Rome was not built in a day. Nor did the journey of a thousand miles begin with a step. Slow and steady wins the race, and so do investors that start SIPs (systematic investment plans) with specific goals, such as by investing $1,000 per month for five years.

Wealth is not built in a day, but rather is the result of small steps consistently taken over a long period.

However, we have tended to emphasise the slowness of wealth building rather than the steadiness. When it comes to wealth building and personal finance, steadiness is key. It’s important to move (even if slowly) but it is even more important to keep moving.

If you invest $1,000 (slowly) per month for five years (steadily), you are on a better track to wealth than if you only invest $1,000 twice in year 1, once in year 2, and twice in year 3, etc.

The steadiness and consistency of the former approach helps you earn compound interest on a larger scale. In fact, at the end of the five years, if you invest $1,000 per month you would have $83,156.62 in your investment account, according to the SIP calculator (assuming a yearly rate of return of 11.97% and quarterly compounding).

This is why at Sarwa we encourage investors to use a systematic investment plan that helps you set aside a consistent portion of your income (say 20% if you use the 50/30/20 rule) every month for the long term.

In this article, we will consider how you can maximise the use of an SIP by practically looking at how to consistently invest $1,000 a month for five years. We’ll cover:

- Creating a diversified portfolio

- Automating monthly transfers from a local bank account to an investment account

- Rebalancing the portfolio

- Reinvesting dividends

- Monitoring performance

[Do you want to set up a diversified portfolio that will help you achieve your investment objectives? Sign up for Sarwa and get started on your investment journey.]

1. Creating a diversified portfolio

Investing is not an end in itself. If you are setting up a 5-year SIP, it is because you have a goal you want to achieve at the end of year 5. Identifying and clarifying this goal(s) is important since it will determine the best approach to go about your investments.

Once the goal has been clarified, the next step is to create a diversified portfolio that will help you achieve that goal.

For reasons that we have explicated in other articles, we believe the average investor is better off as a passive investor. People like Warren Buffett, the legendary investor, and Mark Cuban, a billionaire and seasoned investor, agree with us.

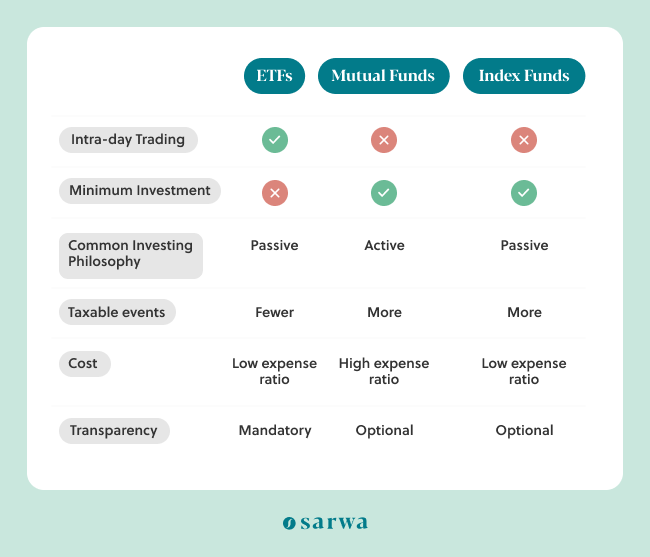

As an investment option, passive investing is cheaper, less risky, more transparent, and makes it easier to achieve diversification. This is why it is preferred over buying individual stocks (even bluechip stocks) or mutual fund investments (whether bonds or equity mutual funds).

Also, ETFs, as a channel for passive investing, are better than index funds because they are more liquid, support intra-day trading, and are more transparent.

So, the first step towards setting up a SIP is to create a diversified portfolio of ETFs that will help you achieve your investment goals and preferably lean into a passive investing approach.

At Sarwa, we use the Modern Portfolio Theory (MPT) to develop such portfolios. Every portfolio is personalised to fit in with the goals, risk appetite or tolerance, and time horizon of every investor.

You can get a customised portfolio from Sarwa or strategically build your own.

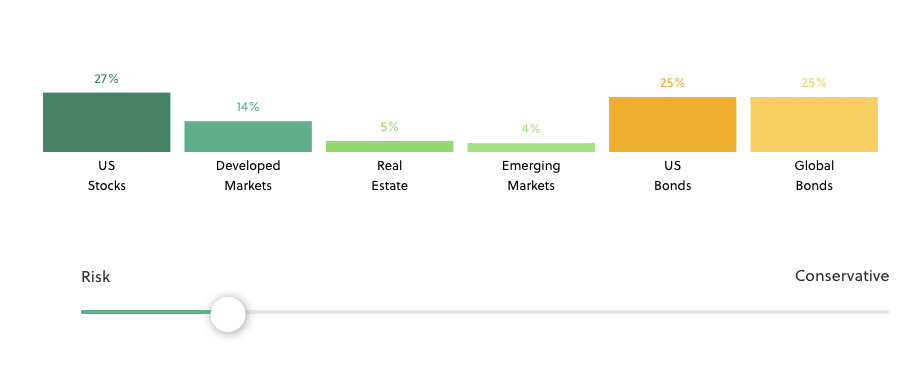

Below is a sample of a Conventional portfolio that Sarwa creates for clients. This portfolio is diversified across three asset classes: stocks, bonds, and real estate (by using REITs, or Real Estate Investment Trusts).

Stocks, which constitute 44% of the entire portfolio, are also diversified to include US stocks (which includes large cap, mid cap, and small cap stocks in the US), developed markets (stocks from countries outside of the US), and stocks from emerging markets (economies on the path to becoming developed markets).

Half of the portfolio is made up of bonds, diversified to include US and global bonds.

And 5% of the portfolio is in REITs.

This is a portfolio for a more risk-averse investor and/or someone with a shorter time horizon.

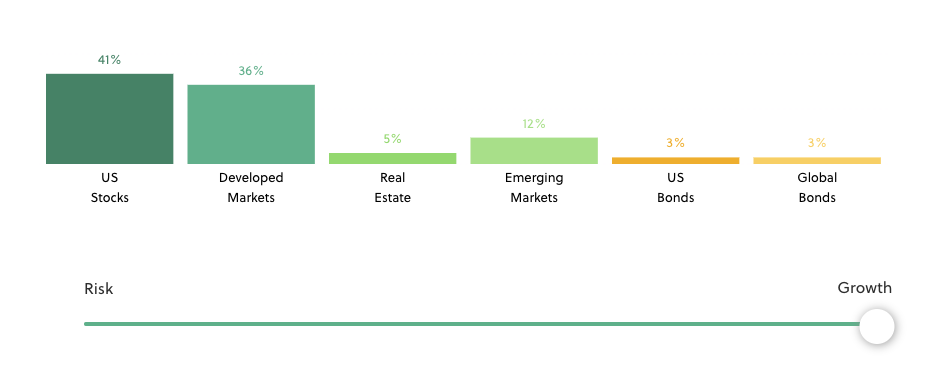

For a more risk-seeking investor and/or someone with a longer time horizon, the portfolio will look something like this:

Here, stocks make up 89% of the portfolio, bonds 6%, and REITs 5%.

These are not arbitrary numbers by any means. Rather, they are the product of applying the Modern Portfolio Theory to these two sample investors.

It also bears mentioning that every asset in this portfolio is an ETF:

- US stocks: Vanguard Total Stock Market Index Fund ETF (VTI)

- Developed markets: Foreign Developed Markets (IEFA)

- Emerging markets stocks: Vanguard Emerging Markets Stock Index Fund ETF (VWO)

- US bonds: Vanguard Total Bond Market Index Fund ETF (BND)

- Global bonds: Vanguard Total International Bond Index Fund ETF (BNDX)

- REITs: Vanguard Real Estate Index Fund ETF (VNQ)

Sarwa uses Vanguard’s ETFs because they are cheaper, transparent, and provide better opportunities to attain broad diversification with just a few ETFs.

To summarise all the information above, let’s consider what the portfolio of Investor A – a risk-seeking investor learning how to invest $1,000 a month – will look like:

- VTI – $400 (40%)

- IEFA – $200 (20%)

- VWO – $100 (10%)

- BND – $100 (10%)

- BNDX – $100 (10%)

- VNQ – $100 (10%)

Setting up your SIP will require that you have something like the above: a diversified portfolio of ETFs designed to minimise your risk and maximise your returns so you can achieve your goals.

2. Automating monthly transfers from a local bank account to an investment account

In learning how to invest $1,000 in stocks every month, the next step would be to actually take the monthly investment amount from your local bank account (checking or savings account) and transfer it to your investment account.

For Investor A, this means consistently transferring $1,000 as a lump sum to their investment account every month and purchasing VTI, IEFA or VOO, VWO, BND, BNDX, and VNQ based on the allocation formula that has been decided.

A company like Sarwa makes this process easier by allowing you to automate the deduction and the investment allocation. So, if your payday is the 25th of every month, you can set up your Sarwa account to automatically deduct $1,000 from your account on that day, and then it will automatically spread your money across all ETFs in order to best maintain your portfolio allocation.

Aside from the convenience, such automatic deduction ensures that you are faithful to your budget.

George Clason, the author of The Greatest Man in Babylon, proposed that the best way to steadily invest is to pay yourself first. That is, you should invest first and then spend the rest. In this way, you will avoid spending your investment amount on other things.

Automating your monthly investment is the perfect way to follow Clason’s advice.

3. Rebalancing the portfolio

A passive investor committed to SIP does not need to tamper with his investment portfolio that often.

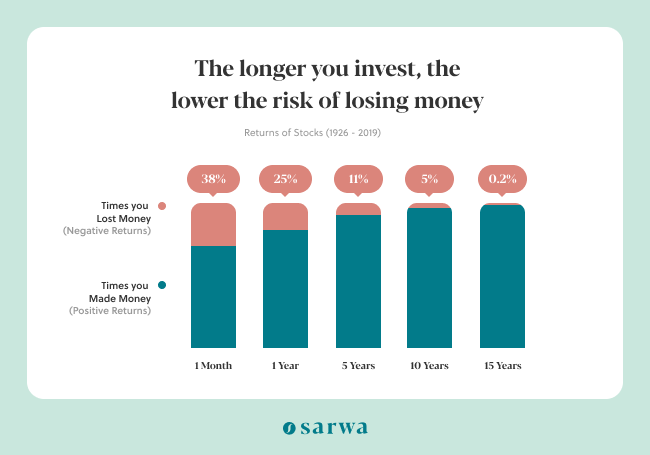

Insead, the passive approach is meant for long term investors who are willing to ride the short-term price fluctuations and focus on the bigger goal – the wealth that will be built at the end of your investment time horizon, be it five, 10 or 20 years.

This commitment to the long term is important since the stock market rises more than it falls and the longer the time spent in the market, the higher the probability of profiting and the less the risk of losing money (as seen below).

The only time a passive investor should tweak their portfolio is when the current portfolio allocation has become unbalanced due to gains and falls of prices.

Take Investor A as an example. His ideal allocation formula is 40:20:10:10:10:10, as seen above. Due to price fluctuations (some ETFs rising and others falling), it is possible for the allocation to become something like 30:10:10:20:15:15, for example.

Since this latter allocation is not the target one, the investor can rebalance it by selling a portion of the ones that have gone overboard and buying more of the ones that have fallen. Again, this is the only time a passive investor worries about tweaking their portfolio.

A digital financial advisor like Sarwa helps investors automate the rebalancing process so that they don’t have to worry about it.

Therefore, a Sarwa investor can be sure that the ideal portfolio that minimises risk and maximises returns will be upheld.

Also, Sarwa ensures that the rebalancing is done optimally – not too frequently and not too sporadic.

4. Reinvesting dividends

Compound interest and wealth is best maximised when an investor reinvests the dividend they earn.

“If you reinvest dividends, you can supercharge your long-term returns because of the power of compounding,” according to Investopedia. “Your dividends buy more shares, which increases your dividend the next time, which lets you buy even more shares, and so on.”

With a platform like Sarwa, investors can easily choose to have their dividends reinvested every quarter instead of receiving them as cash into their bank accounts.

5. Monitoring performance

In the introduction, we noticed that you would have $83,156.62 at the end of year 5 if you invest $1,000 per month for five years.

This calculation assumed an average interest rate of return of 11.97%, which is the average returns of the S&P 500 Index, an index containing the 500 largest US companies, from 2010-2020.

However, research has shown that while the S&P 500 yields a good return, the type of diversification we suggested above – that combines stocks, bonds, and REITs – will produce even higher returns. And this is why we advise against investing only in the S&P 500.

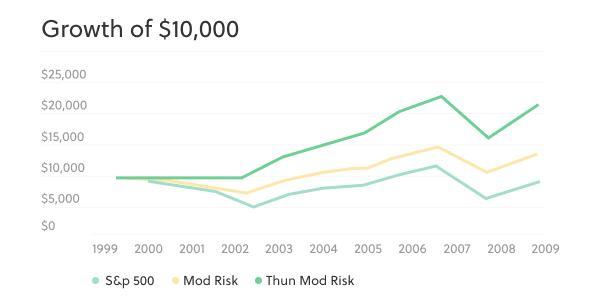

At Sarwa, we did a study comparing the performance of three portfolios between 2000 and 2009.

The first portfolio contained only the S&P 500 index; the second (Mod Risk portfolio) was an allocation to US stocks (40%), global stocks (30%), and high-quality bonds (30%); and the third (Thun Mod Risk portfolio) was “diversified across multiple asset classes including stocks, bonds, real estate, and commodities.”

We discovered, as seen below, that the broader the diversification, the higher the returns, with the Thun Mod Risk portfolio outperforming the S&P 500 and the Mod Risk portfolio.

In essence, building a diversified portfolio can both reduce risk and increase returns. To continue with our example, suppose a diversified portfolio produces average returns of 13%, which is 1.03% higher than the S&P 500’s. With this, you could expect $85,484.41 instead of $83,156.62.

Of course, past performance does not guarantee future performance (and stocks are not fixed deposits or money market assets). Nevertheless, it is the only way we can reasonably project what future performance could be. This projection is important in deciding which kind of portfolio will help to achieve your goal.

For example, if you need a portfolio that can produce annual average returns of 10% in the next 10 years to achieve your goal, then choosing a portfolio that has done it over the past 10 years (Portfolio A) makes more sense than one that has returned only 5% over the past 10 years (Portfolio B). Though there is no guarantee, it still makes more sense to choose Portfolio A over B.

However, while it is important to know the potential returns you will get at the end of the investment period (so you can determine if you can meet your investment goal), this should not translate to an obsession over current market conditions and trending news.

“Waiting helps you as an investor and a lot of people just can’t stand to wait,” said Charlie Munger, vice chairman of Warren Buffett’s Berkshire Hathaway. “If you didn’t get the deferred-gratification gene, you’ve got to work very hard to overcome that.”

Consequently, the most important thing in learning how to invest $1,000 per month for five years is to create your portfolio, continue investing slowly and steadily, rebalancing your portfolio when needed, and keeping your eyes on the long-term prospects of your portfolio instead of the short-term price movements.

[Do you want to build a personalised portfolio based on the Nobel-prize winning Modern Portfolio Theory? Sign up for Sarwa and get access to a portfolio that will help you achieve your financial goals.]

Takeaways

- Building wealth requires consistently and steadily investing in the stock market through a systematic investment plan (SIP) for a time period.

- To implement a SIP, the investor must create a diversified portfolio, transfer the SIP amount into it every month, and rebalance the portfolio as at when due.

- For ordinary investors, a diversified portfolio of ETFs is the best investment.

- Investors must choose the best portfolio that has the potential of minimising their risk and maximising their compound interest.

- Successful SIP requires a long-term approach to investing instead of an obsession with short-term fluctuations.