Is it not pointless (or even boring) to invest just $100 in the market when others are investing thousands and millions? Perhaps you have asked yourself this question and wondered if there is really any gain to learning how to invest little money instead of waiting for your cash to add up so you can invest more significant amounts.

Well, to put it simply, starting out small is wise investing. There are at least four reasons why investing your “small” amounts is better than just spending it indiscriminately or stashing it in a savings account to wait for it to accumulate.

First, the small amount you invest now will continue to grow in the stock market and benefit from compound interest, what Albert Einstein once called the eighth wonder of the world.

For example, if you put $100 every month into the stock market, you will have potentially earned $21,499.31 at the end of 10 years (with interests compounding quarterly and with the average return on the S&P 500 being 10.7% per annum).

If you had instead chosen to spend this $100 every month, there wouldn’t be any amount waiting for you.

Second, the earlier you start investing, the more time you have to earn compound interest.

That is, the more time you spend invested, the more returns you can potentially earn from your investment. If we change the number of years in the above example from 10 to nine, then you will have $18,210.99, a difference of $3,288.32. Just by spending one year out of the market, you are set to lose more than $3,000.

Third, learning how to invest a little money will prepare you to invest larger amounts.

Benjamin Graham, the mentor of Warren Buffett, said that successful investing requires both a plan and behavioural discipline. By learning how to invest money wisely with small amounts, you can build that discipline and apply it to larger amounts.

Fourth, the global inflationary pressure that has remained strong since the beginning of 2022 requires that you learn to protect your future purchasing power by investing in the stock market, irrespective of the size of your investment.

With global inflation, the interest you will earn from savings accounts or bonds will continuously be difficult to meet up with the rise in the prices of goods and services.

For example, if the $100 you put in a savings account only earned $2 (at a 2% interest rate) in a year but the average prices of goods and services has increased by 5% in the same time, then that $102 in cash is less valuable than it was a year ago.

In fact, the average interest rate on savings accounts in the UAE is just 1.32%, and it is only 0.16% in the US. With growing inflationary pressure, savings account returns will find it increasingly difficult to keep up with growing inflation.

In contrast, the S&P 500 still has an average annual return of 10.7%, which is better suited to keep up with rising inflation. Therefore, it is better to invest even a small amount of money than put it in a savings account (except if it is money you need in the short term).

Consequently, instead of wasting your $100 (or what have you) on things you don’t need or putting it in savings accounts that can’t keep up with inflation, you should learn how to invest a little money to earn compound interest and build the discipline you need for the future.

In this article, we will consider 10 ways to safely and wisely build wealth with small amounts of money. We’ll cover:

- Set SMART goals

- Create an investment plan

- Start investing immediately

- Seek to minimise costs and fees

- Minimise your risks with diversification

- Seek to maximise your returns

- Understand safe investment options in Dubai

- Avoid risky investments

- Use an online financial advisor to invest money wisely

- Discipline yourself

[Do you want to create an investing plan that will help you achieve your financial goals? Sign up with Sarwa and get started on the right foot.]

1. Set SMART goals

Any kind of investing (whether it’s with a little or a lot of money) must begin with understanding why.

Why do you want to invest in the first place? So that you can retire well? Leave an estate for your children? Travel around the world? Maybe buy a house?

Whatever the motivation is, you need to be clear about it. A clear grasp of the “why” will help you to endure potential hurdles along the path of wealth building.

After pinpointing your high-level dream, you need to turn it into a wise SMART goal; that is, a specific, measurable, achievable, realistic, and time-bound goal.

This basically means outlining your dream with actionable ways that can help you measure your success. For example, if your dream is to “retire early” you can turn that into a SMART goal like “retiring early at the age of 38 with AED 1 million in my retirement account.”

Even though you are starting off by investing with just a little money, you can still set big goals and visualise their results to make the dream crystal clear. If you can almost see the dream materialising, then you have started off on the right track.

2. Create an investment plan

Once you know the “why” you can begin to focus on the “how”.

Say you want to retire at 38. How do you go about achieving that? How much money do you need to be saving? How often should you save and for how long?

Setting SMART goals is not enough; you need an action plan to achieve them.

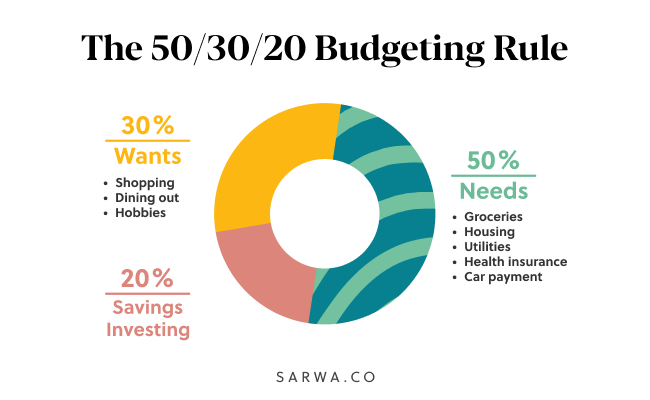

Start by creating a budget if you don’t already have one, and then begin identifying how much you want to save on a monthly basis. The 50/30/20 rule, a budgeting system popularised by Elizabeth Warren, a US senator, is a good place to start.

With this system, you spend 50% of your income on your needs (housing, insurance, clothes, transport), 30% on your wants (entertainment, vacation, leisure), and 20% on savings/investment.

No matter how small that 20% of your income is – maybe just $100 – you still need to create a monthly investment plan that will detail how you will use that $100 every month to achieve your financial (SMART) goals.

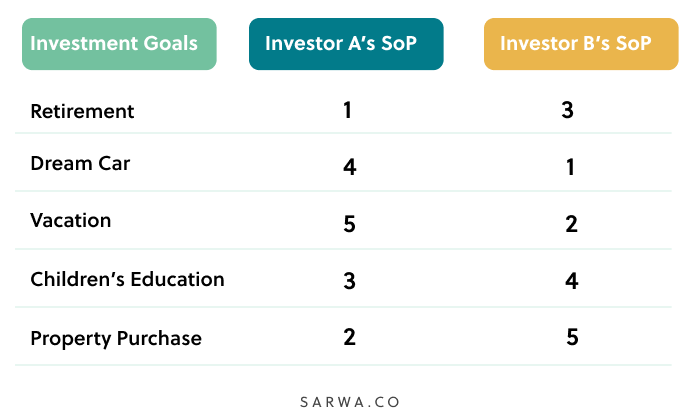

A monthly investment plan will require that you divide your goals into short-term, medium-term, and long-term goals. Also, it will require you to rank your goals in the order of preference. Below is a sample scale of preference of two investors:

By ranking your goals in this way, you will know which ones to direct your monthly savings (the 20% of your income) first and which ones can wait.

Also, by clarifying whether a goal is short, medium, or long term, you will be able to decide whether that goal requires saving or investing.

For example, if you want to buy your dream car in six months, you are better off saving the money in a savings account. However, achieving your retirement plan will require that you put money in an investment account.

[For more on how to decide between saving and investing, read “How Much Percentage of Savings Should You Invest In The Market?”]

Another important point needs emphasising: planning to save money and actually saving it is not the same thing.

To stay faithful to your savings target, “the moment you get paid, you remove the money out of your account,” advises Andrew Hallam, personal finance journalist, and author of Millionaire Teacher.

“Treat it like a tax if you need to. Get it out of the account, so you are not tempted to spend it. And that’s the most effective way to maximise your savings potential.”

The faster you begin outlining a structured way to save, the faster you can begin to clearly identify exactly what to do with your little start-up investment.

3. Start investing immediately

As said above, the more time you spend in the market, the more compound interest you will earn. This is because research has shown that the stock market rises more than it falls.

As a study by the Center for Research in Security Prices has shown, between 1926 and 2019, the stock market rose 74% of the time and fell only 26% of the time.

Therefore, it is better to start investing immediately instead of holding off to a more opportune time – also known as market timing. This latter approach deprives you of the returns you could have earned in the waiting period.

Also, though market timing seeks to benefit from buying the dip (buying a stock when its price is very low), in reality, “Buy the dip is one of those things that works really well on paper, but it doesn’t work well in real life,” according to Callie Cox, senior investment strategist with Ally Invest.

Many of these investors realise that what they thought is the dip is just a step in the continuing downtrend. Consequently, they still lose money (even after missing out of possible returns in the waiting period). And for those who are impatient to wait for the recovery of the market, that loss is permanent.

In fact, a report by Dalbar Inc. has shown that waiting for a more opportune time (timing the market) is a strategy that is guaranteed to ensure that you underperform by 5% over 30 years.

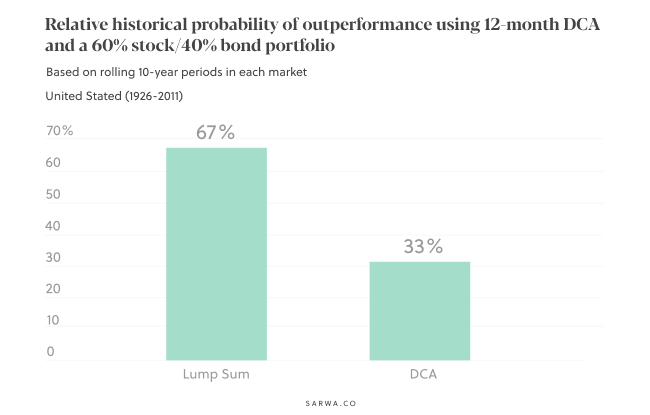

Similarly, investing immediately (also known as lump-sum investing) is better than splitting the money into smaller amounts and investing it over a defined period (also known as dollar cost averaging). In a Vanguard study, the former approach outperformed the latter by 67% in six months and by 92% in one year.

Consequently, investing your $100 now is better than splitting it into $20 invested over five months. That means that lump-sum investing is the best approach for those learning how to invest little money.

Nevertheless, dollar-cost averaging has many benefits, especially for new investors who are not yet confident about investing all their savings in the market at once. It can help you overcome the temptation to market timing and emotional investing, help you build discipline, and take advantage of a stock market crash.

In summary, while it’s best to invest your little money with lump-sum investing, dollar-cost averaging is also a good option, while market timing (buying the dip) is not advisable.

4. Seek to minimise costs and fees

To invest money wisely, you need to reduce the fees you pay for investing.

If you are an active investor, you will incur various brokerage fees and commissions when you buy or sell stocks. For example, ADCB securities charge a minimum of AED 78.5 per trading session (all brokerage fees and commissions excluding VAT).

If you choose to invest in mutual funds instead, the mutual funds will charge you for their expense ratio (management and administration fees) and other commissions when you purchase them. This is because in their effort to beat the market, they often need to pay high administration and management overheads.

However, with Sarwa Trade, you can open a free brokerage account and buy and sell stocks without paying any commissions or local transfer fees (to transfer money from your bank account to the investment account).

If you are a passive investor, you will also need to choose exchange-traded funds (ETFs) that have low expense ratios and an online financial advisor with low management fees.

With Sarwa Invest, you can get access to a portfolio of low-cost ETFs for low management fees, which reduces as the amount invested increases.

5. Minimise your risks with diversification

Many people have stuck with savings accounts as low-risk alternatives because of the risk that comes with the volatility of stocks.

However, instead of enduring the poor returns of savings accounts, investors should stick with the high returns of stocks and then seek to minimise their investment risk.

Whether you are an active investor who buys and sells individual stocks or a passive investor who invests in a portfolio of passive ETFs, you need to diversify your investment portfolio to reduce your investment risk.

Portfolio diversification is the way to avoid putting all your eggs in one basket.

Before the 1960s, investors didn’t know what to do with risk because it was hardly measurable. Instead, investors depended on selecting stocks with good fundamentals, buying them at a perceived low-value price and holding them for the long-term – a strategy called value investing.

The problem was that a company many investors thought had good fundamentals could still end up failing for many reasons.

In that event, small investors were often left holding the bag — essentially, losing money for following the poor predictions made by larger investors. This exposed large amounts of individual retail investors to all the unsystematic risks associated with a particular company — the company fails, you lose all your money.

However, in 1952, an economist, Harry Markowitz, published an article called “Portfolio Selection” in the Journal of Finance that would change how investors approached risk forever.

The article led to the formulation of the Modern Portfolio Theory, for which he won a Nobel Prize in Economics in 1990. In his theory, Markowitz developed a systematic way to measure risk through variance and standard deviation. Furthermore, he emphasised that the average investor is risk-averse — he/she will more likely desire to minimise risk for a given level of return.

Therefore, Markowitz expounded a simple way to minimise risk: portfolio diversification.

By buying several stocks that are not positively correlated (what causes stock A to fall causes B to rise, and vice versa), said Markowitz, an investor can minimise his risk. In essence, the risk of a portfolio of non-positively-correlated stocks is less than the risk of one single stock in that portfolio.

For example, owning stock of a company in the finance industry exposes you to all the risks in that industry. But by buying a stock in finance, another in healthcare, and yet another in consumer goods minimises your overall risk exposure.

When the finance industry is down, the healthcare industry will not necessarily be down because they are distinct industrial ecosystems with distinct supply chains and business models.

The benefits of stock diversification are further amplified by buying across geographies and companies of various sizes (classified by market capitalisation).

It is a simple but powerful solution to invest with a little money wisely. By following Markowitz, portfolio diversification prevents an investor from having all his/her eggs in one basket.

As someone looking to start investing with little money in Dubai, you should understand how to minimise your risk by diversifying.

Putting your money in one stock is a novice mistake that could cost you bundles.

Instead, you should have a diversified portfolio consisting of stocks, bonds, and REITs, so you can minimise your risk exposure.

With active investing, you can do this by buying stocks from different companies, with different market caps (diversification by market cap), in diverse industries (diversification by industry), and across various economies (diversification by market).

Sarwa Trade allows you to achieve this even with little money through fractional trading. That is, on Sarwa Trade, you can buy fractional shares instead of buying a single share. For example, if you can’t buy a share of Apple’s stock (which is $138 at the time of writing), you can buy one-fifth (or 20%) of a share for $27.6. In this way, even with your $100, you can buy multiple stocks and diversify.

Nevertheless, with small money, diversification is easier with ETFs. With just a single ETF, an investor already enjoys a measure of diversification.

For example, the Vanguard S&P 500 ETF (VOO) exposes you to all the stocks in the S&P 500 index. In that index, there are U.S. stocks from various industries like communication services, consumer discretionary, financials, healthcare, information technology, consumer supplies, among others. So when you buy a single unit of VOO, you have a stake in almost 500 large-cap companies with various unsystematic risks.

Now imagine the diversification you will get from buying many non-positively correlated ETFs.

As an active investor, you can buy and sell ETFs on Sarwa Trade and as a passive investor, you will get a portfolio of diversified ETFs when you sign up for Sarwa Invest.

6. Seek to maximise your returns

It is natural to seek to maximise your returns for the long term, but doing so wisely (as we have seen) requires understanding how to also minimise risk.

Investors and mutual funds who try to outperform the market have proven to chronically underperform it, and thus add more risk to your investment.

A study by SPIVA shows that 89% of large-cap, 84% of mid-cap, and 89% of small-cap equity mutual funds underperformed the market over 10 years (2009-2019).

Active investing isn’t only expensive; it also has a historical record for underperforming.

Therefore, to maximise your returns, you should stick with passive investing. Unlike active investing, passive investing focuses on holding for the long-term a diversified basket of securities that matches the performance of a market index. Instead of trying to beat the market and failing at a high cost, passive investors match the performance of the market at a lower cost.

This is the same investment strategy that Buffett has long supported, and even placed friendly bets on.

Warren Buffett once placed a bet that the S&P 500 Index Fund (a passive fund) would outperform a basket of securities selected by Protege Partners over a 10 year period. Buffett won the $1 million bet as the S&P 500 Index Fund returned 7.1%, while Protege Partners’ basket of securities returned an average of 2.2%.

However, it bears mentioning that active investing also has its advantages. First, it is more flexible as it allows investors to tweak their portfolio as often as they like to achieve their goals. Also, though many active managers fail to beat the market, some, like Peter Lynch, have a history of success behind them. Those who can do this will enjoy better returns than their passive counterparts.

Similarly, active investing allows investing strategies like hedging and tax loss harvesting, which can help to reduce risk and taxes, respectively.

Therefore, if you are confident in your knowledge and experience, you can try your hands on active investing. But remember that even successful investors like Warren Buffett and Peter Lynch have advised ordinary investors and beginners to stick with passive investing.

7. Understand safe investment options in Dubai

Learning how to invest with little money begins with the “why’ but eventually ends with the “where.”

We have already seen that buying ETFs is better than buying individual stocks for those with low money due to the advantage of diversification. Therefore, for small investments in Dubai, you are better off with an actively managed (through Sarwa Trade) or a passively managed (through Sarwa Invest) portfolio of ETFs.

With the former, you will create your own portfolio of ETFs and make your own buy and sell decisions. With the latter, Sarwa uses the Modern Portfolio Theory to create a diversified portfolio of ETFs that will help you minimise your risk and maximise your returns given your unique personal time horizon, risk tolerance, and financial goals.

Whichever one you choose, these are some safe investment options in Dubai at your disposal:

- Stock ETFs: Stocks still offer the best returns of all the asset classes. When you own the stock of a company, your money grows with the company. While stocks on their own are high-risk, buying an ETF of stocks reduces your risk to the barest minimum (because of diversification). A single stock ETF is already a diversified portfolio of stocks in itself. Also, buying stock ETFs (compared to individual stocks or equity mutual funds) will save you lots of money in commission and fees.

- Bond ETFs: Bonds produce lower returns at a lower risk. When combined with stocks in a portfolio, they help reduce your overall risk. The best way to buy bonds is through ETFs since they provide you with a diversified selection of bonds. A single bond ETF exposes you to many bonds, diversified by market (among others). Buying bonds through ETFs is also cheaper than the alternatives.

- REITs ETFs: Since you are investing with only a little money, you probably don’t have enough to buy real estate. However, instead of buying real estate, you can purchase the stock of real estate and mortgage companies and grow your money as they grow. That’s what REITs are for. Another advantage of REITs is that they pay significant dividends, which provide you with regular income you can reinvest for more compound interest. A REITs ETF also provides you with a diversified selection of ETFs, thereby lowering your risk.

Of course, if you prefer to buy individual stocks with your low money (as a way to gain more control over the companies you own), you can do so with Sarwa Trade. However, given that you are investing with little money, you are better off with ETFs.

What about Crypto?

Due to popular demand, Sarwa now allows investors to diversify into crypto. Passive investors can do this by adding bitcoin to their portfolio (with a suggested limit of 5% of total portfolio value) – an investment solution called Sarwa Bitcoin.

Also, active investors can now buy and sell various cryptocurrencies through the Sarwa Trade app – a solution called Sarwa Crypto.

Bitcoin enthusiasts have pointed to its value as digital gold – diversification, hedge against inflation, and an opportunity to earn outsized returns. Nevertheless, Jiro Kondo, Associate Professor of Finance at McGill University and Head of Portfolio Construction at Sarwa, has issued some caution about these benefits. “Bitcoin still has a very long way to go to reach true ‘gold-like’ status and there’s no guarantee that the recent convergence trend will continue,” he said.

Also, “the link between bitcoin’s finite supply and its effectiveness as an inflation-hedge is still theoretical,” according to Kondo. “We don’t have historical evidence to back up this hypothesis because inflation expectations have been fairly low and stable during the period that bitcoin has been meaningfully traded [e.g., 2015 and beyond].”

This is why Sarwa offers a portfolio that limits investment in bitcoin to 5% of the investor’s portfolio value. However, investors who are more confident in Bitcoin and Crypto in general, can always buy and sell them actively with Sarwa Crypto, available on the Sarwa Trade app.

8. Avoid risky investments

Warren Buffett, the legendary investor, has said that an investor’s top priority should be to avoid losing his money.

“Rule No. 1 is never lose money,” goes the oft-quoted Buffetism. “Rule No. 2 is never forget Rule No.1.”

Consequently, you should avoid risky types of investments like:

- Real Estate Investment: Real estate is expensive, so the consequences of things not working out are enormous. When you buy a property, there are also lots of fees involved, and locking yourself into a single, costly physical asset is just about as opposite from diversification as you can get. Also, you might find it difficult to sell or rent your properties during economic downturns. These are just some of the reasons why investing in real estate is not safe.

- Day Trading: Day trading is market timing on steroids. For the same reasons we discourage market timing, we also discourage day trading. “Calling someone who trades actively in the market an investor is like calling someone who repeatedly engages in one-night stands a romantic,” said Warren Buffett. “The stock market is designed to transfer money from the active to the patient.”

- Gold: The problem with gold and many commodities is that they are unproductive. On its own, gold does not contribute to any economic activity, so its price only changes based on speculation. There are no fundamentals to gold, and most people buy it because of the fear that the stock market will drop. But we know that the market rises more than it falls.

9. Use an online financial advisor to invest money wisely

As said above, many successful investors have advised ordinary investors and beginners to stick with passive investing. And this is even more important for ordinary investors with small investments in Dubai.

To get the best out of passive investing, ordinary investors need to use online financial advisors. These advisors use the best investing theories to construct a personalised passive portfolio of ETFs (or index funds) based on the investor’s time horizon, investment goals, and risk tolerance. That is, they can use their knowledge and experience to help investors get the best out of passive investing.

An online financial advisor like Sarwa uses the Modern Portfolio Theory to help investors build a diversified portfolio of ETFs that will maximise your returns and minimise your risk. They also help you automatically reinvest your dividends and interest, as well as regularly rebalance your portfolio.

Those looking to safely invest with little money will find that Sarwa also allows accessibility, with a minimum investment requirement of just $5.

Though many people consider them online investing platforms, digital financial advisors like Sarwa actually do more than help you invest your money. And this is why they prefer the name “digital financial advisor” to “robo-advisor.” They can also help you:

- Set up a budget

- Create a retirement plan

- Make specific plans to achieve specific goals

In this way, they work to help you better understand yourself and establish a strategy that matches.

An online financial advisor will seek to understand your current situation, your goals, and present challenges, and then help you develop and implement strategies that will help you overcome the challenges needed to achieve your goals.

Unlike traditional financial advisors, online financial advisors are more accessible and offer much lower costs.

The best way to manage your small investments in Dubai is to automate your investments (to avoid spending what you should invest) through an online financial advisor that can offer these automated online investing and financial planning services.

10. Discipline yourself

Learning how to invest with little money is incomplete (especially for Dubai investors) without talking about the emotions involved in investing.

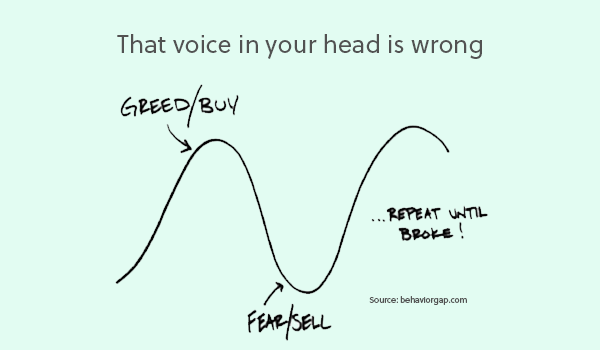

People lose money in the market because of fear and greed. They follow the crowd and make poor emotional decisions. Here is one of the most favourite (dare I say infamous) graphs at Sarwa describing this situation.

What is the remedy?

Invest for the long term.

“I will tell you how to become rich,” once said Warren Buffett. “Close the doors. Be fearful when others are greedy. Be greedy when others are fearful.” As Benjamin Graham said, behavioural discipline is as important as having a financial plan.

Perhaps the most important piece of sage advice we can give here is don’t follow the crowd.

Sometimes this is easier said than done (we are an emotional and communal species, after all!), but the wise investor will always assert that it is this kind of discipline that will most pay off over the long run.

Stick with your portfolio and continue to invest. Remember, the market rises more than it falls (74% compared to 26%), and with diversification you are effectively maximising your returns while minimising your risk.

Once you start investing (even with only a little money), there is statistically less risk to worry about as the years go on.

[So, are you ready to safely invest your little money and grow wealth with it? Sign up with Sarwa Invest or Sarwa Trade for a passive or active approach to investing.]

Takeaways

- It’s better to invest a little money than spend it unnecessarily or put it in a savings account where it will hardly earn enough to cope with rising inflation.

- Even with little money, you will need to identify your financial goals and create an investment plan to achieve them.

- Successful investing requires that you minimise your risk and maximise your returns by investing in the best investment assets and avoiding the risky investment vehicles.

- An online financial advisor can help you automate your investment as well as provide personalised financial advice and investment portfolios.