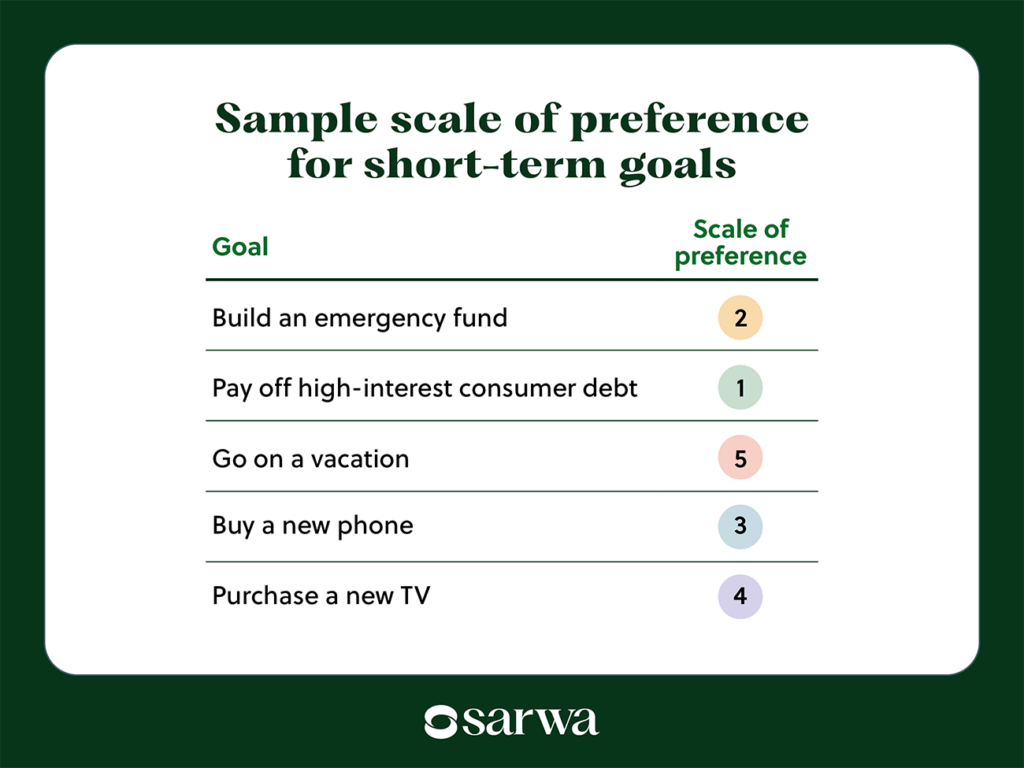

Suppose your short-term goals are to build an emergency fund, pay off high-interest consumer debt, go on a vacation, buy a new phone, and purchase a new TV. A sample scale of preference can be as below:

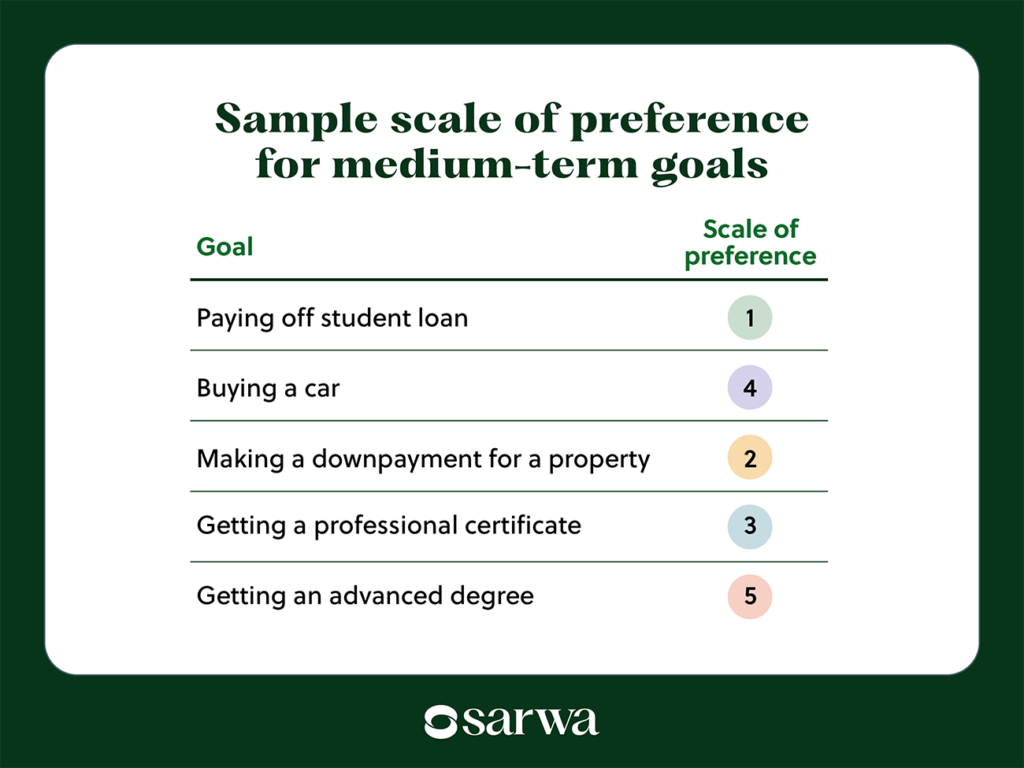

Also, suppose your medium-term goals are paying off your student loan, buying a car, making a down payment for a property, getting a professional certificate, and getting an advanced degree. A sample scale of preference can be as below:

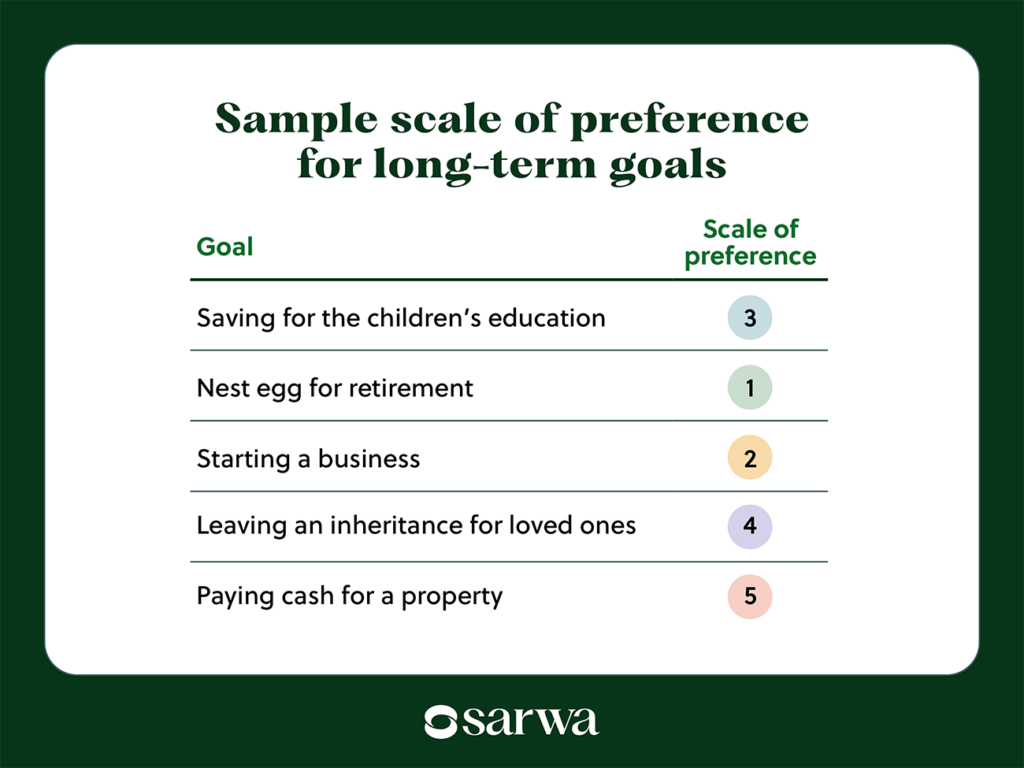

Finally, your long-term goals can include saving for your children’s education, building a nest egg for retirement, starting a business, leaving an inheritance for loved ones, and paying cash for a property. A sample scale of preference can be as follows:

Alternatively, you can put all of the 15 goals together and assign a rank to them based on the order of priority (1 being the most important). Below is an example:

The scale of preference is all about individual priorities, which means it will differ from one person to another. Take the time to think through each goal before completing the scale.

4. Create a plan based on your current financial situation and financial goals

All the steps we have taken so far have ignored the windfall. As we said above, it is better to take the time to create a solid plan that will help you secure your future than to rush and regret it later.

At this point, you understand your current financial situation and financial goals. If done right, you have done those two things without taking into cognizance the financial windfall currently lying in your bank account.

Now is the time to create a plan for that money based on the scale of preference you have created.

The first step towards doing this is to put a monetary figure on the goals you have included in your scale of preference. For example, paying off your high-interest consumer debt may cost AED 100,000, building an emergency fund may cost AED 300,000, and you may need a nest egg of AED 9,000,000 to retire.

After doing this, you may discover that your windfall is sufficient to meet all your goals. However, in most cases, they won’t be sufficient. This means that you will still need to keep to the 50/30/20 rule to meet all of your financial goals (and many more goals will be added over time).

The point here is that the financial windfall should be seen as support for your systematic investment plan rather than its replacement.

Let’s consider what a typical financial windfall plan looks like based on the scale of preference we created above. Assume that the windfall is AED 20,000,000.

Again, this is just an example. Your goals and scale of preference may differ. Also, your financial windfall may not remain after allocating it towards your financial goals.

5. Select the right investment opportunities

Your short-term and medium-term goals will require that you put money aside in savings products where you can easily access them to achieve those goals. The returns will be low (compared to investing in the stock market), but the goal here is not to build wealth but to preserve it.

A savings product like Sarwa Save can help you do this. You can pack money for your short-term and medium-term goals here and earn a 4.5% return.

Unlike other high-yield savings products, Sarwa Save does not lock up your money – you can withdraw part or all of it at any time.

There is also a halal version where you can earn a 4.1% return on your cash.

However, for your long-term financial goals, you will need to invest in the financial markets.

As the example above shows, lump-sum investing in the stock market can significantly reduce the amount you need to commit now to achieve a long-term financial goal involving a large sum of money later on.

To illustrate, leaving AED 40,000,000 for your children may seem incredible, but putting AED 729,000 in the stock market today can get you there in the next 45 years.

However, this is where you need to be especially careful. Many people who have received financial windfalls have failed to make much of it because they took investment advice from charlatans or misguided financial ‘analysts.’

Avoid get-rich-quick and money-doubling schemes from fake investment advisers. If it sounds too good to be true, it is probably a scam. Instead, stick to the financial assets that have created wealth for millions of people across time – stocks, bonds, real estate investment trusts (REITs), and gold.

6. Invest in a diversified portfolio of credible investment opportunities

Diversification ensures that you are not putting all your money in one basket.

Why not?

Putting your money in one basket means that once the basket is lost all your money is lost.

If you bought that one stock that you thought would be the next Amazon with all your windfall and it fails, all your money is gone. What if you bought a house in that location that will be the next industrial hub and a sudden flood leads to mass emigration instead? All your windfall is gone. What if you invested in that crypto that was supposed to be the next bitcoin but it doesn’t even last beyond ICO (initial coin offering)? All your money is also gone.

In contrast, diversification helps you spread your wealth in reputable assets that have made money for investors consistently over many decades.

By investing in a diversified portfolio of uncorrelated and negatively correlated assets, your overall risk is less than the risk of investing in any one single asset. In other words, when one of these assets is losing money, another asset is compensating for that loss (benefit of negative correlation), reducing the risk of losing your money.

Sarwa, for example, creates a diversified portfolio of stock ETFs, bond ETFs, and REIT ETFs (and bitcoin ETF, for those interested) that take into account your risk tolerance, financial goals, and time horizon. By combining these three elements, we create an efficient portfolio for every investor with the Modern Portfolio Theory.

By subscribing to Sarwa Invest, you can get your personalized portfolio(s) from Sarwa and start investing towards your long-term financial goals. You can also choose from a conventional portfolio, a halal portfolio, a socially responsible investment portfolio (assets that have positive impacts on the world), and a crypto portfolio (invests 5% of the portfolio in a bitcoin ETF).

Alternatively, if you prefer making your investment decisions and building an investment portfolio from scratch, you can purchase stocks, stock ETFs, REITs ETFs, gold ETFs, bitcoin, and other altcoins through Sarwa Trade.

7. Stick to your plan

When learning how to manage sudden wealth, we cannot take away the emotional part of it. This is why we started by advising you to stay calm and allow the excitement to wear off a bit.

For the same reason, we close by advising you to stick to your plan.

It is one thing to create elaborate plans of what you intend to do, it is another thing to execute those plans. Many people have paid financial advisors for customized plans and veered off to do the opposite of what they recommended.

This is especially important if you have chosen to build your net worth by investing in the financial market. Though we have looked at how money can grow in the stock market over the years, there is a short-term volatility that may make some people exit the market in pursuit of some schemes promising better returns.

The stock market is a slow and steady way to build wealth. “Do not take yearly results too seriously,” said Warren Buffett. “Instead, focus on four or five-year averages.”

As he said in another place, “If you aren’t willing to own a stock for 10 years, don’t even think about owning it for 10 minutes.”

The market will rise and fall in the short term, and you might become fearful.

Try not to let this get to you. Over the long-term, the market rises more than it falls (74%-26%). Don’t play the short-term game that causes many to lose their windfalls. Focus on the long term.

Also, the voices of your friends and neighbors pitching some investment products that will double your money in six months will grow louder, and you will be tempted to be greedy. They may even have some products to show you. Resist the urge. Keep playing the long-term game with a sharp-eyed focus on your financial goals.

In essence, avoid the fear-greed cycle.

Or as Warren Buffet puts it, “Be fearful when others are greedy. Be greedy when others are fearful.” When everybody is queuing to buy the next big thing (that is, when others are greedy), be fearful and stick with your plan. When others are fearful because the market is down, be greedy and focus on long-term growth.

As your money grows in a diversified portfolio, you will be well poised to achieve all of those goals one by one while your friends and neighbors are still trying to identify the next real estate hub, bitcoin, or Amazon.

“The best way to measure your investing success is not by whether you’re beating the market, said Benjamin Graham, Warren Buffet’s teacher and the father of value investing, “but by whether you’ve put in place a financial plan and a behavioral discipline that are likely to get you where you want to go.”

Are you ready to use your financial windfall to create a prosperous future? Sign up for Sarwa to access Sarwa Save, Sarwa Trade, and Sarwa Invest, or schedule a free call with a Sarwa wealth advisor to create a comprehensive financial plan.

Takeaways

- Sudden wealth can be overwhelming, leading to impulsive spending or poor financial choices. Taking time to let emotions settle before making major decisions can help ensure smart, long-term financial planning.

- Before deciding how to allocate your windfall, review your current financial situation and set clear financial goals ranked on a scale of preference.

- Avoid get-rich-quick schemes and invest in a well-diversified portfolio of credible assets like stocks, bonds, and REITs. A structured investment strategy helps grow wealth sustainably over time while managing risk.

- Emotional decision-making and market volatility can lead to poor investment choices. Staying disciplined, following a well-thought-out plan, and resisting the pressure of short-term gains ensures long-term financial stability.